11:06 am

This morning I had given a “worst case” scenario for the SPX to retrace 61.8% of its decline from mid-August. The Wave structure may be developing for a much quicker resolution. Wave C may be complete at the 50-day Moving Average at 4021.00, a 30% retracement. It may also extend to the 38.2% retracement at 4054.00. Should it elect one of these levels, it may be accomplished at the end of the day. Remember, this is a Primary Wave [3]. Threes are very powerful and destructive to the downside. This “whipsaw” is meant to shake out the weak hands. Stay strong.

8:00 am

Good Morning!

You may have already guessed that I keep alternate charts to attempt to explain the seemingly chaotic moves in the market. This may be the most viable alternative at this time.

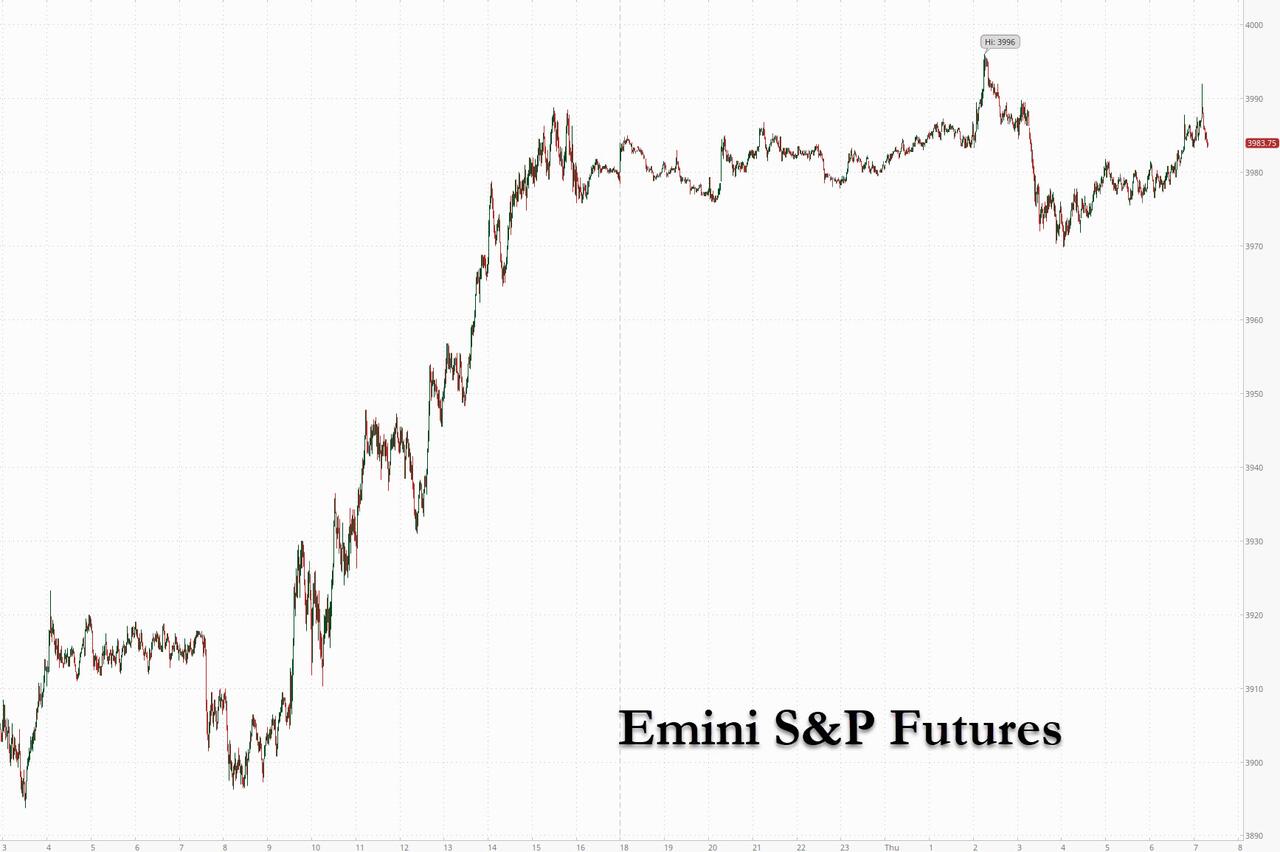

SPX futures remain stalled after reaching 3994.60 in the overnight market, pressing the long gamma zone. The scenario pictured above suggests the retracement may go as high as 4106.00, the 61.8% retracement of Wave (A). The Cycles Model suggests a probable extension of this retracement to Monday. Hopefully sooner, but the market is out to prove everyone wrong…again.

In today’s op-ex, Max Pain is at 3975.00. Calls dominate above 3985.00 and long gamma begins at 4000.00. Fortunately long gamma peaks at 4100.00, thus the retracement value I noted earlier. Short gamma begins beneath 3900.00.

ZeroHedge reports, “US stock futures traded flat, erasing modest earlier gains and losses in the overnight session as investors remained cautious while watching for signs of a softening in the Federal Reserve’s policy. Nasdaq 100 futures were little changed by 7:15 a.m. in New York after earlier gaining as much as 0.6%. S&P 500 contracts were up less than 0.1%, at 3,983.75 after hitting 3,996 overnight and following small gains in Estoxx50. The underlying index notched its biggest gain in a month on Wednesday which was sparked by yet another short squeeze, and is attempting to rebound following three straight weeks of declines that were fueled by fading bets on a Fed policy pivot and as investors braced for the impact of a potential economic contraction. Crude oil futures managed a feeble, +0.5% bounce after falling 5.7% Wednesday. The dollar reversed earlier gains helping lift the badly beaten EUR and JPY higher.”

VIX futures pressed against mid-Cycle resistance at 25.10, but remained beneath it. Should the SPX scenario be viable, we may see VIX drop to 20.00 in the next couple of days. Trending strength (long) may return after next week’s op-ex.

Wednesday’s op-ex shows short gamma below 25.00, but peters out at 23.00. What is more scary to the dealers is that VIX calls dominate above 26.00 and long gamma begins at 30.00 and extends to 60.00.

TNX futures declined to 32.01 this morning, giving more credence to the money flows, especially from the European continent. The Cycles Model suggests rates may begin to tumble on Tuesday and intensify through the end of September. However, this Master Cycle may not end until mid-November. Commentators are still looking through the rear-view mirror.

ZeroHedge comments, “US nominal yields are quite the rage these days.

And the dollar is having a heyday like no other, with the yen, the euro and the pound desperately in need of some smelling salts – except that there is just no one to nurse the non-dollars back to health in quick order.

Underpinning the inexorable increase in dollar-denominated nominal yields and the chutzpah in the greenback is, of course, the surge in inflation-adjusted yields in the state-side.

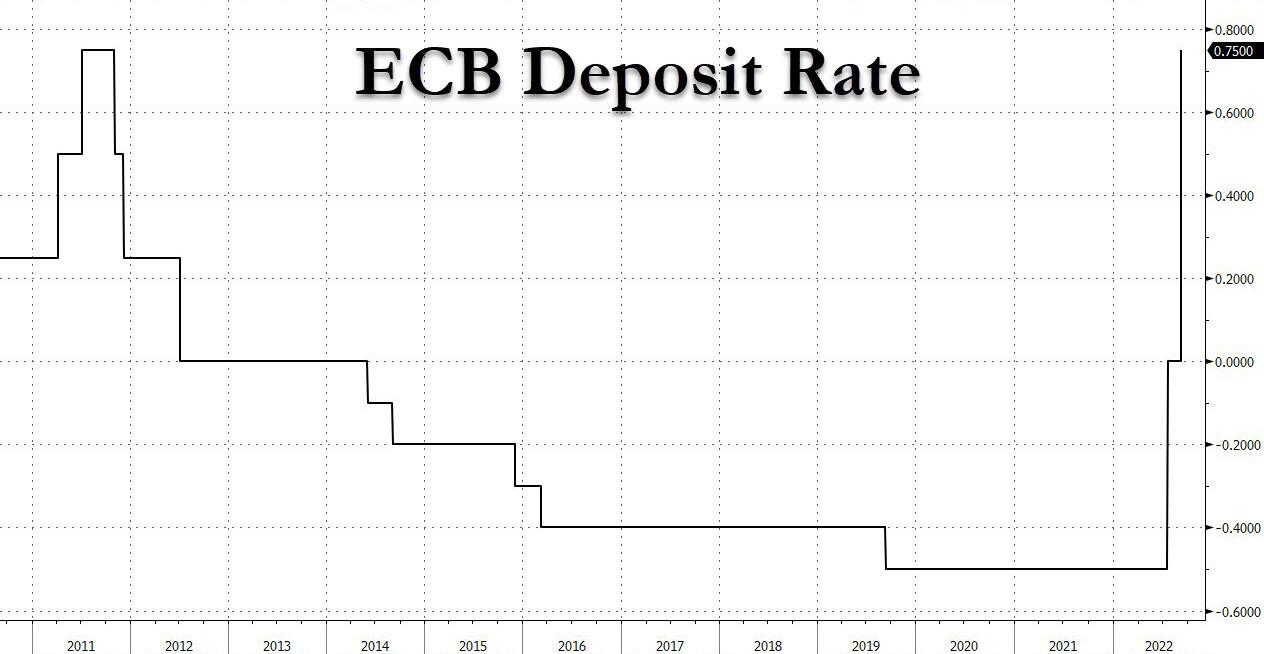

In a related note, ZeroHedge observes, “And we have the answer: after lots of heming and hawing, moments ago the ECB hiked its deposit rate by 75bps from 0% to 0.75bps, the first time European rates are positive in over a decade (since July 2012) noting that “the Governing Council’s future policy rate decisions will continue to be data-dependent and follow a meeting-by-meeting approach.” The ECB itself described today’s move as a “major step” that’s frontloading the transition toward a more neutral policy stance, and said that following the raising of the deposit facility rate to above zero, “the two-tier system for the remuneration of excess reserves is no longer necessary” and “the Governing Council therefore decided today to suspend the two-tier system by setting the multiplier to zero.”

USD futures declined to 109.32, testing the upper trendline near 109.00. Should USD decline beneath the trendline in the next few days, it may decline back to the 50-day Moving Average at 106.93 by the end of the month for the end of the current Master Cycle. However, the USD may remain in its uptrend through the end of the year.

My concerns were realized as WTI futures plummeted beneath its prior low. This morning it bounced to 82.90, but the course is set for a continued decline through the end of October. Brent oil is under 90.00, suggesting the European bailout may fail to provide enough liquidity to carry out its plan.

Gold futures rose to an overnight high of 1739.35, suggesting a continued retracement higher. The current Master Cycle has a week to go, so I wouldn’t put much emphasis on this rally. The big test will be the Cup with Handle trendline at 1675.00. Should that take place, gold may decline through the end of November, fulfilling the Cup with Handle target(s).