9:45 am

BKX may have made its reversal today, on day 258 of the Master Cycle. It was repelled by Intermediate resistance at 78.89 yesterday, giving the BKX an aggressive sell signal. A further decline beneath support at 75.50 confirms the sell signal. The Cycles Model suggests a decline lasting up to seven weeks. This is not a sector to own.

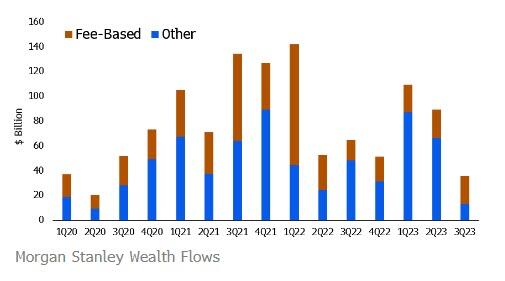

ZeroHedge breaks the first bad news, “Morgan Stanley reported Q3 earnings of $1.38 per share on net revenue of $13.3 bn (better than the $1.22 and $13.2 bn that were expected).

However, while the numbers beat on the top and bottom lines, wealth management revenue disappointed at $6.40 bn versus $6.58 bn expected”

8:00 am

Good Morning!

NDX futures declined to a morning low of 15021.20, beneath both the 50-day and 100-day Moving Averages at 15066.00. This gives the NDX its sell signal. Today the 50-day Moving Average makes its bearish cross beneath the 100-day Moving Average. Today is day 258 in the old Master Cycle. While the NDX may make a new high in the next few days, the chances become less likely as time passes. The Cycles Model projects an approximate month of decline.

Today’s options expiration shows Maximum Investor Pain at 15175.00. Long gamma starts at 15200.00 while short gamma begins at 15160.00, beneath the 50-day Moving Average.

ZeroHedge reports, “In a world where dealer gamma, 0DTE derivatives, positioning, technicals, and liquidity regularly eclipse fundamentals, here are the most important market levels, according to Goldman trader Cullen Morgan (full note available to pro subs).

Summary:

- CTA Corner: Goldman has CTAs modeled short -$82bn of global equities (8th %tile). In the US, CTAs are short -$30bn of equities after buying $16bn last week. Per GS model, the CTAs are now buyers of SPX in every scenario over the next week.

- GS PB: The GS Equity Fundamental L/S Performance Estimate rose +0.80% between 10/6 and 10/12 (vs MSCI World TR +2.42%), driven by beta of +1.11% (from market exposure and market sensitivity combined) partially offset by alpha of -0.32% on the back of long side losses (link).

- Buybacks: This is the final week of the estimated blackout window. As companies have started releasing earnings, we will start to see them enter their open window period. We estimate companies typically enter open window 1-2 days post earnings release. This next open window period is estimated to be 10/23/23 – 12/08/23 (link).

- Charts in Focus: Sentiment Indicator, SPX vs. Singles Skew, Call Skew vs. Put Skew, S&P Futures Liquidity, Funding Spreads vs. S&P 500, VIX call volume.”

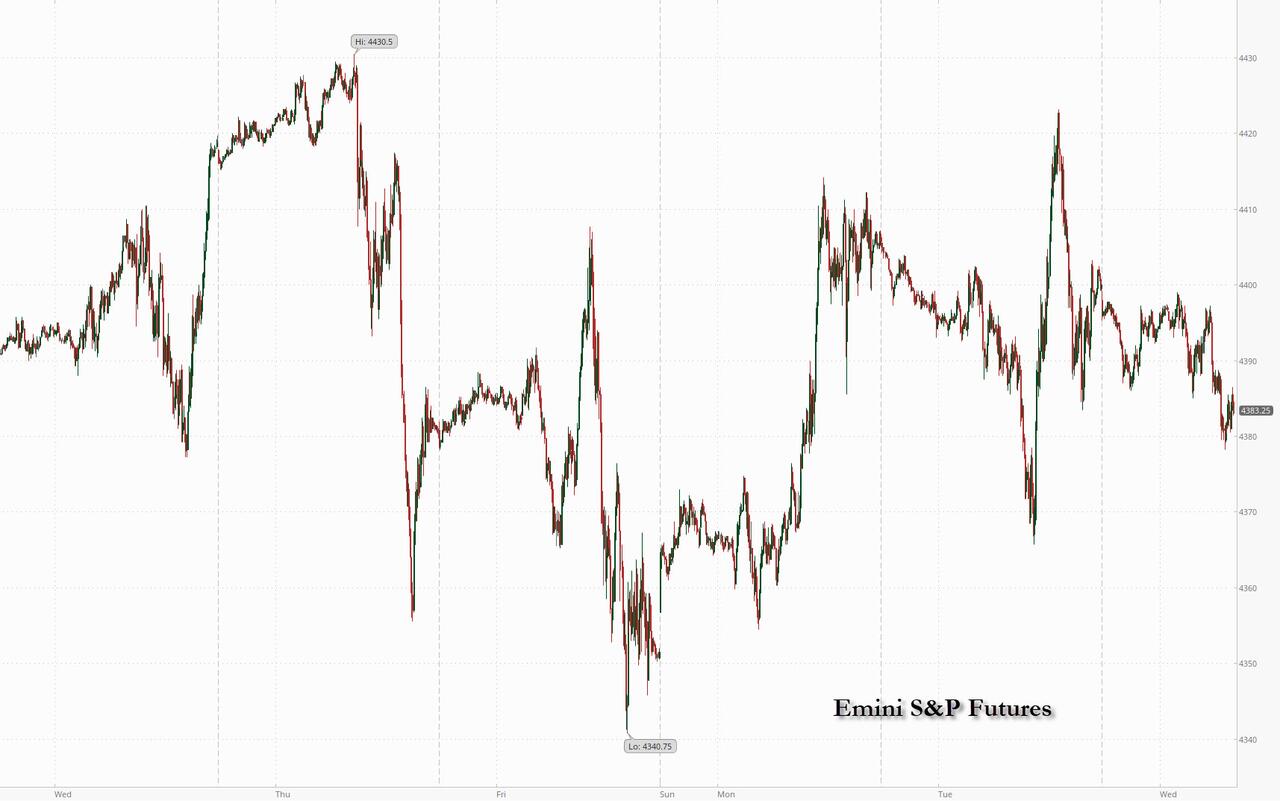

SPX futures declined to a morning low of 4350.70 thus far. SPX has not been able to overcome the 50-day and 100-day Moving Averages. However, it has rose above Intermediate resistance at 4383.76, then declined beneath it, creating an aggressive sell signal. A decline through the next support at 4337.00 confirms the sell signal. The Master Cycle high may have been made yesterday at 4393.57 on day 257. Should that be accurate, the new Master Cycle allows an approximate month of decline.

Today’s op-ex shows Max Pain at 4355.00. Long gamma begins at 4370.00 while short gamma may begin at 4350.00. There are over 6000 put contracts at 4300.00, a level to watch closely.

ZeroHedge reports, “US equity futures and global markets dropped, while gold surged and crude oil futures spiked as much as 3% to fresh weekly highs as the conflict in the Middle East escalated sharply despite Biden’s visit to Israel seeking a normalization in tensions, as Arab leaders canceled a summit with US President Biden and as Iran intensified its war of words against Israel. As of 7:45am, S&P 500 and Nasdaq 100 futures lost more than 0.4%, after yesterday’s flat close. Crude’s surged after the foreign minister of Iran, a major oil exporter albeit embargoed, called for an embargo against Israel. Gold prices rose as investors snapped up haven assets.”

VIX futures rose to 18.55 this morning, just beneath the trendline. VIX is on a buy signal which may be reinforced above the trendline at 18.60. The Cycles Model suggests the VIX may rally from one month to six weeks.

Today is monthly options expiration in the VIX. Maximum investor pain is at 19.00. Short gamma extends from 18.00 down to 14.00. Long gamma begins at 20.00 and extends to 47.50.

USD futures continue to consolidate beneath the Cycle Top resistance at 106.35. All indications are that the Master Cycle made a low on October 13. Should that be correct, the rally may resume imminently, as trending strength resumes by the weekend.

TNX surged to a new high this morning, challenging the October 6 high at 48.87. Today is day 258 of the (old) Master Cycle. There is an outside chance of a brief reversal here before resuming the rally. In either event, the probability of a new high today is large due to trending strength.

RealInvestmentAdvice gives the bullish case for bonds, “Treasury yield levels are overwhelmingly a function of inflation. However, in the short run, a plethora of influences can explain deviations between yields and inflation. These factors, which we call noise, are significant for short-term traders but can hide tremendous opportunities for long-term investors.

As we witness, bond market noise can be deafening. The horror-ridden narratives explaining the sudden rise in yields are compelling. They can steer even the best traders away from a golden opportunity.

For those bullish on bonds, separating the noise from the signal is difficult. But, doing so allows you to alleviate short-term stress when bond prices move adversely. Additionally, it helps maintain confidence in long-term fundamental prognostications. ”

Crude oil futures rose to 88.57 in the overnight market as it probed toward its Cycle Top at 90.33. The corrective swings are wide and have moved back beneath Intermediate support at 87.55. There is a probability of yet another probe at the Cycle Top resistance. However, a sell signal may be generated beneath the 50-day Moving Average at 85.44.

ZeroHedge observes, “Oil prices spiked on Wednesday morning after Iran called for an oil embargo against Israel over its air strikes on Gaza. Iranian Foreign Minister Hossein Amirabdollahian said there should be an “an immediate and complete embargo on the Zionist regime by Islamic countries, an oil embargo against the regime,” Bloomberg reported citing a ministry statement on Telegram. He also urged Muslim countries to expel Israeli ambassadors.

Amirabdollahian made the comments in Saudi Arabia at a summit of the Organisation of Islamic Cooperation, called to discuss the Israel-Hamas war. The comments came as US President Joe Biden arrived in Tel Aviv in a bid to calm regional tensions and support Israel.

Oil traders are increasingly concerned that Israel’s war on Hamas will spread and potentially draw in Iran and its allies such as Hezbollah in Lebanon.”