11:02 am

SPX is probing lower today. A potential sell signal awaits beneath Wednesday’s low at 4325.43. TNX is recovering after testing its Cycle Top support, which suggests we may see higher yields today. The market may fall apart as the day progresses.

10:08 am

The Ag Index may be reiterating its buy signal by exceeding its 50-day Moving Average at 391.33. I have been advocating “accumulating” shares of agriculture products and companies for the past two months, as they may be a long-term buy.

KSAL.com reports, “A former U.S. ambassador who helped to negotiate an iconic agricultural trade agreement with China said that America’s farmers have a bright future if the industry can capitalize on available opportunities for exports, technology and value-added products.

But Gregg Doud – currently the president and Chief Executive Officer of the National Milk Producer’s Federation – said each has its own set of challenges as the U.S. balances world politics and intense competition in the global food market.

“You live in a world today, folks, where total U.S. agricultural exports to the world are about the same as China’s total food imports from the world,” said Doud, in remarks as the 10th speaker in Kansas State University’s Henry C. Gardiner Global Food Systems lecture series on Oct. 9.”

9:55 am

BKX, our liquidity proxy, is on the cusp of a severe decline, larger than that seen in March. The “good stuff” has been announced in JPM’s stellar earnings. This may be followed by the “less good” announcements during the remaining market hours and the horrible announcements after hours. The following article is worth a read in its entirety.

ZeroHedge reports, ” As happens every quarter, moments ago JPM – the largest US bank – officially fired the starting gun on Q3 earnings season when it reported earnings which – courtesy of the bank’s taxpayer-funded g(r)ift of First Republic earlier this year – were stellar, beating on the top and bottom line, and despite some weakness (in equity sales and trading) and some gloomy comments from CEO Jamie Dimon, were well received by the market: it is the other US banks, and especially the smaller ones, that are a far more concerning prospect, while JPM once again validates its “fortress balance sheet” especially with the benefit of the recent taxpayer-funded fortressization in the form of acquiring all First Republic good assets.”

8:05 am

Good Morning!

NDX futures slipped down to 15092.00 this morning as the rally loses its grip. Key support lies at the 50-day at 15088.33, below which a sell signal is generated. While the NDX may keep some equilibrium today, the Cycles Model suggests a likely downdraft generated over the weekend. This implies market-moving announcements may be released after hours.

Today’s options expiration shows Maximum Investor Pain at 15125.00. Long gamma may prevail above 15150.00 while short gamma begins at 15100.00.

ZeroHedge remarks, “Rates are back

Massive up candle in the 30 year as rates spike even higher post the latest auction. Today’s candle is much bigger than yesterday’s down candle. Note we almost touched the 21 day earlier today.

Source: Refinitiv

Rates stress remains intact

The gap between the VXTLT and the VIX stays wide. Looks like rates stress has decided to follow the higher for longer path as well…”

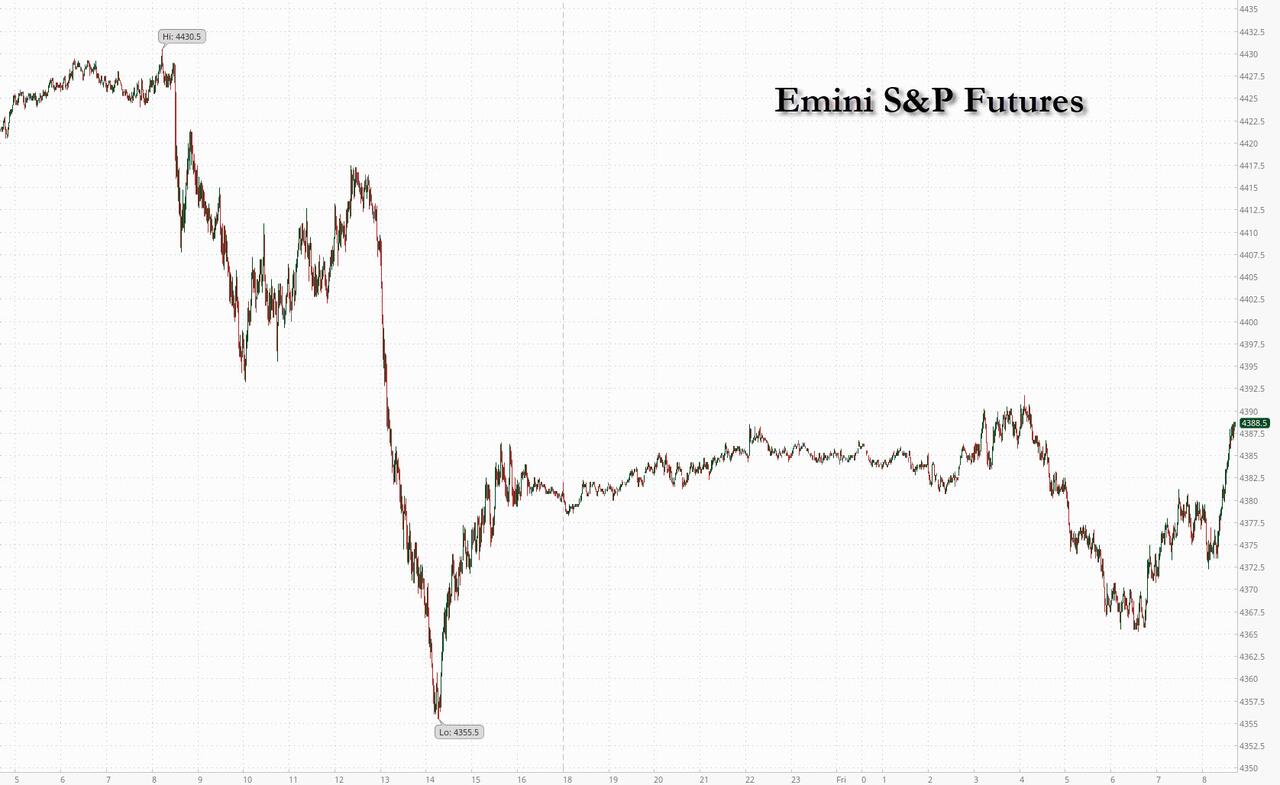

SPX futures are consolidating this morning, currently at 4335.40. SPX was turned back at the Intermediate resistance at 4391.47, indicting the significance of the overhead resistance cluster. In addition, Intermediate resistance has made a death cross with the 100-dy Moving Average, signifying downside momentum.

Today’s op-ex shows Max Pain at 4330.00. Long gamma begins at 4350.00, while short gamma starts at 4300.00.

ZeroHedge reports, “US equity futures reverased earlier losses, thanks to solid results from JPM and Citi…

… while treasuries rallied with 10Y yields tumbling more than 10 basis point to session lows below 4.59% and paring almost all of Thursday’s sharp rise in the wake of hotter-than-expected US consumer price data.

VIX futures rose above the mid-Cycle support/resistance at 17.20, reinstating its buy signal. The Cycles Model implies a period of strength may begin today and may influence the VIX over the next two weeks.

Next Wednesday’s op-ex shows Max Pain at 18.00. Beneath that are massive sort holdings extending down to 14.00. Long gamma begins at 20.00 and now extends in six-figure holdings to 45.00.

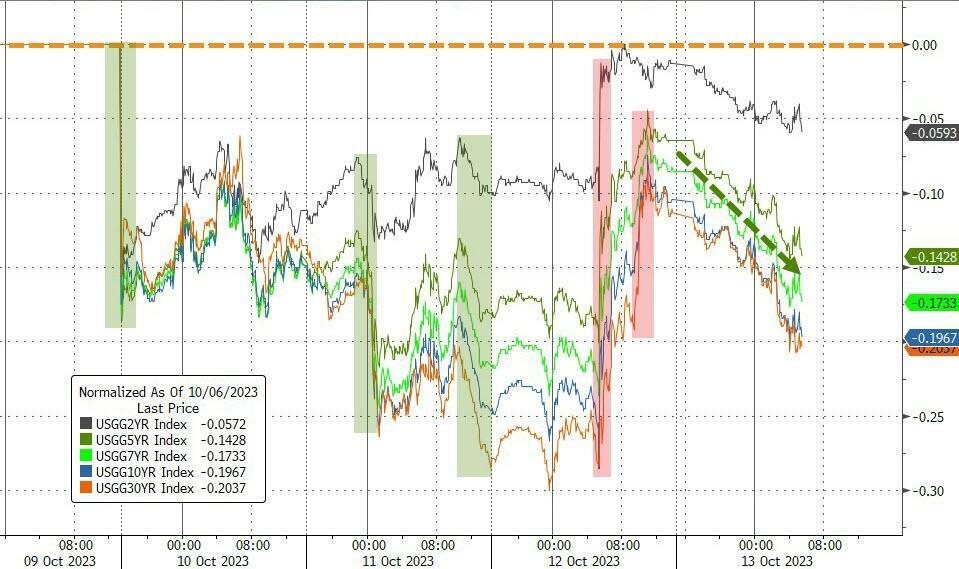

TNX is testing the Cycle Top support at 46.00 this morning after its blow-out rally yesterday. Rate jitters are getting extreme, especially after yesterday’s “Horrific” 30-year auction.

ZeroHedge remarks, “After two ugly, Dealer-heavy auctions, moments ago the Treasury concluded the week’s coupon issuance with the sale of $20 billion in 30Y paper, and boy was it ugly.

The auction, a reopening of 29-Year 10-month cusip TT5, priced at a high yield of 4.837%, which was almost 50bps higher than just last month’s 30Y auction (which priced at 4.345%). This was not only the highest stop on a 30Y auction since August 2007, but it tailed the When Issued 4.800% by 3.7bps, the 4th consecutive tail and the biggest since Nov 2021 when we saw a record 5.1bps tail, and the 3rd biggest tail on record.

The bid to cover was ugly, coming at 2.349, the lowest since February. and well below the six-auction average of 2.44%.”

USD futures are currently testing the Cycle Top support at 103.20. It may be breached in favor of the Intermediate support at 105.24 today. However, the Cycles Model implies a higher high may be due in the next week.

Crude oil futures spiked higher today, testing Intermediate resistance at 87.00. The Cycles Model is neutral in the short term. However, normal retracements may allow a probe to the Cycle Top at 90.07 before reversing lower.

ZeroHedge reports, “While the dollar is relatively flat overnight, both gold and crude are soaring (and bonds bid) as fears of what lies ahead this weekend in Israel and Palestine spark risk-off around the world.

The dollar has gone nowhere since reaching last Friday’s pre-payrolls level…

The Israel-Hamas war hasn’t had any direct effect on global oil supplies and flows so far, but traders are wary that the conflict could disrupt transportation through vital chokepoints or lead to tougher restrictions on Iranian exports. Additionally, the US tightened sanctions on Russian crude exports, which exacerbated concerns about supplies…”

Gold futures punched higher to 1932.00 this morning, crossing the 50-day Moving Average at 1928.00. Additional resistance lies at the mid-Cycle line at 1944.26. The Cycles Model suggests that the rally may come to an abrupt end in the next few days, leading to a possible decline to the end of the year.