2:33 pm

While we were watching the SPX, another indicator has turned. The BKX, a proxy for market liquidity, has reversed down from Monday’s high and the Cycle Top resistance at 140.05. A Master Cycle reversal may be considered a sell signal, but we await another indicator…the 50-day Moving average at 129.48 for a confirmed sell signal. The Cycles Model suggests lower liquidity through late November or early December. This index tells us what is keeping all assets afloat for the past 18.5 months, perfect timing for a Wave (b). The coming decline may match or exceed the decline from February 2007 to March 2009.

ZeroHedge observes, “Since the last FOMC meeting (September 22nd) – when Chair Powell began to detail the taper and rate-hike traajectory to come – bonds are down (yields higher) but stocks, gold, and the dollar are all up around 1%…

Source: Bloomberg

And even more notably, the trajectory (and initial timing) or rate-hikes has soared…

Source: Bloomberg

But the long-end of the yield curve is signaling that The Fed will once again commit a faux-pass…”

2:23 pm

Today’s action verifies the Master Cycle high put in on Friday. The Cycles Model suggests lower rated through mid-November. This doesn’t make sense to many, but the money flows tell all.

ZeroHedge reports, “After an ugly 3Y auction, and a solid 10Y sale yesterday, moments ago the Treasury sold $24BN in a 29 Year-10 month reopening of cusip SZ2 ahead of today’s Fed minutes. But if one thought investors would show any nerves about the coming taper in today’s auction, boy were they in for a surprise.

That’s because the auction was nothing short of spectacular: stopping at 2.049%, the auction stopped through the 2.062% When Issued by 1.3bps, which aside from last month’s 1.8bps stop, was the first non-tailing auction in 5. That said, it was the highest auction for the 30Y tenor since June’s 2.172, even if there was no concession in today’s session as a result of the sharp grind lower in yields on the long end if not the short one.”

2:05 pm

SPX revisited the MAX Pain level at 4375.00, but could not maintain it. It has also failed at the Short-term support at 4366.75. The negative gamma may take hold and propel SPX much lower. The Cycles Model suggest a strong move today, possibly a panic decline. The Model supports the notion that, once it begins there may be no stopping it this week, just in time for monthly options expiration.

The NYSE Hi-Lo Index opened at 22.00 and rose to 58 tis afternoon. A reversal may give it a negative number at the close of the day.

8:15 am

Good Morning!

SPX futures rose to test the 100-day Moving Average at 4362.45 this morning. Should it not be able to rise above it, the next suport is the Lip of the Cup with Handle formation at 4306.00. The Max Pain zone for today’s options is at 4375.00. Today’s expiring options become increasingly more bearish down to 4300.00, where there are 6800 net open interest contracts expiring today. The Cycles Model implies trending strength over the next three days. suggesting a panic decline may be in the making.

ZeroHedge reports, “For the second day in a row, an overnight slump in equity futures sparked by concerns about iPhone sales (with Bloomberg reporting at the close on Tuesday that iPhone 13 production target may be cut by 10mm units due to chip shortages) and driven be more weakness out of China was rescued thanks to aggressive buying around the European open. At 800 a.m. ET, Dow e-minis were up 35 points, or 0.1%, S&P 500 e-minis were up 10.25 points, or 0.24%, and Nasdaq 100 e-minis were up 58.50 points, or 0.4% ahead of the CPI report due at 830am ET. 10Y yields dipped to 1.566%, the dollar was lower and Brent crude dropped below $83.

JPMorgan rose as much as 0.8% in premarket trading after the firm’s merger advisory business reported its best quarterly profit. On the other end, Apple dropped 1% lower in premarket trading, a day after Bloomberg reported that the technology giant is likely to slash its projected iPhone 13 production targets for 2021 by as many as 10 million units due to prolonged chip shortages. ”

VIX futures are in a consolidation mode, neither going higher nor lower than yesterday’s range. The Cycles Model calls for a strengthening VIX over the next two weeks. Today’s expiring options show a preponderance of open interest in puts up to 22.00,, its Max Pain level. Above that level, today’s expiring options support the longs.

TNX is rising this morning, but no new highs. Today is day 259 of the old Master Cycle, so there may still be an extension of the old Cycle.

ZeroHedge comments, “Having slowed for two straight months, whisper numbers predicted a slightly hotter than expected September CPI (edging up to 5.4% YoY, slightly above the consensus of 5.3%) on the back of a re-intensification of supply-chain bottlenecks due to a combination of natural disasters and COVID disruptions in the US and Asia kept pressure on manufactured goods in September.

Headline CPI did indeed come hotter than expected (+0.4% MoM vs +0.3% exp) with the YoY spike edging back up to +5.4%…That is equal to its highest since July 2008.”

Source: Bloomberg

USD futures declined to 94.25 overnight before bouncing to 94.54 this morning. It appears that a correction may still be in the making with a potential slide down to the 50-day Moving Average at 93.08. However, the pullback may be transitory, with strength reappearing early next week.

Crude oil futures cotinue to consolidate above the Cycle Top support at 78.92. The Master Cycle high appears to have been made on Monday with a potential 5-6 week decline. There may be some incentive to keep crude prices high due to options and futures expiration on Friday. But the damage has already been done. A sell signal lies beneath the Cycle Top support.

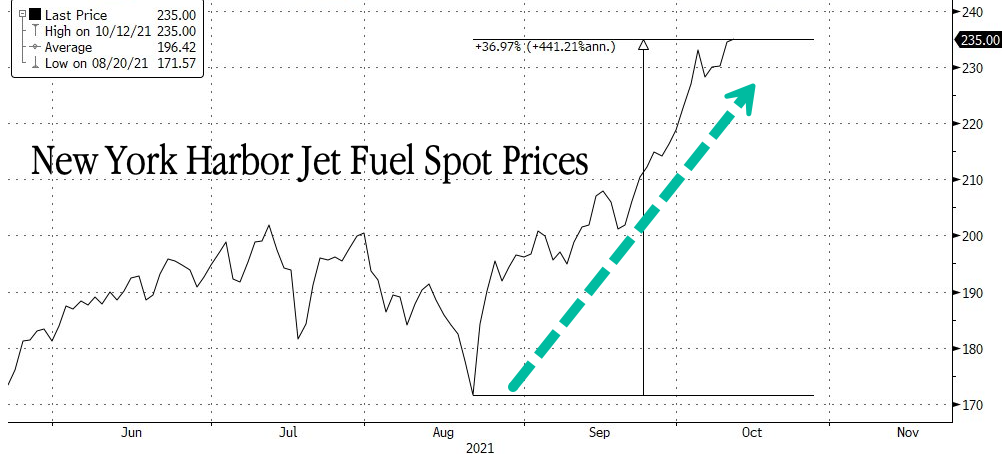

ZeroHedge explains, “Delta Air Lines Inc. delivered a profit in the third quarter but warned soaring jet fuel prices might result in an unprofitable fourth quarter.

Since August, spot prices for New York Harbor Jet Fuel have risen 37%. Delta expects fuel prices between $2.25 and $2.40 a gallon in the quarter, up from $1.94 in the third.

Fuel costs accounted for 20% of Delta’s adjusted operating expenses in the third quarter. Soaring costs are “going to be a limiter on our ability to post a profit in the quarter. At these current fuel levels, it looks like we’ll have a modest loss,” CEO Ed Bastian said. ”