10:25 am

BKX, our liquidity proxy, has been repelled from the 200-day Moving Average, currently at 83.11, twice thus far. It may be considered on an aggressive sell signal with confirmation at the mid-Cycle support/resistance line at 80.90. The Fed has been doing a fine job of postponing the inevitable, but it can only last so lang. Branch closures often precede bank closures. See the articles below.

ZeroHedge observes,The financial crisis that kicked off in March continues to bubble under the surface…

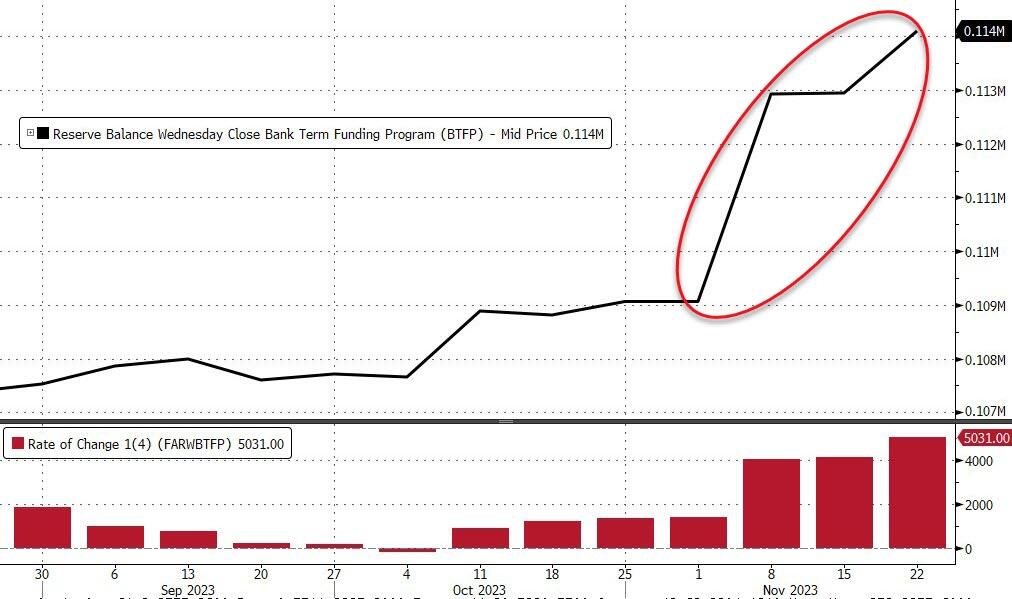

Total outstanding loans in the Federal Reserve’s bank bailout program jumped by just over $5 billion in November.

There was a sudden spike in banks tapping into the bailout program during the first week of the month with financial institutions borrowing $3.87 billion from the Bank Term Funding Program (BTFP). There was another surge in borrowing between Nov. 15 and Nov. 22, according to Fed data.

As of Nov. 22, there was $114.1 billion in outstanding loans in the BTFP bank bailout program.

ZeroHedge also observes, “Big banks such as PNC Bank and JPMorgan Chase have filed to close several branch offices in multiple states amid a troubling pattern of rising branch shutdowns in recent years.

Between Nov. 12 and 18, several banks filed to close branch locations, with PNC Bank with the most filings, according to data from the U.S. Office of the Comptroller of the Currency. Pittsburgh-based PNC Bank filed for 19 branch closures—five in Pennsylvania, four in Illinois, three in Texas, two each in Alabama and New Jersey, and one each in Indiana, Ohio, and Florida.

JPMorgan Chase followed closely with 18 filings—three in Ohio, two each in Connecticut and South Carolina, and one each in 11 states, including New York, Illinois, Florida, and Massachusetts.”

8:10 am

Good Morning!

Please note: I am going in for eye surgery tomorrow and may not be able to see well enough to write this blog for at least a few days. Please be patient. I will return as soon as possible.

NDX has made its high on Wednesday, day 254 of the Master Cycle which averages 258 days in length. Today is day 259, suggesting time is running out for this Cycle. This morning NDX futures declined to 15896.80 before a bounce. Overhead resistance is at 16200.00, then 16590.00. The 2021 all-time high is 16764.86. The Cycles Model suggests that NDX neither has the time nor the energy to make a new all-time high. An aggressive short may be made beneath 15738.00.

Today’s options chain shows Maximum investor pain at 16000.00. Long gamma may begin at 16050.00, while short gamma may begin at 15950.00.

ZeroHedge remarks, “There was a notable divergence below the market’s otherwise silky smooth surface last week.

While the broader market rally accelerated for the 4th consecutive week from the October lows, sending various indexes anywhere between 9% and 13 % higher in the past 4 weeks…

… and the S&P just shy of 2023 highs and less than 5% from its Jan 2022 all time highs, even though interestingly enough, tech actually underperformed last week as we pointed out in our week wrap.”

SPX futures made a low at 4542.20 this morning before a bounce bringing it back to neutral. Todays is day 259 of the Master Cycle which may be complete or nearly so. Overhead resistance is at 4600.00. An aggressive sell signal lies at 4500.00.

Today’s options chain shows Max Pain at 4550.00. Long gamma begins at 4560.00 while short gamma starts at 4535.00.

ZeroHedge reports, “US equity futures and global markets are in the red, amid a broader risk-off tone to start the week as a renewed slowdown in China’s industrial profits growth dented sentiment in global financial markets, as they were seen as a sign of weak domestic demand and a reminder of the country’s economic slowdown. As of 7:35am, S&P and Nasdaq futures were both down 0.1%, off the worst levels of the session. 10-year TSY yields climbed as much as five basis points to 4.51%, the highest in more than a week, before reversing the entire move; gold climbed to the highest since May, rising over $2,100 while the dollar was little changed and bitcoin slumped under $37,000. Oil was down a fourth day before this week’s delayed OPEC+ meeting. Retail Sales numbers for Black Friday showing +2.5% YoY gain with online sales +7.5% to a record $9.8bn; this could be driven by discount/bargain hunting. Today we will get the October new home sales data, with economists expecting a decline after September’s surprise surge in sales volumes as higher mortgage rates and increased inventories of existing homes weigh on sales. The Dallas Fed manufacturing activity index is also due later for November.”

VIX futures are hovering near Friday’s low, which May have concluded the current Master Cycle. Should the new Master Cycle begin, it may last until mid-January. Historical comparisons are misleading and dangerous to your wealth.

Wednesday’s options chain shows Max Pain at 14.50. Short gamma reigns between 12.50 and 14.00. Long gamma begins at 15.00 and extends to 27.00.

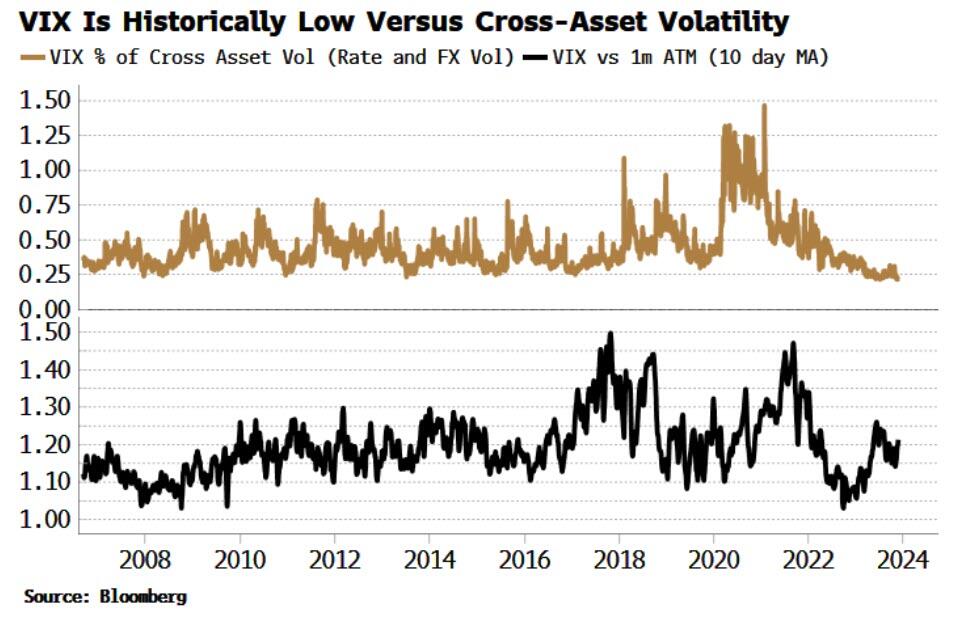

ZeroHedge remarks, “he VIX made its cycle lows last week, despite elevated cross-asset volatility and poor fundamentals in credit markets that would normally be consistent with a higher VIX.

The index made a new pandemic-era low last Friday, steepening the VIX futures curve.

The VXV (made up of options with an average expiry of three months) and the VIX1D (made of zero-day options) also both made new lows.

Moreover, the VIX is low versus realized volatility and, shown in the top panel of the chart below, historically low versus cross-asset volatility (i.e. fixed-income and FX volatility).”

TNX is retesting its trendline after rising above it on Friday. This may be the beginning of a new Master Cycle that may rise into the end of the year. Unfortunately, the prevalent discussion is when the Fed may start cutting rates, not a resumption of rising rates.