1:30 pm

SPX may have been stopped by the trendline at 4339.50,a 47% retracement VS. a 61.8% Fibonacci retracement mentioned this morning. The decline may be resuming.

8:00 am

Good Morning!

NDX futures made a new low at 14828.00, then bounced back above the close. The Cycles Model suggests another 3-4 weeks of decline before a possible correction. NDX is on a sell signal beneath the 50-day Moving Average at 15059.00.

Today’s options expiation shows Maximum investor pain at 14940.00. Long gamma starts at 14975.00, while short gamma begins at 16930.00 with a put wall at 14900.00.

ZeroHedge notes,”Stock investors had looked pretty impervious to risk aversion until recently.

But with yields pushing higher, they have started making an about-turn. An escalation of the conflict in the Middle East may just be what sends indexes back to fair value, and that would mean a drop of 14% for the Nasdaq 100.”

SPX futures continued their decline to 4294.00 before making a bounce. This may be a typical retracement to 4355.00 which may lend an opportunity to sell/short the bounce. The Intermediate resistance is at 4377.00 as an alternate target.

Today’s op-ex shows Max Pain at 4345. Long gamma begins at 4350.00 while short gamma starts at 4320.00. The dealers’ game is to keep SPX between long and short gamma with a close at or near Max Pain.

ZeroHedge reports, “Futures dropped and global markets slumped again after treasury yields continued their relentless march higher (until something breaks), draining appetite for stocks as traders tracked earnings news and an intensifying diplomatic push to contain the Israel-Hamas war. Yields on 10-year US government bonds gained for a fourth day, pushing them just shy of 5% for the first time since 2007, while 30Y yields are well above 5% now. Many potential drivers for price action Thursday include weekly jobless claims data and a packed Fed speaker slate headed by Chair Powell at 12pm New York time…

… while the ridiculous explosion in US debt which has increased by over $600 billion in one month, or about $20 billion per day, is not helping.

VIX futures rose overnight to 20.29 before a pullback. Support may be found at the mid-Cycle support at 17.17. VIX is on a buy signal and any pullback offers an opportunity to accumulate shares.

Next Wednesday’s op-ex shows Max Pain at 18.00. Short gamma has virtually disappeared, while long gamma begins at 20.00. Pockets of longs extend to 50.00 as sentiment gradually changes.

ZeroHedge remarks, “In a market where trader exhaustion is now pervasive and palpable and certainly far greater than the subdued level of the VIX would indicated because, as noted earlier, the gap between the intraday VIX (thanks 0DTE) and the close-to-close VIX has never been greater…”

TNX futures surged to an overnight high of 49.87, nearly making the Head & Shoulders target. This formation was first noted in early August when TNX broke above the neckline. This trend may continue for another 4-6 weeks, according to the Cycles Model. US government debt is crowding out all other avenues of financing.

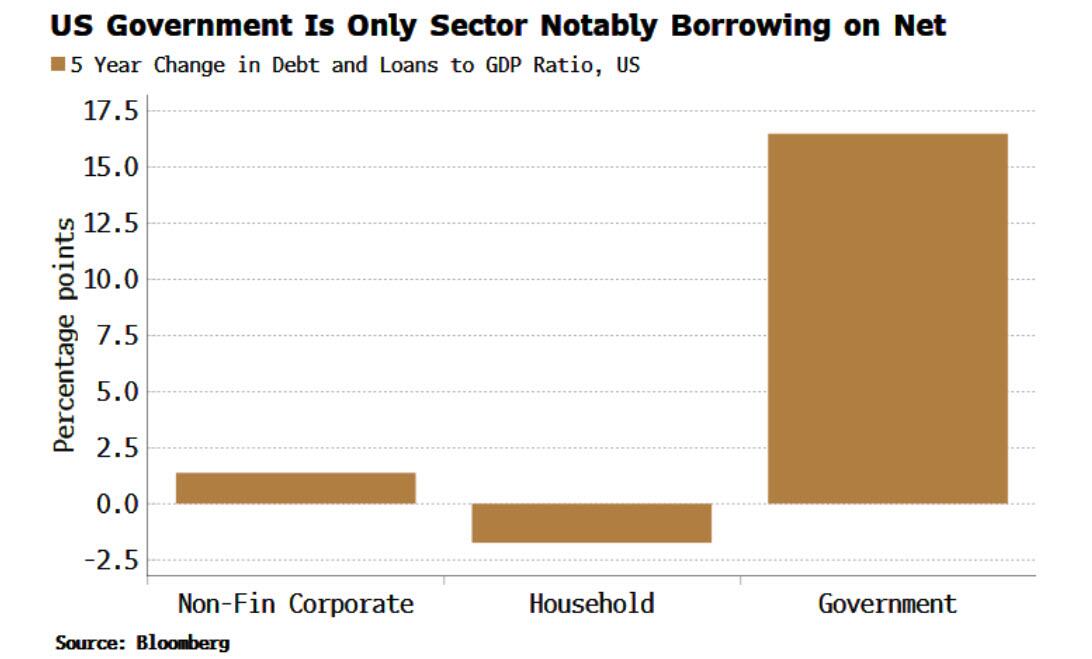

ZeroHedge remarks, “The US government is the only sector to have notably borrowed on a net basis over the last five years. The market sees that as inflationary, driving yields higher.

The pandemic saw an increase in the borrowing of all sectors. But it was the government that saw the biggest rise in GDP terms, and it is the government whose debt is still considerably higher than it was before the pandemic – the debt-to-GDP ratio is up 16 percentage points over the last five years.

In contrast, the household sector’s leverage is now lower than it was pre-pandemic, while the corporate sector’s is only marginally higher. The US government has become the borrower of first as well as last resort.

The market is picking up on this and is pricing accordingly. We can decompose nominal yields into a sum of expected short rate + real term premium + expected inflation + inflation term premium (see here for more).”

ZeroHedge further elaborates, “$1.2bn per hour

“….US debt adding around $28.5bn per day for 18 days in a row….or put a different way increasing that debt burden by $1.2bn per hour and likely to increase that total debt bill by around $1 trillion in around 6 weeks” (GS trading desk)

Bonds down 3 years in a row

Looks like it at least… The 10-Yr Treasury bond is down 5% this year, on pace for its 3rd consecutive annual decline. With data going back to 1928, that’s never happened before. The worst 3-year period for bonds prior to now was 1978-1980 w/ a 3% loss for the 10-Yr. What’s the 2021-23 decline? -26%. (Bilello)”

USD futures declined to an overnight low at 106.11, which is beneath the Cycle Top at 106.48. This may be an indication of a further decline to the 50-day Moving Average at 104.78 to complete the correction in the next few days.

Crude oil futures declined to an overnight low of 85.50, testing the 50-day Moving Average at 85.41. There may be a final attempt to test the Cycle Top at 90.44. A failure to overcome this resistance may result in the resumption of the decline. A confirmed sell signal lies beneath the 50-day at 85.41.

ZeroHedge remarks, “A panicking Joe Biden has realized that his best friends, now that oil prices are soaring again and the SPR remains largely drained, are tinpot banana-republic “dictators” (in the White House’s own words) like Venezuela’s Nicolas Maduro, and on Wednesday the White House suspended sanctions on Venezuelan oil, gas and gold production. But since it would be too corrupt even for Biden to drop sanctions on Maduro in exchange for just a few barrels oil and nothing else, the White House pretended that the deal was in exchange for “promoting democracy”, and In return the Nicolas Maduro government promised a deal with the opposition that could see elections held next year. Which likely means 100% mail-in ballots and Dominion machines to “count” them.”