9:34 am

The Ag Index appears to have finally made a reversal yesterday, at day 287 of the Master Cycle, matching the 10-year Treasury at 285 days. I don’t know what the relationship is, other than the rising cost of money has an effect on food prices. What the Cycles Model suggests is that GKX may now decline through mid-November. Since it has already achieved the 50% retracement value at 432.52, it is likely to target the 61.8% retracement at 387.96. An added confirmation is straight line support at 380.54. What we are dealing with is not supply-and-demand. Instead we are dealing with market forces, namely lack of liquidity and possibly a transportation shutdown this weekend.

OilPrice.com observes, “Energy crises impact nearly every aspect of our lives, and that is particularly true of food markets, with food production next year expected to be severely threatened.

- About 70 percent of the cost of fertilizer production is solely the price of natural gas, and as the price of energy soars, the cost of making and moving food is increasing alongside it.

- At the same time, Russia’s invasion of Ukraine and threats from Putin that Russia may alter grain export routes have only added to uncertainty in food markets.

The problem with an energy crisis is that it’s actually an everything crisis. In a world where virtually every industry relies on energy in some form, runaway inflation is an inevitability. This phenomenon is not news – you’ve been experiencing it for the better part of two years now. But while global governments are using every tool in their kits to curb the rising inflation rates, there’s far less they can do about the coming food shortage. ‘

7:45 am

Good Morning!

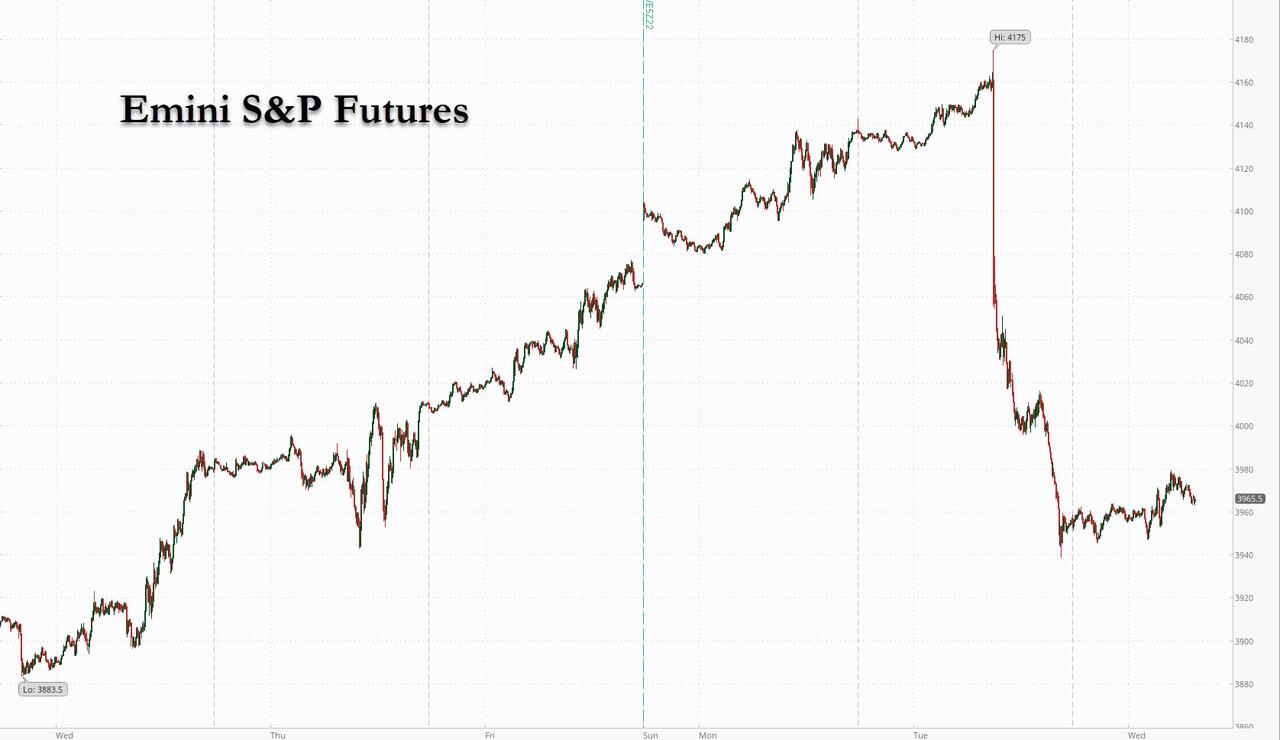

NDX futures rallied to 12137.70 in the overnight markets, but are now approaching negative territory. Considering the speed of the decline, NDX may open beneath the most recent low at 11928.81. The Cycles Model calls for an acceleration to the downside into the weekend, very likely making new bear market lows.

In today’s op-ex, Max pain is at 12090.00. Long gamma begins at 12275.00, while short gamma lies at 12010.00. This morning’s futures have already placed NDX into short gamma with more puts every 100 points down to 11100.00. Friday’s monthly op-ex shows short gamma beginning at 12000.00 with 2453 put contracts at that point.

ZeroHedge observes, “Heading into today’s CPI print, one of the most notable positioning technicals that helped push risk assets higher (since it isn’t buybacks which are about to enter their new blackout period starting Friday), was that CTAs went from furious sellers just two weeks ago, to aggressive buyers late last week. Well, after today’s historic rout which saw the S&P tumble over 4%, the most since June 2020, and the Nasdaq plunged more than 5%, at least there is no more doubt which was the systematics are leaning.

First, here is JPM equity derivatives strategist Bram Kaplan, who echoed Nomura’s Charlie McElligott writing that “we’re back to a material put imbalance on today’s sell-off” and estimates that “between option hedging flows and the ~$15Bn levered ETFs need to sell based on today’s moves so far”, there’s risk of continued downward momentum. Worse, in a follow up, Kaplan confirms that “CTAs probably are already selling on today’s move, as we crossed back through the 50d & 100dma (that were taken out on the upside on Friday) on SPX (at 4040 and 4023) and NDX (at 12619 and 12456), and the 50don RTY (at 1863)”

SPX futures also bounced, but are now testing yesterday’s low at 3921.28. The Cycles Model allows a short bounce this morning before resuming the decline. Theoretically the bounce may go as high as 4000.00. However there may be a time limitation that could run out well before reaching that point. The 50-dqy Moving Average is at 4030.00.

Today’s op-ex shows Max Pain at 3975. Calls don’t seriously rule until above 4000.00. Short gamma begins at 3950.00.

ZeroHedge reports, “US equity futures are trying to rebound after their biggest plunge in more than two years, when the hotter than expected CPI print wiped out 4.3% or $1.5 trillion in market value from the S&P, and are up a modest 0.2% at 730am ET, erasing most of an earlier gain of 0.6%. Nasdaq 100 futures rose 0.7% after the tech-heavy gauge tumbled 5.5% in its worst day since March 2020. Ahead of today’s PPI print, the Bloomberg dollar index retreated after jumping the most in three months on Tuesday, while 10-year Treasurys ticked higher, hovering near a decade-peak. Oil was flat now that the traders consider $80 as a “Biden Bottom.”

VIX futures declined to 26.29 before a rebound brought it near the close. Yesterday it made a new high at 28.15 for the month and the trend may continue after a brief pullback. The mid-Cycle support may be tested before a resumption of the trend. The Cycles Model suggests the VIX may reach a Master Cycle high on or near the 21st of September. I will try to fine-tune that projection as we approach the date.

Today’s op-ex shows Max Pain at 27.00. Short gamma may begin at 26.00, while long gamma starts at 29.00. Should long gamma emerge, VIX may be driven as high as 37.50 (or higher) today. Investors are buying calls extending to 60.00 with 5353 call contracts at that level for today’s close. Next week’s (Sept 21) op-ex in the VIX is loaded with 55837 call contracts at 100.00. Theoretically, VIX should not go above 100. However, speculators are buying calls with strikes up to 180!

DailyFX comments, “There is no mincing words on how extreme the swoon in risk assets was this past session. The S&P 500’s -4.3 percent tumble was the largest since June 11, 2020 – with no other comparable declines before the tumult of the pandemic (February to March 2020) since August 2011. As one would expect from a sweep of risk appetite, the more targeted Nasdaq 100 suffered a more intense -5.5 percent tumble which drove the Nasdaq-to-Dow ratio (growth-to-value) sharply lower. It wasn’t just a US indices phenomenon. From European equities to emerging markets to junk bonds, there was a sympathetic plunge. And yet, correlation and intensity signals neither conviction or capitulation – though you will find true believer bears and bulls make the argument. Such intense moves historically have not generated a strong record of immediate follow through – in fact recent years could be used to infer a turn, but I would argue against such immediate contrarianism. That is particularly true of those opportunists constantly on the hunt for ‘capitulation’ to ‘pick a bottom’ on the market. While the market’s shift was sharp and severe, we are far from the measures of panic that can historically reflect a market that has flushed its hold out hopes. I would consider that extreme on the VIX to be somewhere on the order of the 50.0 handle, but we are barely above the half-way point on that stretch.”

TNX continues its rise to a new retracement high on day 285 of the current Master Cycle. It has not overcome its June 14 high at 34.83, but may do so if it doesn’t reverse immediately. The Cycles Model has run out of trending strength as of yesterday, so today may see the onset of the reversal today. The Model calls for a decline to mid-November in the 10-year.

ZeroHedge reports, “In today’s shitshow of a post-CPI market session, the last thing traders needed to worry about was whether the 30Y TSY auction would be a failure. Luckily, it wasn’t, and moments ago the Treasury sold $18bn in 30Y paper (in a 29-Y 11-Month reopening of cusip TJ7), in a far stronger auction than yesterday’s lousy 3 and 10Y sales.

The high yield of 3.511%, was – as expected – the highest since April 2014, surpassing the previous Fed tightening top of 3.418% from November 2018. More importantly, the yield stopped through the 3.530% When Issued by 1.9bps, the biggest strop through since March as traders are buying at least one of today’s dips.

The bid to Cover of 2.419 was slightly above last month’s 2.310, and was generally in line with the six-auction average of 2.37%. In other words, not great, not terrible.”

USD futures challenged the trendline this morning at 108.97 as it gains its footing for a new surge higher. Trending strength rises into the weekend and through the following week until the next Master Cycle high, due at month-end.

Crude oil futures are consolidating beneath Intermediate-term resistance at 90.69. Prior strength on Monday has now evaporated and the decline may resume at any time. The Cycles Model suggests weakness increasing by the weekend, suggesting new lows. (Is someone reading my blog?)

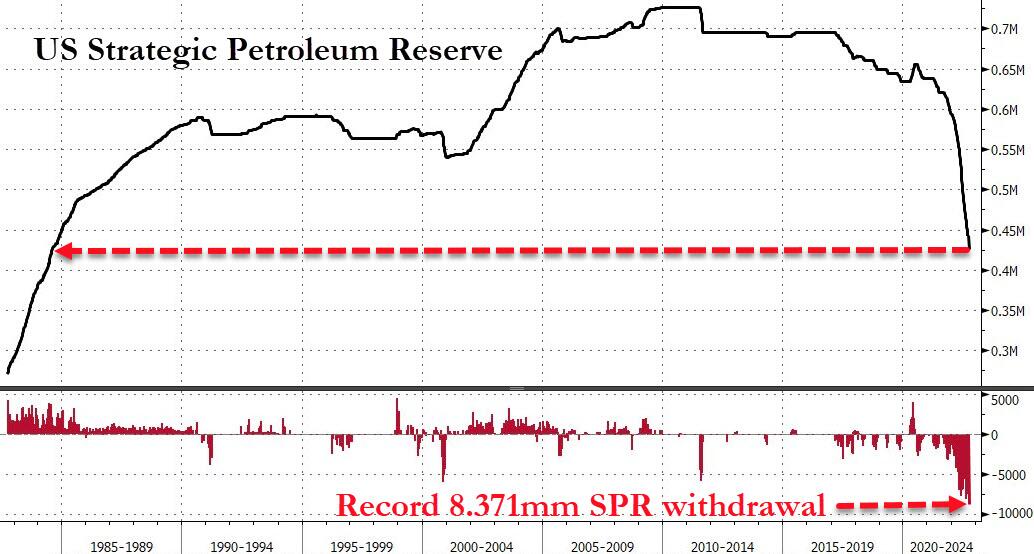

ZeroHedge comments, “A day after we reported that the Biden administration withdrew a record amount from the US Strategic Petroleum Reserve plunging it to its lowest since 1982, Bloomberg reports that, according to people familiar with the matter, the US may begin refilling its emergency oil reserve when crude prices fall to around $80 a barrel.

The sources said that Biden administration officials are weighing the timing of such a move, with an eye toward protecting US oil-production growth and preventing crude prices from plummeting (in an effort to reassure oil producers that the administration won’t let prices collapse).

The reaction in WTI was immediate with the front-month bid (well above $80)…”