1:03 pm

SPX has made a very irregular retracement, as shorts get squeezed mercilessly. By most standards, the retracement should have ended yesterday. The retracement has taken back 70% of the decline since October 17 thus far. It may be on its final legs, but now that it has gone this far, the 50-day Moving Average at 4352.55 offers a challenge. What’s not to like, especially when BofA and Goldman Sachs are cheerleading? As I said multiple times, this Wave can be treacherous.

ZeroHedge pronounces, “Equities (and bonds) are extending gains this morning with a massive short-squeeze. ‘Most Shorted’ stocks are up over 5% for now, the biggest daily squeeze since February…

Source: Bloomberg

And, as Goldman Sachs Partner, flow-trader John Flood warns, “this squeeze has momentum”.

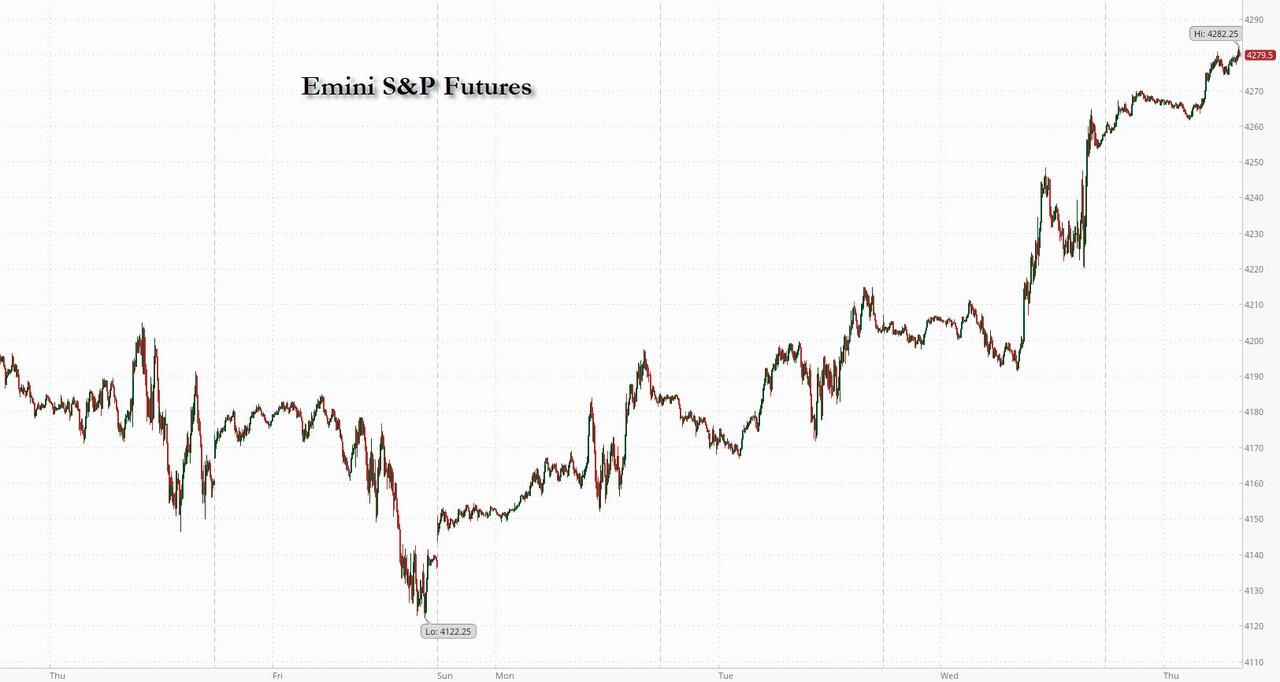

8:10 am

Good Morning!

NDX futures have hit a morning high at 14811.50, on their way to the 61.8% Fibonacci retracement at 14945.00 or possibly the 50-day Moving Average at 14949.82. Some traders and analysts have decided that the NDX isn’t bearish enough and is due for new highs. The Cycles Model suggests the NDX may linger at the highs until mid-day, then resume its decline.

Today’s options expiration shows Maximum Investor Pain at 14725.00. Short gamma begins strongly at 14710.00, while long gamma may take hold above 14800.00. Long gamma does not have a lot of conviction, leaving the rally in a tenuous position.

ZeroHedge notes, ” One week ago, BofA’s Michael Hartnett drew a lot of heat from the permabears when Wall Street’s most accurate strategist of the past decade predicted that a tactical rally was in the cards as one of his closely-followed buy signals had just been triggered. And while stocks did initially dip lower following his Oct 20 note as a result of aggressive mutual fund year-end tax loss selling, the S&P is now back to green from his reco following today’s “dovish at the margins” Fed statement (in Goldman’s words), which may have just given the green light for a year end rally.”

SPX futures have rallied to a morning high at 4269.80, thus far. It has surpassed the mid-Cycle resistance at 4258.64 and may reach Intermediate resistance at 4295.00 or round number resistance at 4300.00. Today may be a trading Cycle (60-day) high, a lesser inflection point that may be finished by mid-day. If so, there may be a month of decline to follow. As mentioned earlier, Wave Bs can be treacherous.

Today’s op-ex shows Max Pain at 4235.00. Long gamma begins at 4270.00 while short gamma starts at 4200.00.

ZeroHedge reports, “US equity futures, and global stocks and bonds extended gains Thursday as traders bet the Federal Reserve is ending its historic tightening campaign, and that easing may not be too far behind. As of 8:00am, S&P 500 futures rose 0.5%, while Nasdaq 100 futures gained 0.7%. Both underlying indexes had jumped on Wednesday after the Fed held interest rates steady and the Treasury announced plans to slow the pace of increases in quarterly long-term securities sales. The dollar weakened and Treasuries steadied after sharp gains following Powell’s comments yesterday. In Asia, the yen extended its gains from Wednesday, while the South Korean won led emerging-market currencies higher. The 10-year TSY yield dipped two basis points after falling below 4.75% for the first time in two weeks. Elsewhere, the latest major company earnings also provided a dose of good news.Commodities are mixed with WTI adding 1.5% in the morning while base metals are for sale. Today, macro calendar is quieter: we have some second-tier labor data (Challenger Job Cuts, Nonfarm Productivity, ULC) and Factory Orders. We will receive AAPL’s earnings after the bell. All eyes on Friday’s NFP and ISM-Srvcs releases.”

VIX futures have declined to 16.12 this morning. A further decline is possible to 15.44 to form an expanded flat formation. The Cycles Model offers little short-term guidance. However, the indications are that trending strength may come roaring back next week.

Next Wednesday’s op-ex shows Mas Pain at 18.00. Short gamma has little advantage over long gamma beneath 18.00. Long gamma starts at 20.00 an had high conviction to 40.00.

TNX plummeted beneath Intermediate support at 47.01 and may be destined to test the 50-day Moving Average at 45.39 by early next week. TNX may be due for a Trading Cycle low at that time. The Cycles Model then suggests the resumption of the rally until the end of November. A possible target at the end of November may be greater that 52.00. By year-end, the 10-year yield may be in the range of 54.00-55.00.

ZeroHedge remarks, “In a clear sign we are reverting to a system where fiscal policy dominates monetary policy, the Treasury’s refunding announcement is probably more consequential than the Federal Reserve’s meeting today. An increased skew away from bill issuance is a headwind for liquidity and risk assets.

The refunding announcement is in focus due to the US’s huge fiscal deficit. It comes when rising yields – i.e. loose fiscal policy meets tight monetary policy – means the government’s interest-rate costs are soaring.

The rapid rise in US yields to ~5% points to the government’s annual interest-rate bill rising to 4.5-5% of debt outstanding in the next six months. That’s in the region of $1.7 trillion – or the GDP of Australia – each year.”