8:10 am

Good Morning!

Hope springs eternal as the NDX futures rallied to a new retracement high at 12552.90 this morning. Yesterday was “relatively” calm as the Cycles Model suggested. Today, on the other hand, is likely to be a bloodbath, despite the short squeeze lifting stocks higher in the pre-market. The problem is, most analysts have no idea what’s next. “What are we reading today, tea leaves, or chicken entrails?”

SPX futures reached an overnight “squeeze high” at 4055.20, within yesterday’s trading range. The Cycles Model calls for a day of trending strength, so the squeeze may turn into a rout by the end of the day. In today’s expiring options, Max Pain is at 4045.00 while short gamma starts at 4000.00 where the slippery slope ends and the drop off begins. It is little wonder the dealers and hedge funds are attempting to keep SPX in the neutral zone.

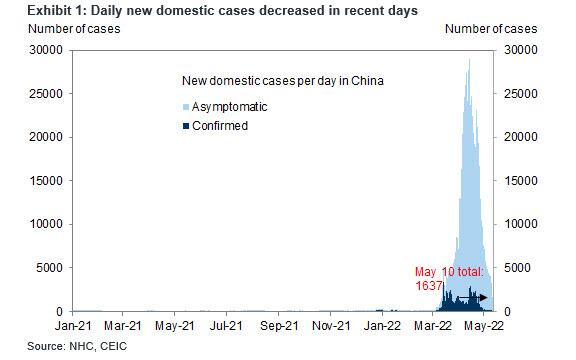

ZeroHedge reports, “US index futures and European stocks were set to extend their recovery from the longest streak of weekly declines since 2011 ahead of an inflation report that was expected to show prices cooled in April, while falling bond yields supported battered tech stocks; Asian equities also advanced, halting a seven-day slide, as new Covid cases tumbled in Shanghai with the local government saying there was basically no COVID community spread in 8 of 16 districts, and the Chinese covid scare appears set to fade.

S&P 500 futures were trading at session highs, up 1.2%, and Nasdaq 100 futures were up 1.4%, while Europe’s Stoxx 600 climbed for a second day. The dollar fell and Treasury yields slumped, with the 10Y trading a 2.91%, a 30 basis points slide in the past three days, providing further support for high duration tech names. US-listed Chinese stocks rallied in New York premarket trading after the Asian nation reported easing Covid cases. Tech stocks also climbed in Hong Kong and Europe on Wednesday.”

The NYSE Hi-Lo Index had its second worst day in two years. The calm surface at yesterday’s close is a lie. Investors are bailing, although this is not capitulation, yet. The sense of defeat at the bottom may be so great that no one will be looking up.

VIX futures are spiking higher, recently hitting 34.25 and climbing. As SPX declined beneath 4000.00, the pressure to hedge will grow exponentially. The ratio of puts to calls is 10 to 1 beneath 4000.00, suggesting VIX may rise to 90.00 or higher this summer.

TNX is on a bounce this morning that may turn into a rout later in the day. An alternate explanation may allow a continued rally in TNX through the end of May. Details may be forthcoming.

ZeroHedge reports, “fter March’s surge in consumer prices, analysts’ consensus is that CPI has peaked and April was expected to show a big slowing from +8.5% YoY to +8.1% YoY, however, CPI printed hotter than expected at +8.3% YoY…

Source: Bloomberg

Bear in mind that headline CPI is still at its second highest since 1982.’

USD futures rose to 104.14 this morning, short of Monday’s high. There is still room to go higher. A sell-off in stocks may increase the demand for dollars as investors choose cash. The common wisdom is the dollar should decline with a higher CPI print.

ZeroHedge comments, “Watch out for a non-textbook surprise in the dollar just after U.S. inflation data hits. In the past 12 months, CPI has mostly come in hot — yet the BBDXY has fallen more often than not. That probably runs counter to the belief that the U.S. currency should rise on a high reading as it steers the Fed toward faster rate hikes.

The one time CPI surprised on the downside in January, the dollar fell 0.2% in the first thirty minutes after the data. Here’s a breakdown of the numbers:”

Crude oil bounced this morning, testing the 50-day Moving Average at 104.56. An alternate retracement target may be the Broadening Wedge trendline near 106.00. However, the short-term trend may be down with the next low near the June options expiration.

ZeroHedge explains, “Global stocks of refined petroleum products have fallen to critically low levels as refineries prove unable to keep up with surging demand especially for the diesel-like fuels used in manufacturing and freight transportation. The result has been a surge in prices refiners receive for selling fuels compared with prices they pay for buying crude and other feedstocks, boosting their profitability significantly.

In the United States, refiners currently receive roughly an average of more than $150 per barrel from the sale of gasoline and diesel at wholesale prices, while paying only around $100 to purchase crude.

The indicative 3-2-1 margin of $50 per barrel is based on the assumption a refinery produces two barrels of gasoline and one barrel of diesel from refining three barrels of crude.”