7:30 pm

TNX may have made its Master Cycle low today at day 255 in the Cycle. The Elliott Wave structure also appears complete. While there may be a small probability of a further low on Monday, the highest probability points to a strong, complacency busting reversal. As mentioned previously, the target for this rally may be 19.71, which would more than compensate for the 3.5 point (current) negative divergence between the CPI and TNX.

ZeroHedge comments, “Even though US CPI smashed expectations again, Deustche Bank’s chief credit strategist Jim Reid correctly points out that “the data isn’t going to change anyone’s mind of whether inflation is transitory or not.”

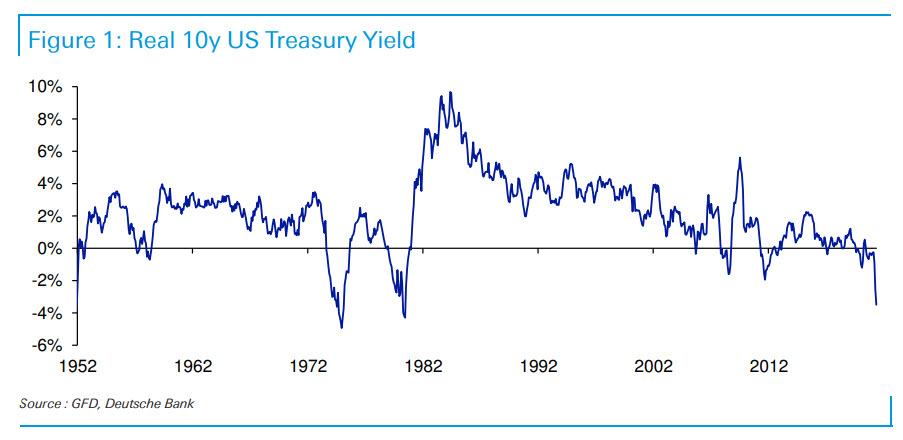

Still, as an aside for those who still care about fundamentals, he notes that the current gap between 10yr US yields (c.1.5%) and US CPI (5.0%) is a whopping 3.5%, the highest since 1980. In fact, the gap has only been more negative for 10 months in the last 70 years, all of which were in 1974, 1975 or 1980.

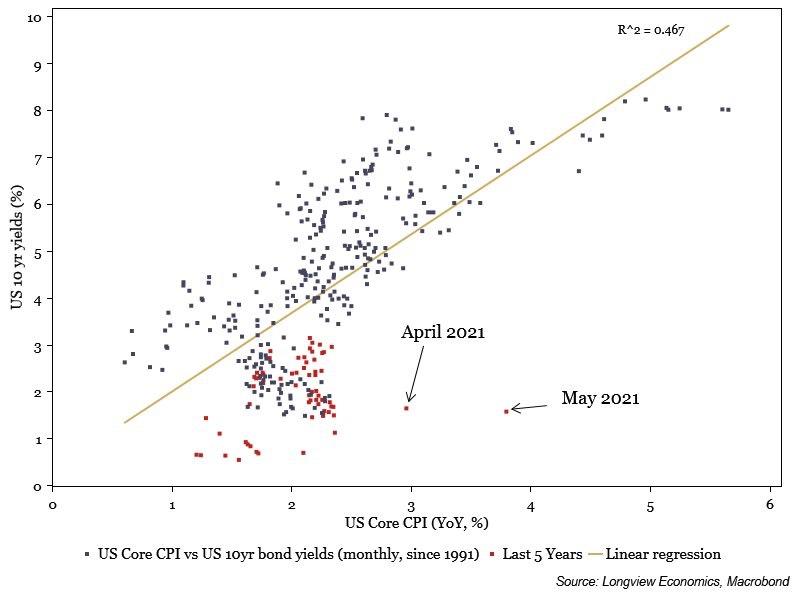

Another way of visualizing the unprecedented divergence between core inflation and 10Y yields is the following scattergram from Longview economics:”

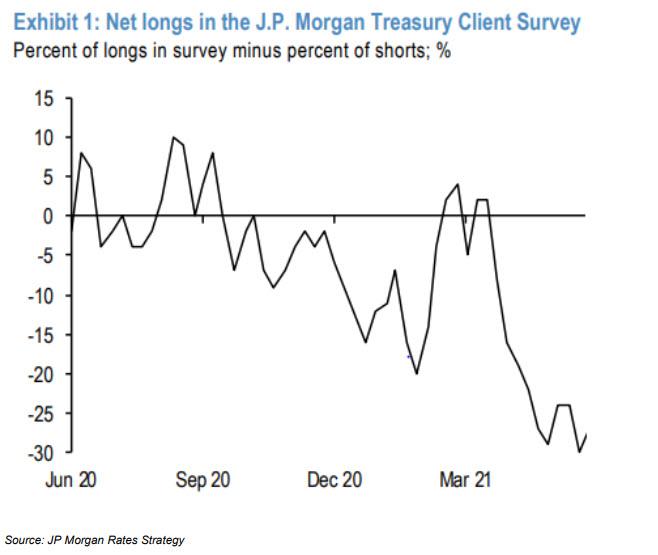

ZeroHedge further comments, “One day before the “most important CPI print in history”, we showed the latest JPM Treasury Client survey and pointed out that “there were virtually no traders left to short Treasurys, with all bears already on board” as net short interest had hit an all time high. As a result, even a red hot CPI had been fully priced in by now, and the result would be sharply lower yields as we got another massive short squeeze, this time in rates.

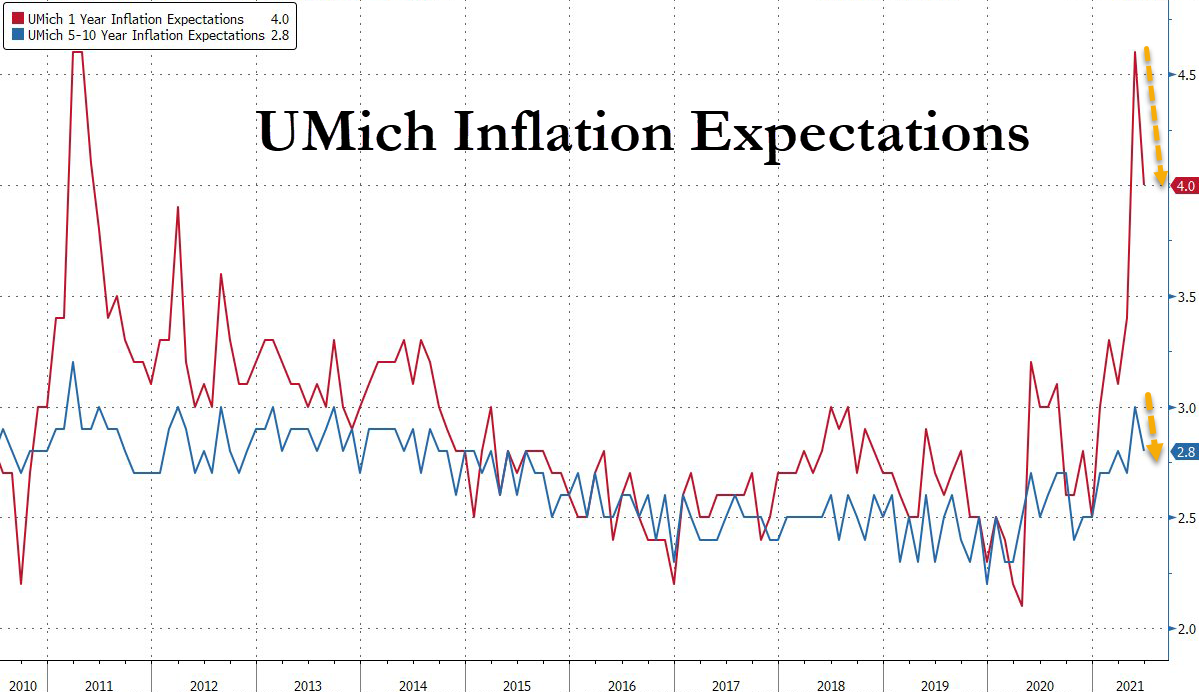

Well, with 10Y yields tumbling to March lows and breakevens in freefall over the past 48 hours, that’s precisely what happened, and since not even yesterday’s scorching inflation print managed to spark some bearish rate sentiment, the market was promptly overrun with speculation that the reflation trade is now largely finished as “inflation has peaked”, an argument which was further bolstered by today’s drop in UMich 1Yr and 5-10Yr inflation expectations.

Commenting on this shift in market sentiment, Nomura’s Charlie McElligott writes that the liquidation of “Reflation” and “Hawkish Fed” trades clearly accelerated into crescendo yesterday, “as despite another really strong US Core CPI print yesterday, the “transitory” nature of a large part of the gains (“Used Vehicles” being 1/3 of the seasonally-adjusted increase, and as a function of supply-chain and semiconductor shortage issues), as well as still-stagnant Wages (AHE YoY cratering with MoM utterly sideways) and most critically, an incredibly disappointing Labor market, all lends further credibility to the Fed’s “slow-play” stance and forces a positioning-cleanse of insanely crowded “Short UST” positioning—which critically, hasn’t been returning for months now.”

7:30 am

Good Morning!

I have an appointment soon, so I will do what I can this morning.

NDX futures have risen to 13997.62 at this point. Since today is a potential day of strength, I wouldn’t be surprised to see it make a new all-time high. Note that this Cycle took 258 days from low-to-high.

SPX futures have come very close to another new all-time high this morning. Today’s Cyclical strength may propel it to that new high, as well.

ZeroHedge reports, “S&P futures – which overnight rolled from the ESM (June) to the ESU (Sept) contract – extended gains on Friday further into record territory as inflation fears receded into the background calming concerns over a possible long-term spike in rising prices, with investors now turning focus to next week’s Federal Reserve meeting for more cues on monetary policy. Treasuries were steady, trading at 1.44% – just above the lowest level since March – amid growing (if wrong, according to BofA and DB) confidence inflation will prove transitory, leaving scope for continued central-bank support. S&P 500 E-minis were up 7.25 points, or 0.17 at 06:36 a.m. ET. Dow E-minis were up 77 points, or 0.22%, while Nasdaq 100 E-minis were up 30.25 points, or 0.22%.

After seeing fresh all-time highs on Thursday, US equity futures have largely been traversing sideways, in wake of Thursday’s dovish ECB confab, and surging US inflation, which has not given too much concern to equity or bond investors ahead of next week’s FOMC, since the Fed is likely to look through what it sees as ‘transitory’ price pressures; some analysts disagree, arguing that there is building evidence of more sticky prices, but whether or not this inflation proves to be transitory will only really be resolved in Q3/Q4, so for now, markets are taking the Fed at its word. BofA reported that US equities have seen the first weekly outflows since March, with more outflows out of growth styles than value styles; by sector, inflows were seen in financials, materials, real estate, energy and health care, while outflows were seen in utilities, communications, consumer sectors, and tech.”

VIX futures record another ow of 15.15 this morning, still within the parameters of a retracement rather than a new low.