8:00 am

Good Morning!

US Tech futures are lower this morning, to 15757.00. Be aware that there is minor support at 05725.00, beneath which no support can be found to 15535.00. This may lend itself to a gap down, leaving an island reversal in the next couple of days. Yesterday’s high at 15904.63 has not overtaken the July 13 high at 15932.06, leaving a potentially bearish outcome. This structure is known as a leading diagonal.

Today’s options expiration shows Maximum Investor Pain at 15680.00. Options are a mixed bag with long gamma starting at 15900.00, while short gamma begins at 15650.00.

ZeroHedge remarks, “Tech vs rates – the Jaws gap

Tech started trading the rates “connection” this summer, but note that NASDAQ has recently decoupled from the US 10 year (inverted). Tech’s overshoot here is somewhat “concerning”.

Source: Refinitiv

Are we decoupling from the bond volatility narrative?

Up until now calmer bond volatility has been key for equities. This relationship has broken down lately…especially when it comes to NASDAQ. Chart shows NASDAQ vs MOVE (inverted).”

SPX futures slipped beneath 4500.oo this morning, reaching a low of 4490.00. Tomorrow is monthly options expiration, so I don’t expect a large move today. Critical support lies at 4458.00, the top of the November 14 gap (up). Today is day 248 of the current Master Cycle. A decline beneath the above-mentioned support indicates a probable reversal into a new Cycle.

Today’s op-ex indicates Maximum Pain at a highly contested 4510.00. Long gamma starts at 4525.00, while short gamma lies beneath 4500.00.

ZeroHedge reports, “S&P futures dropped and global stocks paused their rally on Wednesday as the euphoria over a potential dovish pivot by central banks faded and earnings from a slew of companies undershot expectations. A boost to sentiment from the US averting a government shutdowns was offset by a last minute debacle in the Biden-Xi talks in which the US president (correctly) called his Chinese counterpart a “dictator”; sentiment was also pressured by disappointing guidance and commentary on the US consumer from retail giant Walmart. As of 8:15am, S&P futures ticked 0.2% lower. 10YTreasuries steadied just below 4.5%, after yields increased by almost nine basis points in the previous session. The dollar was little changed and West Texas Intermediate declined toward $76 a barrel.”

VIX futures have declined to a new low at 13.68, which may be the Master Cycle low. Should that be the case, the Cycles Model suggests a rally in the VIX lasting to mid-January.

Noecct week’s op-ex shows short gamma all but extinguished. Long gamma may start as low as 14.00, but becomes serious at 18.00 and currently extends to 30.00.

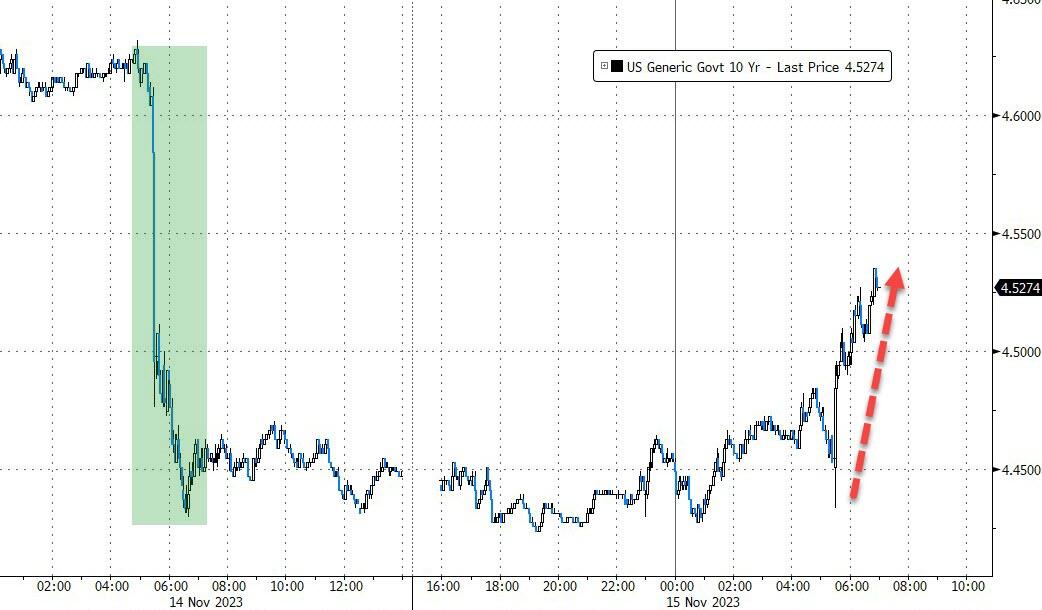

TNX pulled back to test the trendline at 45.45 this morning. Once the trendline has been determined to hold, the rally to the upper trendline may begin, with strength. The Cycles Model suggests TNX may be making new highs at the end of November.

ZeroHhedge remarks, “Short covering on Tuesday drove a powerful rally in Treasuries, but deteriorating liquidity conditions means they face greater downside than upside risk.

The outsized move in bond yields in the US and the rest of the world from a slightly softer-than-expected October inflation print was an unmissable sign of a market that got caught short.

Today’s retail sales number was better than expected (though a decline in headline), potentially wrong-footing the bond market after yesterday’s strong gains.”

USD futures are testing the 200-day Moving Average at 103.42 with a low thus far at 103.99. Today is day 253 of the Master Cycle. There is a strong likelihood of the final low being made yet this week. The Cycles Model suggests that the uptrend may strengthen next week. Remember, the demand for USD (cash) may rise as both stocks and bonds sell off.

Crude Oil futures have slipped beneath the prior low, to 74.64 on day 254 of the current Master Cycle. Crude is nearing a low, possibly at the Cycle Bottom at 65.22. There may be dire consequences should crude decline to or beneath the May low at 63.57.