3:15 pm

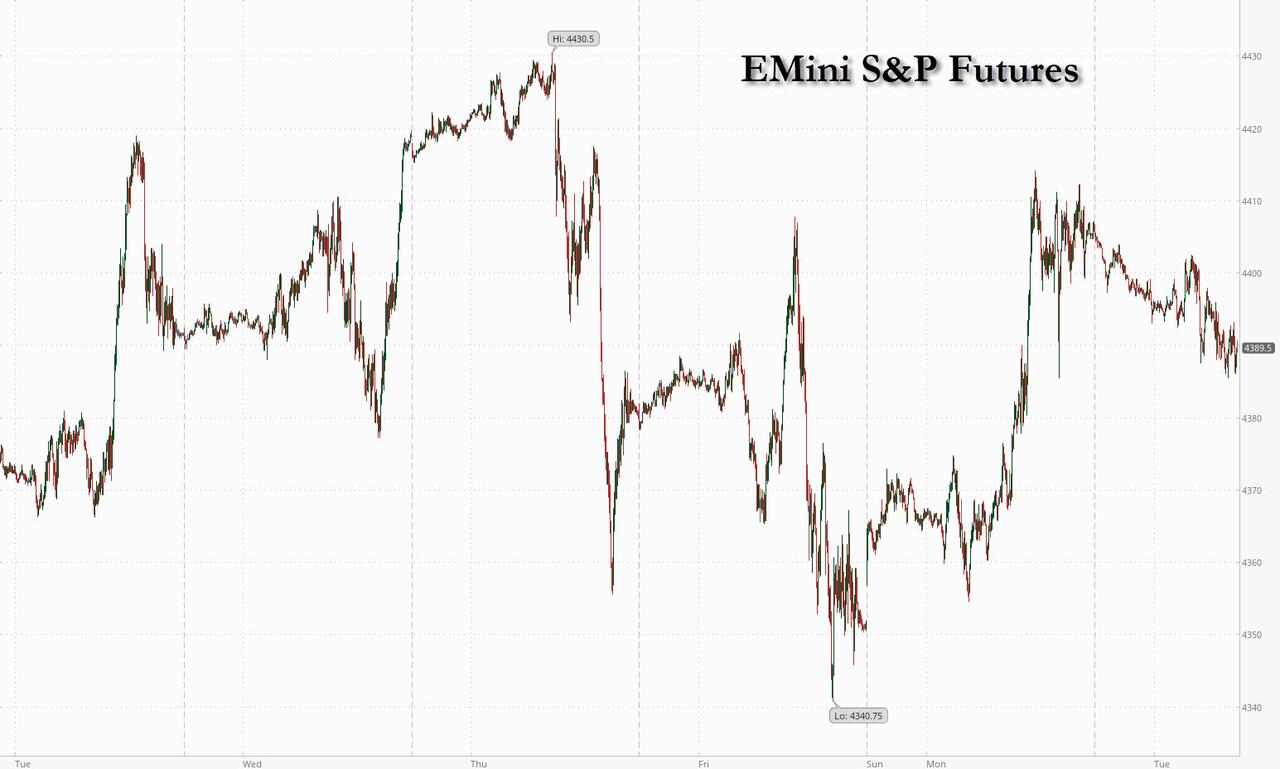

SPX exceeded Intermediate resistance at 4383.75 while making an attempt to test the 50-day Moving Average at 4402.75, but fell short of that target. This has all the earmarks of a final probe in the Master Cycle on day 257. A reversal beneath Intermediate support/resistance may produce a an aggressive sell signal. The rally may simply be running out of time.

ZeroHedge comments, “American investors have been taken for a trillion-dollar ride by naked short sellers, in what could turn out to be the biggest financial regulatory scandal in North American history.

While what is now an all-out war on naked short sellers intensifies, there is a new flashpoint on the front line–a potentially devastating ruling targeting those who are alleged to make illegal naked short selling possible: The Facilitators: bankers and brokers.”

9:52 am

BKX, our liquidity proxy, remains persistently elevated primarily due to the healthier. larger banks’ positive earnings reports, thanks to the Fed allowing the money center banks to pick and choose which assets they will assume from failed banks. While the large banks are staying afloat with burgeoning held-to-maturity (HTM) loans, smaller banks do not have that capability. In addition, long-term yields are resuming their rally, compounding the problem. The Cycles Model and associated technical markers imply a waterfall event in the making.

ZeroHedge observes, “Bank of America, the second largest US bank, was the latest big money-center bank to report earnings this morning, and in keeping the trend started by JPM, Wells and Citi last Friday, it not only beat expectations, but reported Q3 numbers that were the strongest in at least seven years as net interest income topped analysts’ estimates as the lender continues to reap the benefits of Federal Reserve interest-rate hikes and market swings.

Here are the highlights:

- Q3 revenue $25.17BN, up 3% YoY from $24.5BN and beating exp. of $24.94BN

- Q3 EPS $0.90, up 11% YoY from $0.81, and beating exp. of $0.82

8:20 am

Good Morning!

SPX futures have declined to 4356.50 thus far on day 257 (of a potential 258 day Cycle). Thus far, three attempted probes higher have been stopped by Intermediate resistance now at 4387.52. The 50-day Moving Average at 4405.41 provides additional resistance, should a final attempt be made to break through.

Today’s options expiration shows 4365 gives Maximum Pain to options investors. Long gamma starts at 4375.00 while short gamma begins at 4340.00.

ZeroHedge reports, “US index futures slid and global markets dropped as yields rose to session highs as complacent investors once again pressed hopes that the Israel-Hamas war could be resolved diplomatically, after Joe Biden said he will travel to Israel to “show his support”, which in turn shifted attention back to the untenable US fiscal situation which meant the blowout in yields would continue. At 8:15am S&P futures dropped 0.3% as traders assessed a flurry of major earnings. 10Y TSY yields rose to a high of 4.76%, spiking 20bps in the past two days and undoing much of the “flight to safety” after the Israel war. The dollar steadied, while the pound fell after cooling UK wage growth reduced pressure on the Bank of England to raise interest rates further. Israel’s shekel gained after weakening past 4 against the greenback on Monday. Brent crude oil traded near $90 a barrel.”

VIX futures have risen to a morning high of 17.98 thus far. It is on a buy signal (accumulation phase). The probability of a deeper low is diminishing by the day after a near-Fibonacci retracement of 61.8%.

Tomorrow’s op-ex shows 19.00 heavily subscribed by both puts and calls and may be the Max Pain position. Short gamma occupies a wide swath between 14.00 and 18.00. Long gamma begins at 20.00 and is heavily subscribed to 47.50. This has the potential of a runaway train.

ZeroHedge comments, “The rising wall of corporate loans and debt to be refinanced will increasingly stress company balance sheets, leading to a secular rise in equity volatility.

Tensions in the Middle East are adding uncertainty to the outlook. What does that mean for volatility? So far it has led to at least a temporary rise in equity-market volatility, but in recent years any increase has been fairly short lived, despite the sort of catalysts that would be expected to keep it persistently elevated.

Greater uncertainty, therefore, does not necessarily lead to greater volatility. However, a much surer reason why it is destined to see a structural rise in the coming quarters is mounting evidence that the credit cycle is nearing its late stages.”

TNX has risen to a morning high of 48.13 thus far and may be testing the October 6 high today. TNX may have made its Master Cycle low on October 12. Today is a high trending strength day, giving it the ability to break out of any resistance.

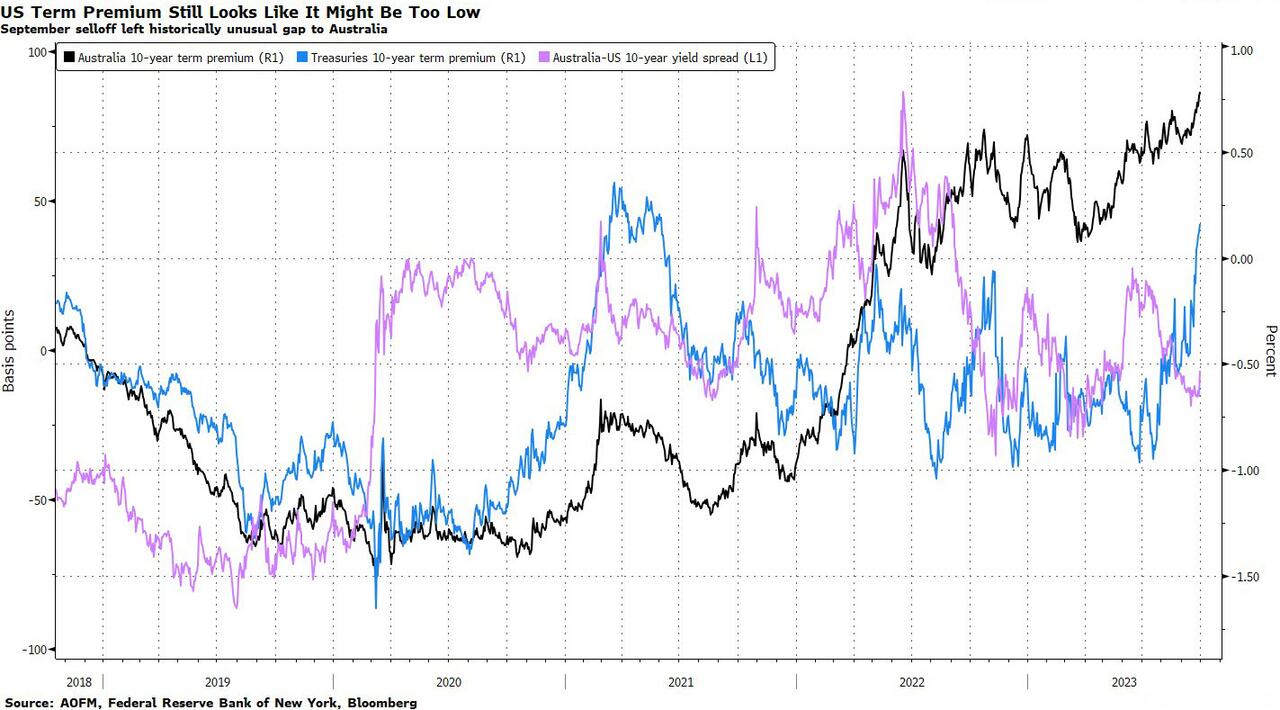

ZeroHedge comments, “Treasuries’ recent slump owed plenty to the return of the so-called term premium as investors became more concerned about the risks of holding longer-dated debt. Even as US bonds get some help from geopolitical uncertainty, there’s plenty of scope for yields to march considerably higher on the same dynamics that helped drive September’s spike.

For one thing there’s little chance that the supply outlook is going to improve noticeably, no matter how the Middle East conflict and the US House speaker situation are resolved. For another, an examination of the relative yields for Australian and US debt signals there’s potential that US term premiums have further to go to.”

USD futures emerged from a morning low of 105.90 and surged to a morning high of 106.31 thus far. A Master Cycle low may have appeared on October 12, day 253 of the master Cycle.

Crude oil futures have declined to a morning low of 84.75, having declined beneath the 50-day Moving Average at 85.25 and confirmed its sell signal. The Cycles Model suggests a possible 5-week decline in crude prices while analysts predict oil rising to $150.00.

OilPrice.com reports, “Oil is on track to be the largest export item for the United States this year for the first time in history, highlighting the growing influence of U.S. oil production and exports on the global oil market.

Rising U.S. crude oil production in recent years and growing exports after the ban was lifted in 2015 have made U.S. oil an increasingly important commodity on the market, especially after the Russian invasion of Ukraine and the ban and sanctions on Russian crude in the West. ”

Gold futures are challenging the October 13 high at 1944.30. Today is day 257 of the (former) Master Cycle. Chances of making a nominal new high are slim. Should the reversal get underway, a decline to the end of the year is forecast by the Cycles Model.