10:25 am

The Ag Index may be pulling back after testing the 50-day Moving Average at 399.18. A probe above the 50-day reinforces the existing buy signal given off the trendline. This is an indication to accumulate shares of agricultural products and companies.

10:10 am

BKX remains upbeat on day 256 of the Master Cycle, suggesting another probe higher, possible to Intermediate resistance at 79.09 or the 50-day Moving Average at 80.72. Expect to see a waterfall event to follow. The decline may continue through the first week of December.

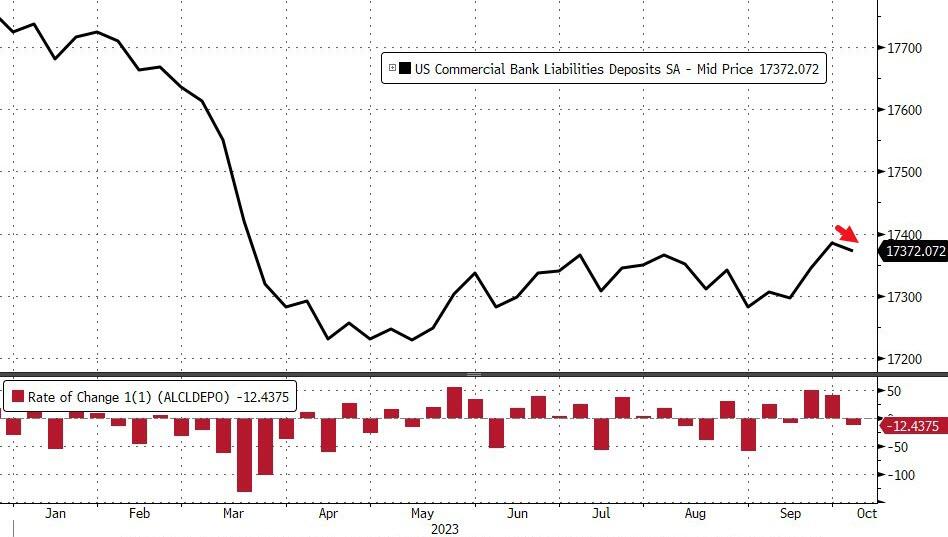

ZeroHedge reports, (after Friday’s close), “Retail money-market funds inflows continued this week, and more troubling (ahead of the coming regional bank earnings), usage of The Fed’s emergency funding facility jumped to a new record high over $109BN. Big banks had a good day today on earnings.

That’s the not-so-rosy picture ahead of tonight’s bank deposit data debacle from The Fed.

On a seasonally-adjusted basis, total deposits declined by $12.4BN (after two big weekly deposit inflows)…

8:00 am

Good Morning!

NDX futures rose to a weekend high of 15066.40, remaining beneath the 50-day Moving Average at 15074.41 and on a sell signal. Thursday’s high at 15333.98 may have been the Master Cycle high, on day 252. Should that be the case, we may see the decline gain momentum by Wednesday. Today is day 256 of the (former) Master Cycle. A new Master Cycle may have begun that may last up to six weeks.

Today’s op-ex shows Maximum Investor Pain at 15010.00. Long gamma may begin at 15025.00 while short gamma starts at 15010.00.

ZeroHedge observes, “Apple shares fell in premarketing trading in New York following research indicating that iPhone 15 sales in China lagged behind its 2022 predecessor.

Bloomberg cited a new report from market tracker Counterpoint Research that showed iPhone 15 sales were down 3.5% compared with iPhone 14 over the first 17 days after launch.

Counterpoint said the new iPhone’s sales slump in China was due to a weakening economy. It noted that in the US, iPhone 15 sales were likely to see double-digit growth over the first nine days of sales in 2022 for the iPhone 14.”

SPX futures reached a weekend high of 4347.30 thus far, staying well beneath the 100-day Moving Average at 4392.15. In addition, not only has the Intermediate support/resistance fallen beneath the 100-day, but the 50 day Moving Average is at 4408.00 and threatens to decline beneath the 100-day in a bearish cross, as well. This may be a basis for a sell signal in the SPX. Note that there may be a brief foray to the 50-day Moving Average in the next few days before turning down. Should this take place, it may set up a clean sell signal.

Today’s op-ex shows Max Pain at 4330.00. This is a tightly wound options market, with long gamma beginning at 4335.00 and short gamma starting at 4325.00.

ZeroHedge reports, ” US index futures are European bourses reversed earlier losses and traded higher, led by small-caps, as Treasuries resumed their slide after Friday’s gains while oil dropped on hopes that a diplomatic solution may emerge to the Israel-Hamas conflict: Secretary of State Blinken has returned to Israel and Joe Biden could follow on Wednesday or Thursday according to unconfirmed reports, as they seek to avoid an escalation. As of 7:45am, S&P futures were 0.3% higher while Nasdaq 100 futs gained 0.1% after declines on Wall Street at the end of last week. The US Dollar started the session lower and commodities came for sale across all three complexes. Brent crude oil held near $91 a barrel, after surging almost 6% on Friday. Gold fell but bitcoin surged.”

VIX futures declined to 18.52 over the weekend, remaining above the trendline thus far. However, it may decline further to 17.50, giving another opportunity to buy the dip. VIX remains on a buy signal and may remain there until the end of November.

Wednesday’s op-ex shows Max Pain at 19.00. Short gamma exists between 18.00 and 14.00. Long gamma starts at 20.00 and extends to 47.50 in six-figure holdings.

ZeroHedge observes,”The geopolitics hedge

Oil volatility is the outperformer on the Mid East situation, although gold volatility is not far behind. Chart shows oil volatility (OVX), bond volatility (MOVE), gold volatility (GVZ) and VIX since September 11.

Source: Refinitiv

Do we see a close above 20?

VIX continues working on the most recent track record. It hasn’t closed above 20 in 102 consecutive sessions…

TNX futures rose to a new weekend high at 47.10 before pulling back. Thus far, Thursday’s low at 46.32 appears to be the Master Cycle low. However, today is day 256, leaving a few more days to verify that event. There is an outside chance for TNX to decline further to Intermediate support at 44.60 or the 50-day Moving Average at 43.66 in the next few days, so stay alert.

ZeroHedge remarks, “Poor liquidity in the Treasury market is contributing to a rise in implied and realized fixed-income volatility. A re-increase in inflation volatility means this dynamic is likely to persist.

Despite being one of the deepest markets in the world, the market for Treasuries has seen liquidity deteriorate in the years since the pandemic. On several measures – bid/offer spread, order-book depth, price impact of a trade – the Treasury market has shown marked signs of a decline in liquidity in recent years.

Bloomberg’s US Treasury Liquidity Index measures liquidity by comparing where yields are to where they “should” be based off a fitted curve. The greater the average of the yield errors across the curve, the worse liquidity is likely to be.”

USD futures have declined to a weekend low at 106.12, beneath the Cycle Top support at 106.28. This suggests another move lower, perhaps to the 50-day Moving Average at 104.54. Today is day 257 in the Master Cycle, running it close to the end. The Cycles Model suggests the new Master Cycle may be running strong by the weekend.

Crude oil futures dropped to a weekend low of 85.67, balling beneath Intermediate support at 87.23. This puts investors on high alert for a sell signal, to be confirmed beneath the 50-day Moving Average at 85.12. The Cycles Model infers that the decline may last to the end of November.