8:10 am

Good Morning!

NDX futures rose to 16011.00 this morning as the index continues to consolidate beneath Monday’s high at 16056.76. Yesterday’s action may have caused an island reversal, leaving a gap between Tuesday’s open at 15951.00 and Monday’s close at 16027.06. Should the gap be filled, the NDX may go higher. However, today is day 254 in the Master Cycle, so time is running out. In addition we have Thanksgiving holiday on Thursday and a half-day market on Friday. Today may tell us whether the rally is over or not.

Today’s options chain shows fierce competition between longs and shorts between 15925.00 and 15950.00. Long gamma starts at 16000.00 while short gamma begins at 15900.00.

ZeroHedge observes, “They are long up here

Non dealers US equity futures positioning is rather long again. We have seen slightly longer positioning, but the brutal move since the crowd was short has been extreme.”

SPX futures have climbed to 4553.10 thus far this morning. Dealers and institutions are attempting to re-ignite the rally going into Thanksgiving. Remember, institutions start the market day, then sit back and observe what retail investors do with their “signals.” The final outcome is the close, where all the activity is netted out. Today is day 254 in the Master Cycle. Time is starting to run out for the bulls. One may consider an aggressive short position beneath 4500.00.

Today’s options chain shows Max Pain at 4525.00. Long gamma starts at 4550.00 while short gamma rears its head at 4520.00 and becomes very persistent beneath 4500.00.

ZeroHedge reports, “Futures reversed earlier losses and traded at session highs as bond yields slid to two-month lows and oil tumbled after Bloomberg reported that the OPEC+ meeting scheduled for this weekend could be delayed amid Saudi dissatisfaction with member production levels. As of 7:40am ET, S&P futures rose 0.24%, trading at 4,562 and Nasdaq futures gained 0.4% as Wall Street headed for one of the best November rallies on record. Nvidia pared a decline in pre-market trading after investors initially reacted coolly to its latest quarterly report; the stock traded in a 6% range last night when its Q4 guidance was in the middle of the whisper range. Microsoft gained about 0.7% as Sam Altman returned to OpenAI after days of drama. The decision to restore him to the world’s best-known artificial intelligence startup marks a victory for biggest backer Microsoft, which worked with fellow investors to reverse Altman’s firing. Treasury yields dipped to two-month lows at 4.37%, while the USD rebounded from its weakest level in almost three months; commodities are under pressure ex-metals; gold remained just over $2000 as bitcoin recovered some of its overnight losses that dragged it below 35,000 following news of the Binance/CZ fine and settlement. News of a temporary halt in fighting between Israel and Hamas failed to ignite broader risk-on sentiment, with investors instead looking to data including mortgage apps, jobless claims, durable- and capital-goods orders and consumer sentiment, for clues on the direction of monetary policy. ”

VIX futures sank to a new low at 12.96 this morning. Today is also day 254 in the Master Cycle. Since VIX trades in smaller volumes, it can be easily manipulated. However, that does not extend beyond the end of the Cycle, which is upon us.

Today’s options chain shows Max Pain at 13.00-13.50. The shorts have an advantage at 13.50, but there is no follow-through. Long gamma starts at 16.00 and extends to 30.00.

ZeroHedge comments, “Record gamma. Record boring

1. GS has dealers long $7.1bn of SPX gamma at spot, the second highest reading since 2022.

2. The cash equity desk at GS says they were 2 on 1 –10 scale in terms of overall activity levels

3. Another slow day on the derivatives side as 28.96mm total options traded, the 3rd lowest volume YTD (42.63mm avg)”

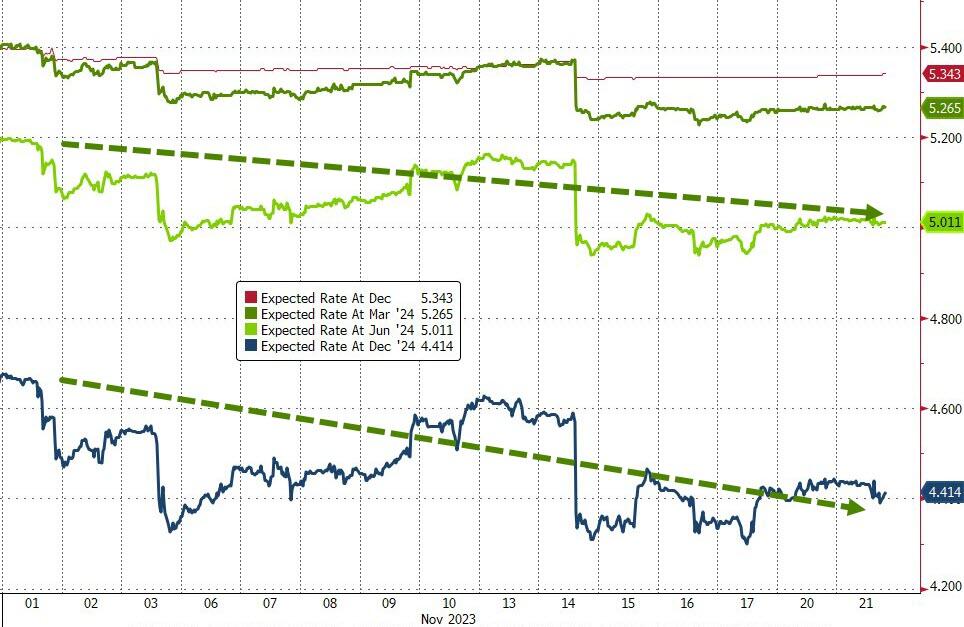

TNX sank to a new low at 43.65 this morning. However, it bounced immediately back to the trendline. Today is day 251 in the current Master Cycle. The Cycle normally may have a week to resolve. However, TNX is putting on the finishing touches to an ending diagonal, signaling the end to this decline. Those expecting rate cuts may be mightily surprised.

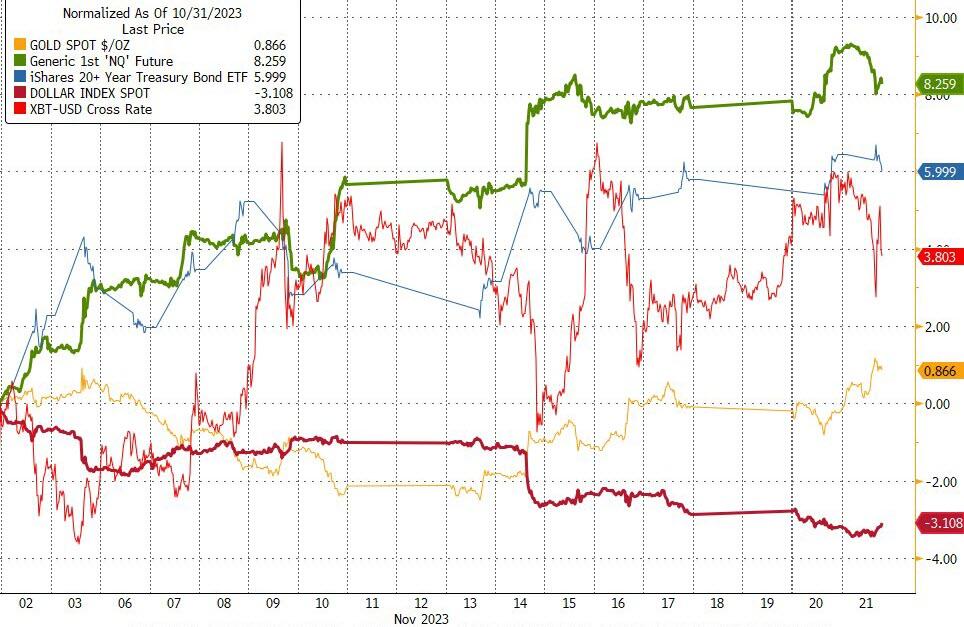

ZeroHedge remarks, “Since the last FOMC meeting, on November 1st, the dollar has tumbled over 3% sending stocks, bonds, and bitcoin all higher (and gold, though only marginally)…

Source: Bloomberg

Rate-change expectations have shifted significantly more dovish with more rate-cuts priced-in sooner in 2024 (with nearly 100bps of cuts priced-in for next year)…”

USD futures consolidated this morning, after rising above the 200.day Moving Average at 103.43. This puts the USD back on a buy signal. This may be a signal to bonds and equities that all is not well. Money flows are paramount in determining the market direction. Although some of these flows may be coming from foreign locations, the rising USD may indicate weakness in the markets.

Crude oil declined to 74.08 after being repelled by the mid-Cycle resistance at 78.21. The decline may continue to early December. The target for this decline may be the Cycle bottom at 66.21. More serious trouble may develop should it cross beneath the March low at 63.57.

ZeroHedge remarks, “Oil prices are lower this morning as the usual malarkey of leaks, rumors, and denials dominates price action ahead of the planned OPEC+ meeting this weekend.

The selling started with a report by Bloomberg claiming that the Saudis expressed dissatisfaction with other members about their oil production levels.

The worry, Bloomberg claims, is that Riyadh might reverse its unilateral 1 million barrel-a-day curb if its counterparts don’t contribute further to the supply reductions.

That sent prices lower.”