8:00 am

Good Morning!

NDX futures climbed to a morning high of 13627.00, above the mid-Cycle resistance at 13533.94, an approximate 34% retracement. The futures page contains some inaccuracies that lead me to take that information with a grain of salt. There is likely to be another push lower that may complete an impulsive (5-Wave) decline.

The NDX Hi-Lo closed at 26.00, not far from where it began yesterday. Remember, due to the presence of the mega-tech stocks, there only needs to be a handful trading positively to keep the NDX elevated. A confirmed sell signal won’t be registered until it falls beneath zero.

SPX futures may have hit a high at 4185.12, but have eased back down to Short-term support/resistance at 4173.92. Again, the market feed is giving troublesome information. Nevertheless, the Short-term line also denotes the 50% retracement level of the decline thus far. Should the SPX resume its decline, it may proceed to mid-Cycle support at a minimum, at 4083.13. The NDX decline may exert a greater downward pull on the blue chips, extending this decline even further.

ZeroHedge reports, “US index futures rebounded from Tuesday’s tech-led rout, with Nasdaq futures leading gains alongside shares in Europe as focus shifted away from inflation fears and turned to strong earnings and the global economic recovery. Nasdaq futs gained the most, rising 70.25pts or 0.52% to 13,606, S&P futures were up 14.25 points or 0.34%, and Dow futures were back over 34,000, up 57pts or 0.17% to 34,077. Oil and the dollar also climbed.”

VIX futures hovered between the trendline and the 50-day Moving Average in the overnight session. Again, the data-feed appears problematic, so we should know more at the open.

TNX rose back above the 50-day Moving average at 15.94 which it tested yesterday. The Cycles Model indicates that strength may come back to this uptrend in the next week.

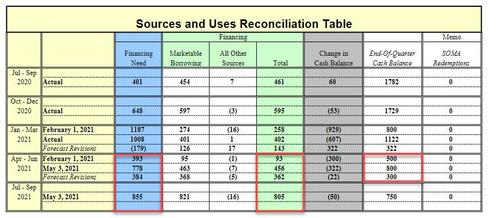

ZeroHedge observes, “Two days after the US Treasury surprised rates watchers by unveiling that it would sell nearly 5x more Treasuries in the current quarter than previously expected ($465BN vs $95BN) and $1.3TN over the second half of the fiscal year, while reducing the amount of cash released from the TGA…

… at 830am on Wednesday in its latest quarterly Refunding Announcement, the Treasury announced that it would keep its quarterly auction of long-term coupon debt unchanged, and at an all time high, of $126 billion (vs $84 billion a year ago) to refund approximately $47.7 billion of Treasury notes and bonds maturing on May 15, 2021. This issuance will raise new cash of approximately $78.3 billion. ”

USD futures appear to be stalled beneath the 50-day Moving Average at 91.60. The Cycles Model suggests strength rising into options expiration week.

ZeroHedge observes, “A little over a week ago, we reported on one of the biggest deflationary threats looming over the global economy: that is, China’s shrinking population, as deaths outpace births for the first time, a trend that demographers believe will only worsen as the impact of China’s one-child policy is felt on its population numbers.

And as Wall Street banks and America’s largest corporations complain about growing inflationary pressures in their sell-side research and earnings calls, the latest population update from the CDC has just confirmed that the deflationary trend of a falling birth rate continued last year in the US. In fact, one could argue this trend has been supercharged by the pandemic, thwarting theories about a lockdown “baby boom” as the number of births in the US fell by 4% in 2020, dropping to the lowest level since 1979.”

Put another way: thanks to the pandemic, US birth rates have fallen to their lowest level in a generation.