7:40 am

Good Morning!

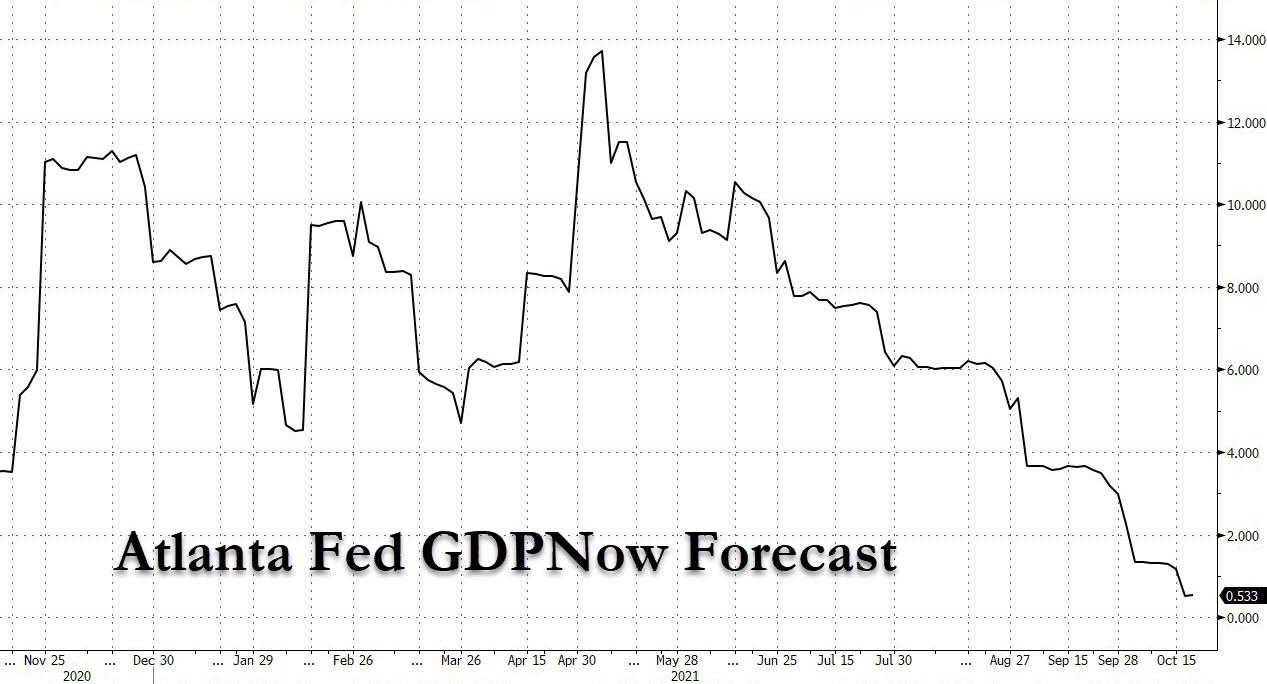

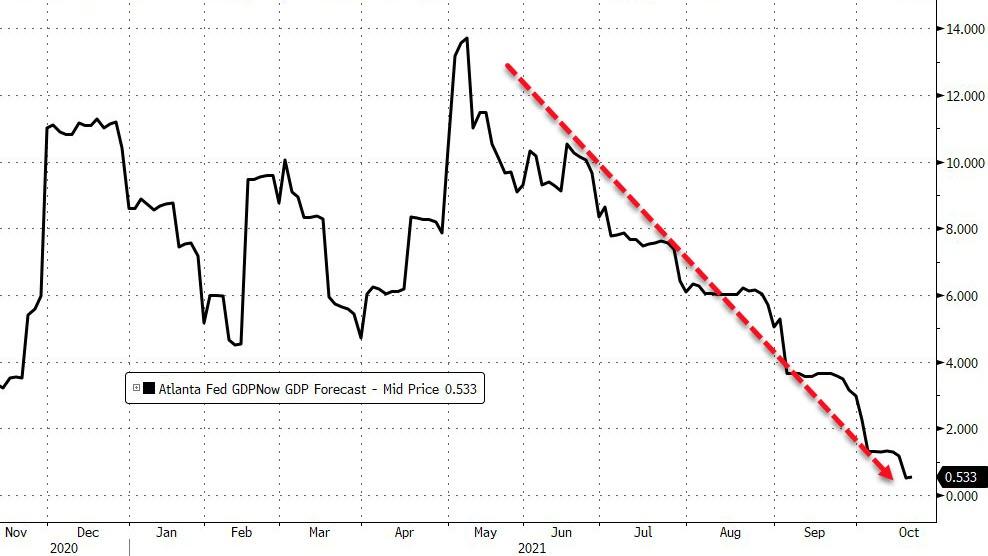

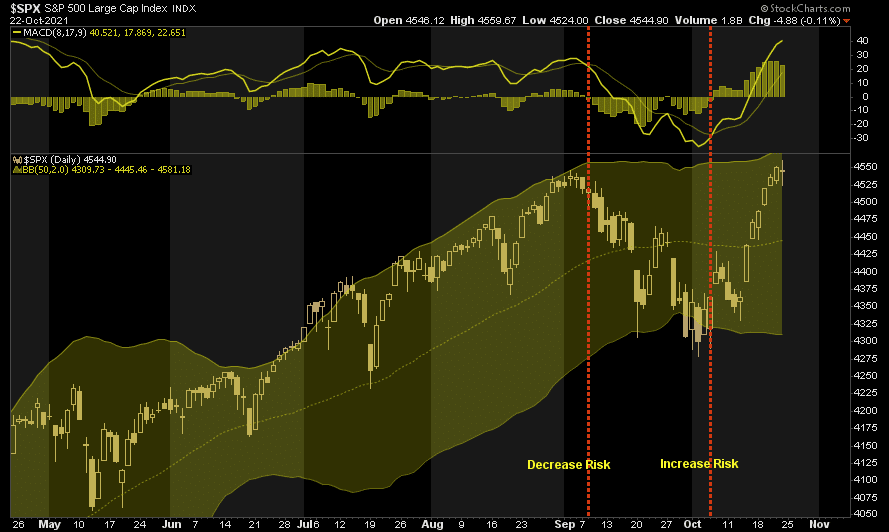

The Dow Jones Industrials made a new all-time high on Friday, but the weekend futures only managed to consolidate within Friday’s trading range. It is possible that Friday’s high on day 266 of the Master Cycle may be the top. A breakdown beneath the Cycle Top support at 35650.00 may provide the first clue of a reversal.

Following up on Dow Theory, the Transports are not providing the confirmation needed by the DJIA to extend its highs much higher. Both indices making new all-time highs are needed to declare the uptrend as healthy. As you know, logistical errors and bottlenecks are causing a slowdown in the delivery of goods across the nation at a reasonable price. As a result, the economy is showing signs of stress. Not only are grocery shelves going bare, but there are work stoppages due to the lack of parts and strikes due to labor restrictions and inadequate pay.

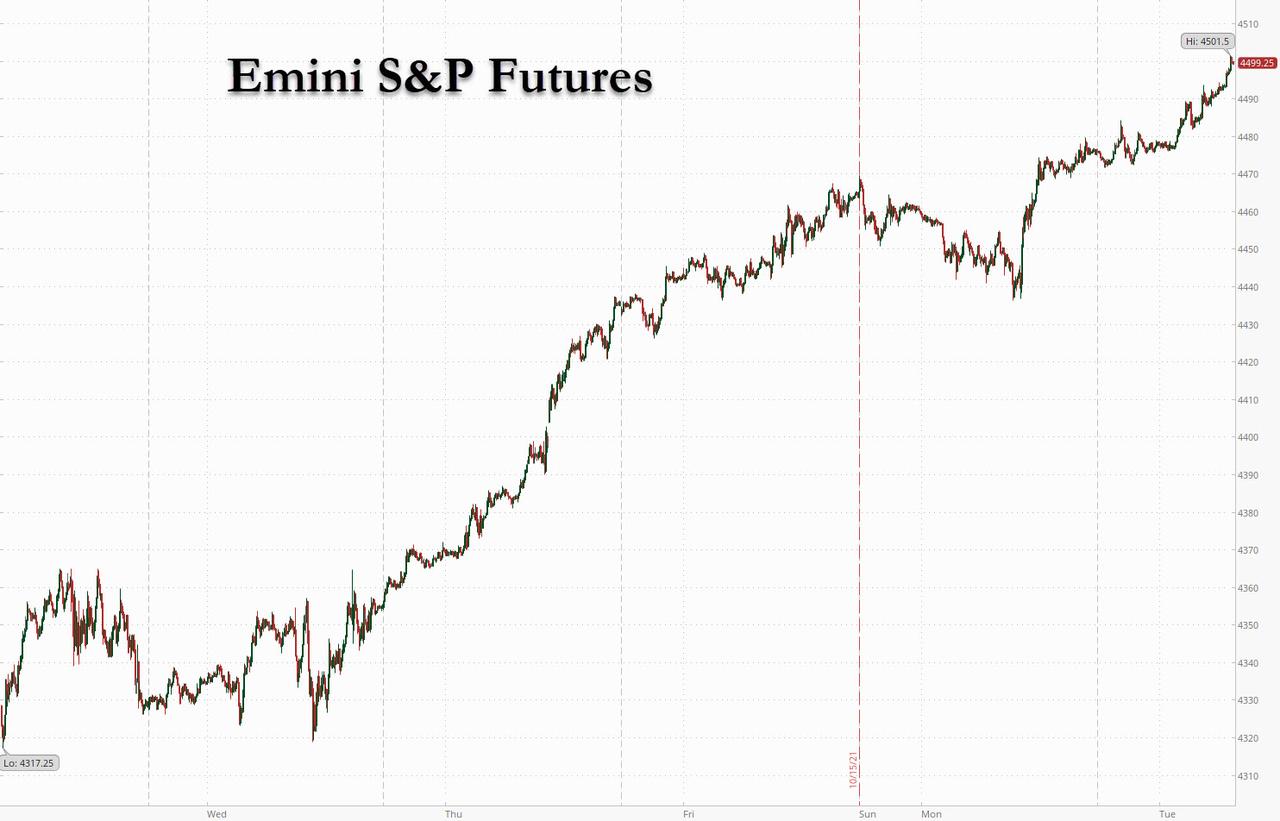

SPX futures hovered between 4531.00 and 4554.50 over the weekend. Today is day 269 of the Master Cycle. Today’s options expiration may remain at Max Pain at 4545.00, but beneath that it runs the risk of negative gamma building as it goes lower. It’s a light option day, so dealers and hedge funds may not see the need to alter their holdings until SPX ventures beneath 4500.00. Having entered the “positive season,” institutions see little reason to hedge against a possible sell-off. A friendly reminder theough…the positive season going into year-end normally starts at a seasonal low, not a high.

ZeroHedge reports, “One day after Goldman doubled down on its call for a market meltup into year-end, futures on the Nasdaq 100 edged higher, while contracts on the S&P 500 were modestly higher on Monday, approaching record highs again as investors braced for a flood of earnings (164 of 500 S&P companies report this week) while weighing rising inflation concerns, Covid-19 risks and China’s deteriorating outlook (Goldman slashed China’s 2022 GDP to 5.2% from 5.6% overnight). The FOMC enters quiet period ahead of next week’s FOMC meeting, which means no Fed speakers as attention shifts to economic data and corporate earnings. At 745 a.m. ET, Dow e-minis were up 3 points, or 0.01%, S&P 500 e-minis were up 4.25 points, or 0.1%, and Nasdaq 100 e-minis were up 36.25 points, or 0.25%. Bitcoin bounced back over $63,000 after sliding below $60,000 over the weekend, the 10-year US Treasury yield rose and the dollar also rose after Federal Reserve Chair Jerome Powell flagged that inflation could stay higher for longer, fueling investor concern that sticky price increases may force policy makers to raise borrowing costs.”

VIX futures also consolidated within Friday’s trading range, neither going higher nor lower than Friday’s possible Master Cycle low on day 254. The VIX and SPX Cycles don’t match, making the top in equities sloppy. Last Wednesday’s high in the Hi-Lo makes Friday’s high in the DJIA and SPX and low in the VIX a likely scenario for the top in equities.

RealInvestmentAdvice observes, “Market Surges Toward Previous Highs

Last week, we discussed the “correction being over” for the time being.

“While the market started the week a bit sloppily, the bulls charged back on Thursday as earnings season officially got underway. With the market crossing above significant resistance at the 50-dma and turning both seasonal “buy signals” confirmed, it appears a push for previous highs is possible.

Two factors are driving the rebound. Earnings, so far, are coming in above estimates. Such isn’t surprising as analysts suppressed estimates going into reporting season. Secondly, bond yields declined.“

Chart updated through Friday.

However, to expand on a point from last week, breadth remains dismal, with only 60% of stocks above their respective 50-dma even though the index is at all-time highs.”

TNX appears to be consolidating near Friday’s high. This week it is due for a minor pullback but not likely to go far. Trending strength may come back on Wednesday, so a trade may not be warranted.

Crude oil futures continue to rise to new highs at 85.36, exceeding its 2016 high on Friday. Crude may have completed a running correction, with a practically non-existent pullback last week. The Cycles Model favors a continuation of this rally for the next 4 weeks before a larger pullback may be made.

ZeroHedge observes, “It’s remarkable that just last April, West Texas Intermediate crude was trading at a negative $40. Well, fast forward to today when moments ago, the US black gold grade just topped $85 for the first time since 2014, the landmark in a global energy crunch that has seen prices soar. Brent traded about 150 cents higher as the spread between the two grades has narrowed sharply in recent weeks.

Oil has jumped in recent weeks as natural gas prices hit records; as a result of rising gas-to-oil switching overnight Goldman forecast that the surge in gas prices could add at least 1 million barrels a day to oil demand “with current gas forwards incentivizing this through winter.” In the note from Goldman commodity analyst Callum Bruce, the bank also estimated that global oil demand has surpassed 99 mb/d and will shortly hit its pre-COVID level of 100 mb/d as Asia rebounds post the Delta wave.”