7:45 am

Good Morning!

NDX futures challenged the trendline at 13430.00 this morning, but did not make a new high. This leaves yesterday’s high as the probable Master Cycle pivot on day 272. The lower trendline of the Ending Diagonal formation appears at 13300.00, offering investors a potential sell signal should NDX decline beneath it.

Today’s options expiration shows Maximum investor Pain at 13370.00. Long gamma starts at 13400.00, while short gamma begins at 13350.00. There does not seem to be much confidence in either direction.

QQQ (327.16) options show Maximum Pain at 328.00. Long gamma starts at 329.00, while short gamma begins at 325.00.

ZeroHedge opines, “It is narrow – SPX edition

The SPX/SPX equal weight ratio vs the SPX. Watching the gap closely…

Source: Refinitiv

Beautiful big tech

The NASDAQ vs Russell ratio is printing new recent highs. We are not far from the post Covid panic highs for this ratio. Investors are sucked into chasing tech here, as who on earth can justify being long the crap and not the big quality stuff?

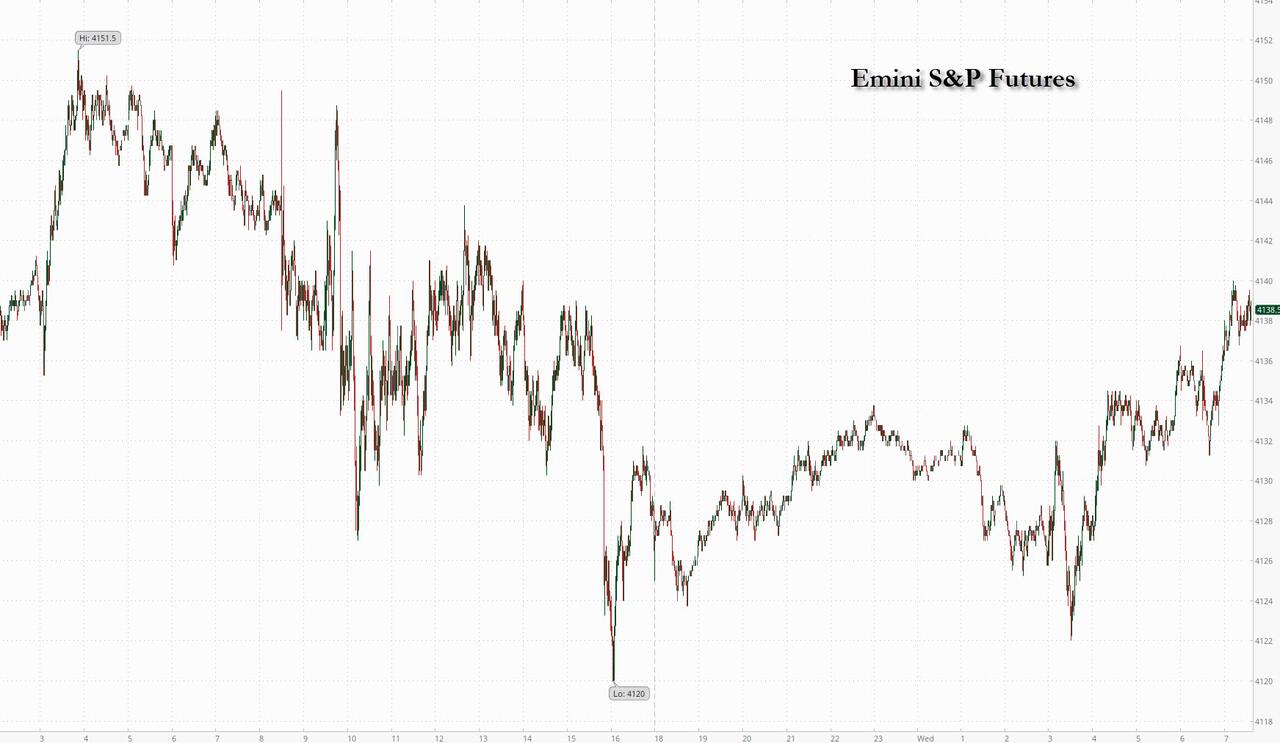

SPX bounced above Intermediate-term support at 4116.69 after closing beneath it. The bounces are weakening to the point where support isn’t holding. We may expect the decline to gain strength imminently. Remember, an aggressive sell signal was made two weeks ago. Aggressive signals often lead to retracement or (in this case) boredom, but it would be unwise to second guess the outcome. Once the decline is underway, the Cycle may continue its decline until mid-June. The Cycles Model suggests that SPX may continue to toe the flat line until the X-date, near June 1.

Today’s op-ex shows Max Pain at 4120.00. Long gamma starts at 4140.00, while short gamma begins in strength at 4100.00. The neutral channel is narrowing…

ZeroHedge reports, “US stock futures crept higher on Wednesday and traded near the best levels of the session, as investors remained focused on debt ceiling talks while negotiators seek a framework agreement for Joe Biden and Kevin McCarthy to review upon the president’s return from a truncated trip to Asia. Contracts on the S&P 500 were up 0.3% as 7:45am ET a.m. while Nasdaq 100 futures added 0.2%. Europe’s Estoxx50 little changed on the day; while Japan’s Nikkei 225 closed above the 30,000 for the first time since September 2021 a day after the Topix closed at its highest level in more than three decades. Treasuries are slightly richer across the curve with spreads broadly within 1bp-2bps of Tuesday’s close while the dollar is flat. Oil rebounded from an earlier drop concerns over demand in China and expectations of rising stockpiles in the US. Iron ore continues its week in the green, while gold and bitcoin declines.”

VIX futures have eased back, but has remained above the long-term trendline. There may yet be a potential surge of strength this week, although much has been accomplished beneath the surface (see below). The next surge in trending strength comes early next week, suggesting more delays in the debt ceiling debacle.

Today’s op-ex shows Max Pain at 20.00, with short gamma extending to 15.00 and long gamma extending to 50.00.

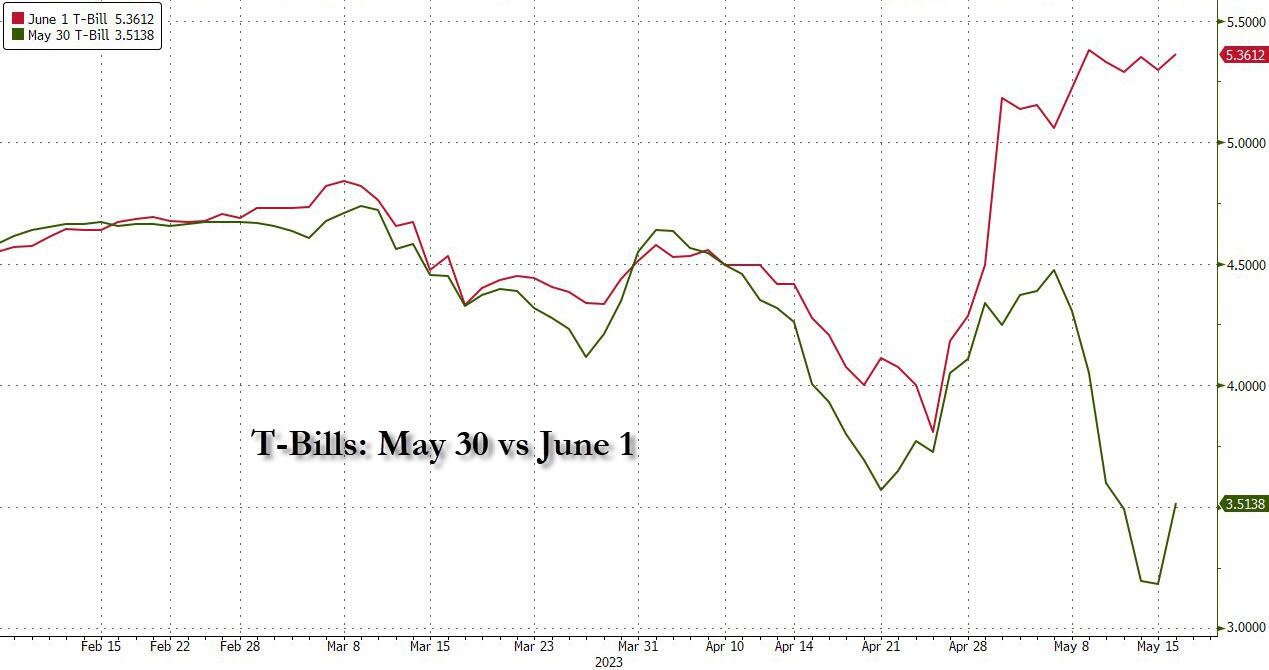

ZeroHedge reveals, “With the debt ceiling game of chicken reaching a crescendo, and just two weeks left until the June 1 X-date, which the Treasury market has already decided is when the US will default (technically) unless a market shock forces Washington to reach a compromise, as observed by the record divergence between the May 30 and June 1 Bills…

… some in the otherwise sleepy and bizarrely complacent equity market are quietly waking up and expecting nothing less than a VIX shock in the next few weeks.

As Goldman trader John Flood writes in his daily market recap, “the street continues to get lifted on wingy VIX upside, something to be mindful of if we do get any vol shock around the debt limit” and specifically, today a Goldman institutional customer bought 50,000 x 150,000 VIX Aug 40-60 1×3 call spreads (bought 60 strike).”

TNX has challenged the 50-day Moving Average at 35.23 this morning, but bounced above it. It may yet test the trendline and Intermediate-term support at 34.70 before trending higher. Trending strength may return by Friday.

ZeroHedge remarks, “Yesterday, in her crusade to scaremonger Republicans into submission and yielding to Biden on the debt ceiling negotiations, Janet Yellen repeated that the Treasury X-Date will be in early June, potentially as soon as the first of the month. The former Fed chair then cranked up the doom to 11, and six years after predicting “no new financial crisis in our lifetimes”, Yellen said that a US default could see “a number of financial markets break – with worldwide panic triggering margin calls, runs and fire sales.” Basically all the worst parts of the bible. And incidentally, Yellen isn’t wrong: a US default would indeed be the end, but of course that will never happen as US tax receipts are more than enough to pay debt interest and maturities; the worst that will happen is that the bloated US deep state and some 25 million government workers will be out of a job, which is long overdue anyway.

Yellen is probably also correct about the timing of the X-Date. As Bloomberg rates strategist Ira Jersey writes, he concurs with Yellen’s assessment “that the debt ceiling X-date could be as early as June 1″ although his calculations suggest the date is a few days later (June 5-8), as shown in the chart below.”

USD futures are moving higher, after overcoming the 50-day Moving Average at 102.29. The Cycles Model suggests the trend may continue until mid-June. The next resistance to challenge is the 200-day at 105.67, running neck-to-neck with the mid-Cycle resistance.