9:30 am

BKX just plunged beneath the 50-day Moving Average at 79.15 and Intermediate-term support at 78.25 to confirm a sell signal. Something may emerge in the Banking Sector that constricts liquidity. The Head & Shoulder target is still valid.

9:20 am

Prepare for a gap down beneath 4350.00 in the SPX and an aggressive sell signal.

7:40 am

Good Morning!

PLEASE NOTE: i will be out of town until Thursday. Commentary may resume on Friday.

NDX futures are down this morning after making a 51% retracement. The Cycle dynamics have changed, with 3 days down and only one day of retracement. This compares to last year’s 2 to 1 ratio. Keep that in mind as we launch a vicious decline that may last up to 4 weeks. Short covering may be brutal, but the decline may be much worse.

In today’s op-ex, 14950.00 is hotly contested. Long gamma may begin at 15000.00 while short gamma gains ascendancy beneath 14900.00.

SPX futures are testing Cycle Top support at 4356.00 this morning after a less-than-Fibonacci retracement of 32%. There is an outside chance of a quick recovery to make a higher retracement, but once beneath 4350.00 the decline resumes under an aggressive sell signal. The sell signal is confirmed beneath Intermediate-term support, currently at 4229.74

Today’s op-ex shows the strike at 4375 may be hotly contested Max Pain. Long gamma begins at 4400.00 while short gamma takes over at 4350.00.

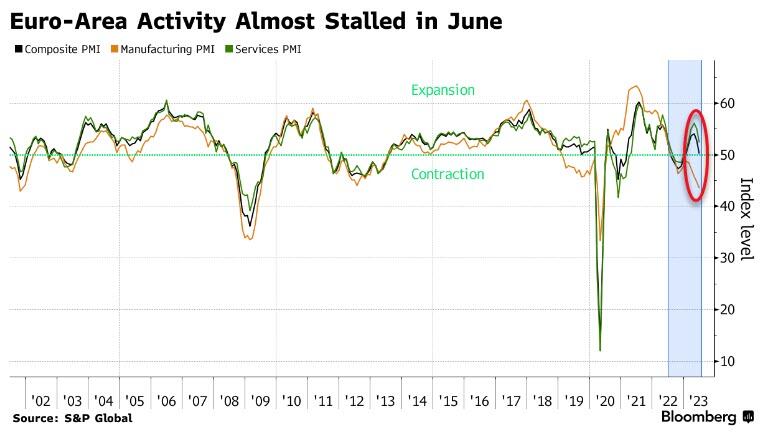

ZeroHedge reports, “One week after S&P futures hit a 52-week high, sentiment has turned increasingly ugly and US equities are set to open lower for the 4th of the past 5 days, with global stocks also sliding, after the latest set of dismal European PMIs revealed that economic momentum in the euro area almost came to a halt in June, signaling an end to the revival the bloc demonstrated since its winter downturn (and good news for the ECB which has been desperate to spark a recession). As of 7:45am ET, emini S&P futures were down 0.5%, trading just over 4,400, almost 100 points below the YTD highs hit last Friday; Nasdaq futures were also down half a percent, as investors fled into the safety of bonds amid a return of fears that weak euro-area activity data together with aggressive central bank rate hikes will tip economies into recession. The Bloomberg dollar index traded near the day’s highs, pressuring all Group-of-10 currencies. Treasury yields fell across the board, following pullbacks in the UK and Europe. Gold advanced, Brent crude slid more than 1.5% and Bitcoin fell for the first time in five days. Today’s macro data focus is PMIs releases: the street expects another contractionary print from the US Mfg PMI at 48.5, while services are expected to dip to at 54.0 from 54.9.”

VIX futures rose to 13.55 this morning after a likely bottom made yesterday on day 267. While an 8.6-day extension is allowed in the Master Cycle, there is no explanation where the selling originates. Was the VIX decline meant to curb the decline in stocks in a tail-wags-the-dog fashion?

A look at the VIX op-ex next Wednesday shows Max Pain at 13.50. There is no short gamma, while long gamma takes of at 16.00.

TNX was beaten back to the mid-cycle support and trendline at 36.80 this morning. It remains in a consolidation as it gathers strength for the next probe higher. The target for the next two weeks appears to be the Cycle Top resistance at 41.22.

USD futures rose to an overnight high of 102.78, probing above the 50-day Moving Average at 102.26 and issuing a buy signal. This action may launch a 2-month rally in the USD. Analysts who are trash talking the USD fail to see the worsening conditions elsewhere, especially in Europe.

ZeroHedge reports, “Hope for a rebound from Europe’s economic ‘winter’ were dashed this morning as PMIs signaled a renewed downturn.

S&P Global EU PMI fell to a 5-month low of 50.3 (barely in expansion). The decrease in the composite index was broad-based across sectors but skewed towards services, although the services index, unlike the manufacturing output index, remains in expansionary territory.

The composition of the June report showed a broad-based moderation across new orders, employment, new export orders, and backlogs. Firms’ future output expectations declined further as well.”