The Lord’s Prayer

Our Father, who art in heaven, hallowed be thy name. Thy Kingdom come, Thy Will be done, on earth as it is in heaven. Give us this day our daily bread and forgive us our trespasses, as we forgive those who trespass against us. And lead us not into temptation, but deliver us from evil. Amen.

8:30 am

Good Morning!

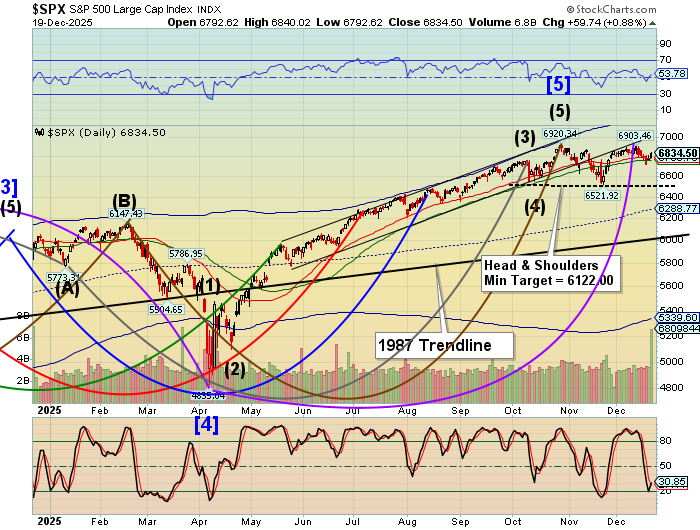

SPX futures rose to 6863.30 thus far this morning, just short of the 6865.00 resistance level mentioned on Friday. The Cycles Model indicates that the SPX is at an important pivot point, suggesting a possible reversal may be at hand. The consensus is that the markets are riding a wave of liquidity into the end of the year. The Cycles Model indicates otherwise. Massive selling lies ahead to fund the in-the-money calls (T+1) that expired on Friday.

Today’s options chain shows Max Pain at 6835.00. Long gamma may begin above 6850.00 while short gamma lurks beneath 6800.00.

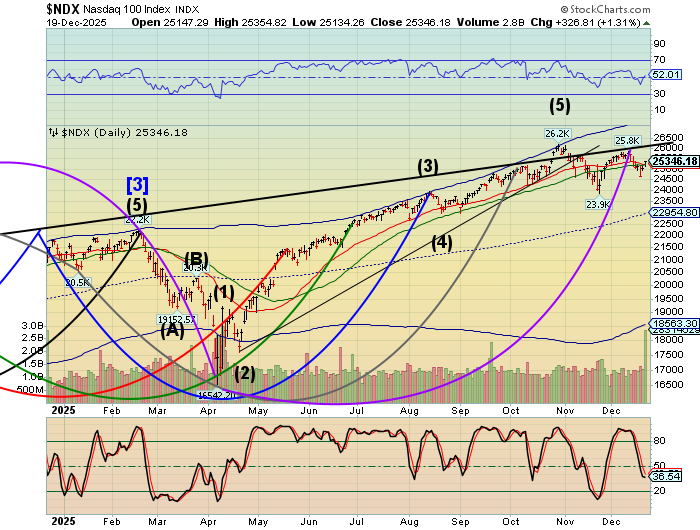

ZeroHedge reports, “As we previewed late last week, the Santa Rally is back all right, and US equity futures are trading near session highs with the Nasdaq 100 poised to wipe out December’s losses as revived appetite for technology stocks powered gains across equity markets.”

NDX futures rose to 25505.80 thus far this morning, momentum being propelled by fumes from Friday’s positive options expiration. However, the December 10 high at 25835.00 has not been breached. Today may be a day of strength for the NDX, but also a day for a reversal.

ZeroHedge observes, “Nvidia shares rose slightly in premarket trading in New York after Reuters reported that the US chipmaker has informed customers it plans to ship its second-most powerful AI chip, the H200, to China before the Lunar New Year in mid-February.”

VIX futures ;declined to 14.81 this morning, extending its Master Cycle low. The Cycles Model cites today as a potential reversal day as the VIX may find “the floor.”

The December 24 options chain shows short gamma under 15.00 while long gamma prevails above 16.00 and has a presence to 35.00.

TNX has risen to a high at 41.69 this morning, under the critical 42.00 level. The Cycles Model shows TNX in a sideways consolidation to the end of the year, then rising, with strength, to mid-January.

ZeroHedge notes, “For those traders who are still “out there” instead of the slopes of Chamonix mingling with freshly embezzled US tax dollars by way of Kiev, DB’s Jim Reid reminds that we’re now entering a very quiet spell for markets before Christmas, with data releases and other headline announcements almost completely drying up.”

Bitcoin may be reversing out of a 61.8% Fibonacci retracement of last week’s decline. The

Cycles Model indicates that Bitcoin is very near its end, if not already on December 19. It may take another day or two to resolve the pivot point. With the resolution may come some high volatility.

Silver futures have risen to 69.51 over the weekend, then eased down from there, testing the upper trendline. The Master Cycle is stretched about a week beyond its median length of time. It is time to be very careful with silver. It may be due for a correction that may potentially decline to the mid-Cycle support at 41.67. One concern of particular note: The EU is preparing for war. As a means of preserving their capital from fleeing, the EU may install capital controls to stymie capital flight. European countries have been historically noted to abscond with privately held precious metals. This may affect the price of precious metals in the US.

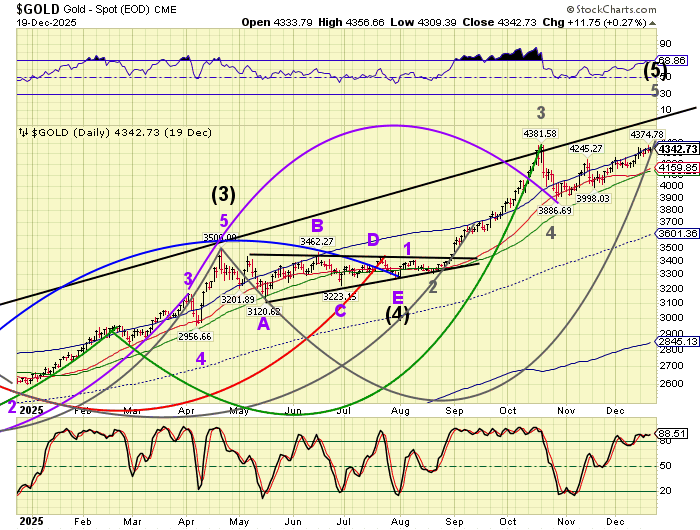

Gold futures rose to 4474.00 and still climbing in a stretched Master Cycle. Resistance is at 4500.00. Gold may be just a day or two from its top, an all-time high. A correction down to mid-Cycle support at 3601.00 may be imminent.

The Yen is bouncing off support from its November low. However, it has about two more weeks in the Current Master Cycle. A deeper low is anticipated by the Cycles Model The minimum target may be near 63.20, but given time, may decline to 62.30. The Yen carry trade has been given a reprieve, if only for the next two weeks. Meanwhile, the Bank of Japan may be worried that the Yen may have lost support, even after raising interest rates to .75% from .5%. On September 19, 2025 (red line), the Bank of Japan announced the beginning of selling shares in the Japanese stock and real estate market to steady the Yen. Instead of shoring up the yen, it caused another sell-off. The current sell-off may destabilize the Japanese markets, thereby increasing the fragility of the US markets.