8:50 am

The GSCI Ag Index broke out above its previous high at 427.51 yesterday, indicating the rally is in full swing. The Cycles Model suggests it may continue to the week of August 23. The next resistance is at the Wave [1] high at 474.12 with additional resistance at the Cycle Top at 478.04. Shortage-driven inflation reigns in the Ag sector.

ZeroHedge reports, “The U.S. Department of Agriculture’s World Agricultural Supply and Demand Estimates (WASDE) report was released Thursday afternoon and pointed to declining grain supplies that sent grain futures prices higher and will keep food inflation in focus.

The closely watched supply and demand report slashed estimates for corn yields and stockpiles. World inventories for wheat were reported near a five-year low.

Grain and oilseed futures soared to a near-decade high earlier this year but have been in a holding pattern for the last month, awaiting new reports on the outlook for upcoming U.S. harvests. A megadrought and back-to-back heat waves have plagued the corn belt and the U.S. West for much of the summer.

December corn futures were up more than 2% to $5.7150 a bushel on the Chicago Board of Trade, soybean futures popped on the report and are now flat at the end of the U.S. cash session, wheat futures rose more than 3%, hitting a fresh eight-year high.”

7:40 am

Good Morning!

SPX futures rose to a new all-time high 4465.30, then eased back to the flat line. The open interest in calls is a net 3600 at 4450.00, a net 3758 at 4460.00 and a net 2400 at 4465.00. MAX PAIN is at the trendline near 4440.00, beneath which the puts rule. The objective for options expiration is to close at MAX PAIN.

ZeroHedge reports, “S&P 500 futures celebrated Friday the 13th with a brand new record highs on Friday boosted by Walt Disney’s forecast-beating results, while signs of cooling inflation and a strong recovery in corporate earnings kept the indexes on track for a second straight week of gains. But the real party today was in Europe, where stocks headed for the 10th consecutive record high, the longest winning streak since 1999, as bullishness swept across markets after a blowout earnings season and economic recovery out of lockdowns. Asian markets, Treasury yields and the dollar dipped while cryptos surged with both bitcoin and ethereum up around 5%. At 730 a.m. ET, Dow e-minis were up 46 points, or 0.13%, S&P 500 e-minis were up 1.5 points, or 0.06%, and Nasdaq 100 e-minis were down 3 points, or 0.01%.”

VIX futures remained flat during the overnight session with a low of 15.53. It is currently positive but not near the 50-day Moving Average at 17.25. The Master Cycle appears to be complete at day 258.

ZeroHedge comments, “We live in fascinating times. Today, we have a unique opportunity to observe one of the biggest speculative bubbles ever, and to understand how financial markets evolve towards critical points.

While Western central banks have lost control in March 2020, flooding the system with absurd amounts of liquidity, a scary number of participants are now convinced that monetary illusion will make them rich.

Unfortunately, historical analysis of capital markets shows us that the exact opposite is likely to happen. But no one really cares about empirical evidence. People are even becoming more aggressive – especially on social media –, whenever someone tries to warn of an incoming tail risk event.

The question is, why? If people are so comfortable with their “stock only go up” scenario, then why worry?”

NDX futures topped out at 15096.50, then resumed their decline. Short-term support lies at 15029.10, beneath which lies a confirmed sell signal. The NDX Hi-Lo Index closed at -23.00 yesterday, giving condirmation of the decline while the VXN/VIX both hover beneath their respective 50-day Moving Averages. Breaking support is likely to punch volatility over resistance.

ZeroHedge cautions, “Back in early February of 2020, I noted that, even as the major stock market indexes had pushed to new highs, a number of Hindenburg Omens had been triggering on the NYSE and the Nasdaq pointing to a significant deterioration in breadth:

“While an individual signal has very little value in forecasting a stock market crash… a cluster of signals can be valuable in that it signals a pattern of dispersion that is not compatible with a healthy uptrend.”

The Shanghai Composite fell through Intermediate-term suport at 3513.20 to 3500.50 before bouncing. This is confirmation of the sell signal and may offer a heads-up to developments in the NDX in the coming weeks. SSEC also put in a Master Cycle high on Wednesday, indicating a potentio decline that may last through mid-October.

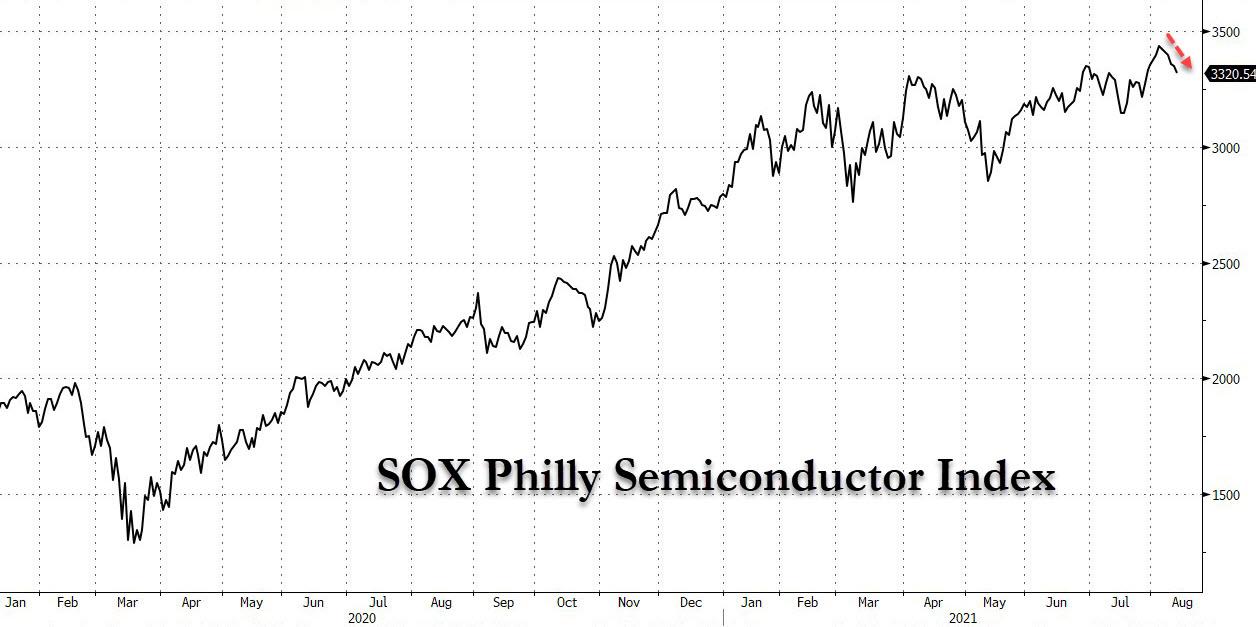

ZeroHedge observes, “The semiconductor space has long been viewed as one of the best leading indicators of the modern technological economy (and capital markets), and with good reason: it was the first sector to bottom in March 2020 when it became apparent that China and various western central banks would inject trillions into the global economy, and had enjoyed a nearly relentless upward climb since then peaking just over a week ago on August 4, but then something snapped…

… and as shown in the next chart, the Semi Index is broadly lower again, having dropped for six consecutive sessions – the longest such streak since the October 2018 Fed “policy error” when stocks cracked after Powell threatened to tighten far more than markets expected, only to end his hiking cycle prematurely just two months later, resulting in the first bear market in a decade.”

USD futures have pulled back this morningand may test support at 92.50. It may regain its strength next week as it resumes its rally.

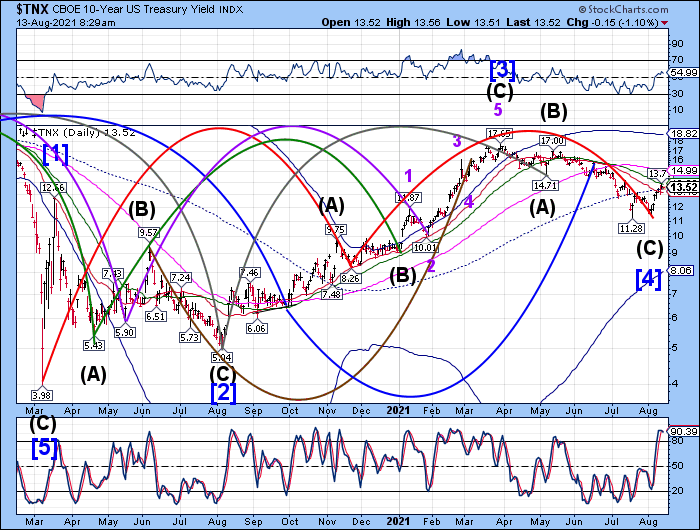

TNX pulled back from the 50-day Moving Average at 13.82. It did not find support at mid-Cycle support at 13.44, so the decline may continue no lower than Intermediate-term support at 13.13. Any pullback may be used as an accumulation phase for the next surge higher in about two weeks.

ZeroHedge reports, “After yesterday’s blockbuster, record-setting 10Y auction which saw many buyside metrics print at the strongest levels on record (nearly 4bps stop through, record high indirects), traders expected today’s last refunding auction – when the Treasury sells $27BN in 30Y paper – to be a more muted affair. According to Bloomberg, investors should go for the $27 billion bonds auction with yields above the round threshold of 2% and there is likely to be a smattering of short covering at the 1 p.m. NYT deadline with 30Y paper trading special in repo.

“The 30-year auction will not have a bid from central banks, in our view,” wrote Padhraic Garvey, head of global debt and rates strategy at ING Groep NV, noting that yields on the long bond are about 2% and broadly in the same area as last month’s sale. “It’s in a similar boat this time around.”