7:00 am – I am posting early as I am taking two grandsons to the airport this morning.

Good Morning!

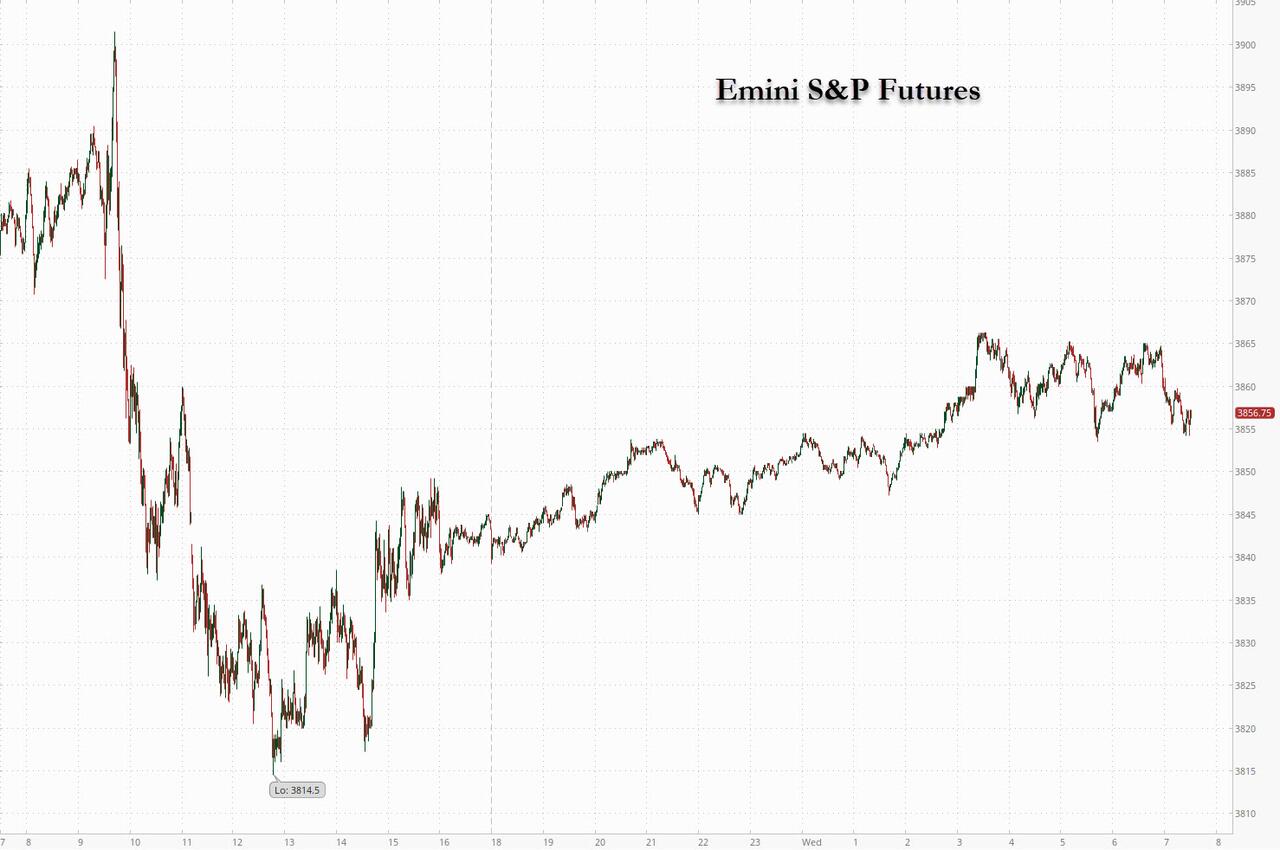

SPX futures made a 61% retracement at 3844.40 in the overnight session and may already be declining again, suggesting the cash retracement may be lower. The Cycles Model suggests the decline may continue through the end of January. The weakness of the retracement to the 50-day may be telling us that the intensity of the decline may increase by the end of the week. A decline in January does not bode well for 2023, as the “January effect” is a known phenomenon that recurs on a Cyclical basis.

ZeroHedge reports, “US futures reversed after Tuesday’s slump and gained on Wednesday, although easing off higher levels reached earlier, amid optimism around a boost from a potential recovery in China’s economy (which however was clearly not enough to find a bid below oil which crumbled for a second day), while investors awaited minutes of the Federal Reserve’s latest policy meeting for clues on the path of monetary policy. Nasdaq 100 futures rose 0.5% by 7:30 a.m. ET, while S&P 500 futures rose 0.3% after gaining 0.5% earlier following a burst of European optimism which sent the Estoxx50 2% higher, aided by European inflation data lifting risk appetite. The risk-on mood was also boosted after Chinese authorities said they are planning to usher in further support measures to ease liquidity stress at some of the nation’s too-big-to-fail developers as the property downturn persists. The dollar fell, erasing all of yesterday’s sharp gains, while Treasuries continued their “peak inflation is behind us and the Fed will soon stop tightening” ascent and added to Tuesday’s gains with yields richer by at least 6bp following wider rally across core European rates after French CPI unexpectedly slowed in December.

ZeroHedge relates, “According to Macrotrends.net, the S&P 500 has only seen consecutive years of negative returns three times since 1957, in 1973/1974 and in 2001/2002/2003 with returns getting worse in the second (and third) down year on each of those occasions. Since 1957, the S&P 500 has ended the year in the red 18 times including 2022. On 14 occasions, the index returned to growth the next year.”

VIX futures opened beneath the 50-day Moving Average at 23.24. Piercing the 50-day puts the VIX on a buy signal. While there may only be two weeks left in the current Master Cycle, the Model suggests Trending Strength may be returning this week. The upper Triangle trendline may be its initial target.

TNX futures are testing the trendline at 36.50 this morning. It turns out that the trendline seen in this chart may be an intermediate degree, while the longer-term trendline may be located near the Cycle Bottom near 23.95.

BKX, our liquidity proxy, lingers above the neckline of its Head & Shoulders formation at 97.00. Yesterday it reversed from its 50-day Moving Average at 102.90 on day 260 of its Master Cycle. A full reversal may be imminent.

ZeroHedge notes, “Money supply growth fell again in November, and this time it turned negative for the first time in 33 years. November’s drop continues a steep downward trend from the unprecedented highs experienced during much of the past two years. During the thirteen months between April 2020 and April 2021, money supply growth in the United States often climbed above 35 percent year over year, well above even the “high” levels experienced from 2009 to 2013.”