10:39 am

SPX has declined beneath its Short-term support at 4125.77, creating an aggressive sell signal. Further confirmation of the sell signal may come at the trend channel lie at 4075.00 and the mid-Cycle support at 4061.89.

ZeroHedge reports, “Weak JOLTS?, Poor factory orders, a sudden realization of the urgency and seriousness of the debt ceiling debacle, Europe back from vacation, or just pre-FOMC jitters?

Who knows to be frank but everything went just a little bit turbo, starting with a total collapse in regional banks…

And despite the Biden admin claiming that FRC was just another ‘outlier’ business model, PacWest, Western Alliance, and Zions (among others) are in a freefall…”

9:37 am

BKX has slipped beneath its Cycle Bottom support at 79.32, confirming the sell signal. Yesterday’s move may confirm downside strength for this index. If so, we may see the decline intensify through mid-June.

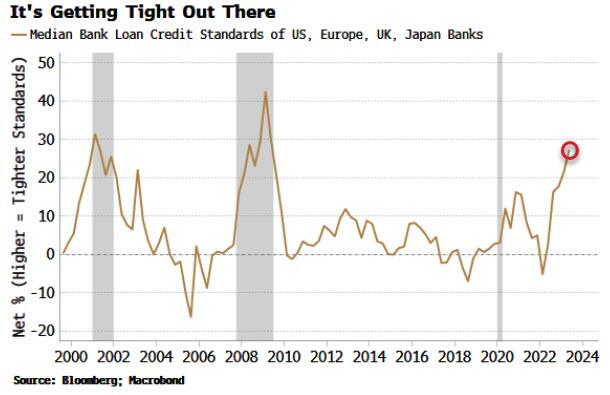

ZeroHedge notes, “A composite measure of DM banks’ lending standards shows they are the tightest since 2009. Tighter credit conditions will be an impediment to central banks’ preference to keep rates “higher for longer.”

The ECB’s bank lending survey was released this morning, with banks further tightening their credit standards.

This has pushed an aggregate measure of bank-loan credit standards to levels not seen since the Lehman crisis.”

7:30 am

Good Morning!

NDX futures have been consolidating in place in the overnight market on day 259 of the current Master Cycle. The current Wave structure puts a target on this move near 13400.00. The 2-hour trading Cycle top is at 13403.37. Cycles may be stretched, for good reason. The markets may be waiting for the FOMC announcement.

Today’s op-ex sows Maximum Pain for options investors at 13180.00. Long gamma may begin at 13200.00, suggesting investors/dealers are comfortable being long up to 13500.00. Short gamma begins at 13130.00, but does not have any depth.

ZeroHedge suggests, “NASDAQ does not care

Did you see the move in the 30 year yesterday? Goldman’s Nocerino reminds us: “The last time the 30yr had a move like this was 06/13 – the SPX fell 3.88% and Non-Profitable Tech fell 8.7%…” Yesterday was pretty much another flat day for equities…”

Source: Refinitiv

SPX futures are also consolidating in a narrow range. The current Master Cycle may have completed yesterday, day 258, but the signs of a reversal have not appeared.

Today’s op-ex shows Max Pain at 4165.00. Long gamma begins at 4190.00, while short gamma starts at 4150.00. There seems to be little conviction for either puts or calls.

ZeroHedge reports, “US index futures saw modest declines on Tuesday as investors braced for this week’s Federal Reserve meeting where policymakers are expected to deliver another rate increase, and then pause the hiking cycle. S&P 500 contracts slid 0.1% as of 8:00 a.m. ET after earlier swinging between small gains and losses. Nasdaq 100 futures traded little changed. Both benchmarks closed steady on Monday after data showed that US factory activity contracted for a sixth-straight month in April, the longest such stretch since 2009.”

VIX futures are testing yesterday’s high after making a new Master Cycle low on day 262. The Wave structure is complex, but appears to be complete. An aggressive buy signal may be imminent, while confirmation lies above the 50-day Moving Average at 20.04.

Tomorrow’s op-ex shows Max Pain at 16.00 with minimal puts beneath it. Long gamma starts at 20.00 and remains strong to 33.00.

ZeroHedge comments, “Yesterday we laid out a tactical summary of the near-term market direction catalysts as a tug of war between several distinct forces: on one hand, risk could be propelled higher thanks to i) the return of buybacks, ii) the much stronger than expected Q1 earnings season, and iii) the “peak Fed narrative” following this week’s final Fed rate hike; on the other hand, bears were betting that i) “sell in May and go away” would work this year as it has in previous years, that ii) the widely discussed collapse in market breadth would lead to a sharp market drop as it has on all previous occasions, and iii) that the coming debt ceiling crisis would require a sharp market drop to force a paralyzed Washington into action.

Finally, the fact that a recession of some sort is inevitable was cited by Goldman as a fundamentally bearish catalyst over the medium-term.

However, looking at the market structure, so far the bulls are winning, and not just because of Friday’s epic 0DTE call-driven squeeze-o-rama: as Goldman’s start derivatives trader writes in a note published today in which he looks at the “greenshoots of the right tail chase”, Friday was the fourth largest SPX Call session in history with some $600bn in call volume traded!”

TNX pulled back beneath the 200-day Moving average at 35.45. It may have embarked on a 2-moth rally to a higher yield that may not be recognized until it breaks above the 50-day Moving Average. The Cycles Model suggests it may do so in the next week.

ZeroHedge remarks, “In a long-awaited update from Janet Yellen, shortly after the close, the Treasury Secretary sent a letter to Congress in which she said that as a result of the recent slowdown in tax receipts (extensively discussed here), the Treasury could run out of emergency debt-limit measures (i.e., hit the infamous X-Date) as soon as June 1 absent a debt-ceiling deal, a revision to her previous Jan 13 letter in which she said that it was “unlikely that cash and extraordinary measures would be exhausted before early June.” In other words, Congress has exactly one month to get a deal to raise the debt limit – which of course won’t happen without the market first plunging enough to prompt the extremely polarized chamber into action.”

USD futures rose to 102.10 this morning, crossing above the Intermediate-term resistance at 102.01. This may confirm the aggressive buy signal coming off the Master Cycle low. The Cycles Model suggests a rising USD to the middle of June. Crossing the 50-day Moving Average at 102.88 may add further confirmation to the rally.

Gold futures are bouncing off the Intermediate-term support at 1992.36. The failure to rally out of the Master Cycle low on April 20 may be suggesting further downside may be imminent. If so, the decline may continue through the middle of June.

Crude oil slipped back beneath the 50-day Moving Average at 76.50 and the trendline near 75.00 to reiterate its sell signal. The Cycles Model suggests at least tree more weeks of decline. There is a possibility of another new low in that time.

OilPrice.com reports, “Western tanker insurers are concerned that they may inadvertently help ship Russian crude oil above the $60 per barrel price cap as purchases and transactions have become opaque since the G7 introduced the price ceiling in early December 2022.

Protection and indemnity (P&I) clubs have attestation that the shipments they are covering have not been bought above the price cap, but they are wary that increasingly evasive practices by Russia and its new crude customers may obscure the actual price at which Russian crude cargoes are being traded.”