12:08 pm

The Ag Index broke through a very narrow trading band support at 439.11 on day 279 of the Master Cycle. There is a trendline support at 324.00 which may stop the decline in the next few days. If so, this may be a major turning point for the Ag Index. A follow-up report may come early next week. In the meantime, the midwest corn belt is being hit by unusually cold and wet weather. Normally the corn planting season would be over and the plants emerging from the ground by now. Instead, farmers cannot even get into their fields.

Meanwhile, ZeroHedge points out, “On Tuesday, financial services firm Stephens Inc. lowered their rating of Cal-Maine Foods from overweight to equal weight, pointing to concerns about plunging wholesale egg prices as the reason.

Stephens research analyst covering the consumer staples, food and agribusiness, and grocery/c-store sectors Ben Bienvenu said in a recent conference call with Urner Barry, a market research firm that tracks wholesale food prices, that wholesale egg price trends were “understandably more downbeat.”

“When considering what’s currently playing out for eggs, we think it is best for us move to the sidelines on Cal-Maine as we think risk/reward is now more balanced,” the analyst said. “

9:41 am

BKX slipped beneath its Cycle Bottom support/resistance at 80.35 and is testing the underside resistance today. As it stands today, the Cycles Model offers a probable decline to the middle of June. The Head & Shoulders minimum target may be the possible low at that time.

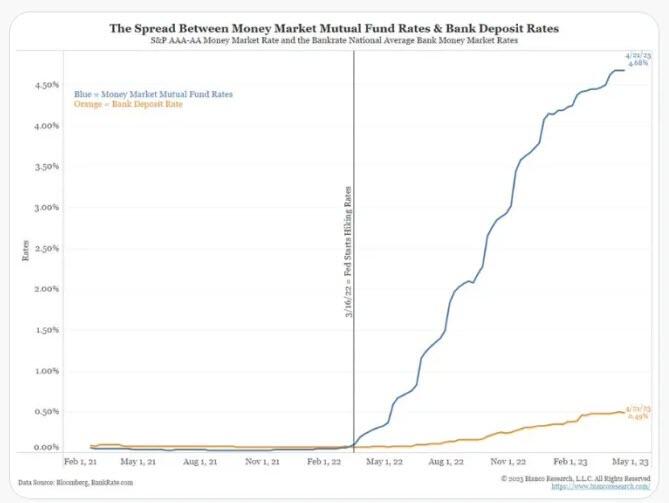

ZeroHedge remarks, “Let’s tune into a mass exodus of deposits at banks for money market mutual funds and what it means…

Spread between bank deposit rates and money market funds from Tweet below.

Jim Bianco has a 21-Tweet Thread on what’s going on with bank deposits. I chimed in on a couple of the Tweets. Here are some of the most important ideas.”

7:45 am

Good Morning!

NDX futures rose off Intermediate-term support at 12765.60 to a high of 12934.40 in the overnight session. The most likely target may be round number resistance at 13000.00, which is near the 50% retracement level. Today may be the last day of the bounce, with trending strength reappearing on Friday and lasting into next week. Investors should not be long beneath 13000.00.

In today’s op-ex, Maximum pain for options investors is at 12860.00. Long gamma may arise at 12900.00, while short gamma may begin at 12850.00.

ZeroHedge observes, “Mightiest tech

The NASDAQ vs Russell futures ratio is breaking above the most recent highs..trading at levels last seen in September 2020. For context, MSFT accounted for 140% of the NDX move yesterday (114 points out of an 81-point move), writes Nocerino.

Source: Refinitiv

There is an equal weight NDX…

…and it is lagging. Mega cap tech becoming more and more important for this market. The ratio continues the powerful break out move.

Source: Refinitiv

It is a narrow bull

Impressive performance by a few. Great chart via JPM showing the current state of narrowness.”

The NDX Hi-Lo Index shows a weakening market. The Cycles Model suggests a worsening condition through the month of June. As the saying goes, “Sell in May and go away.”

ZeroHedge remarks, “Something odd is taking place below the surface of the nasdaq: while the Index is sharply higher today on the back of strong earnings from MSFT and GOOGL, and is just shy of a bull market from the October lows, there is less here than meets the eye. And, as we have noted repeatedly in recent weeks, today’s action cemented what we already knew: Nasdaq breadth defined in this case by the advance/decline ratio, just hit a record low!”

SPX futures are bouncing off the double support at the 50-day Moving Average at 4037.53 this morning. There is an hourly resistance at 4116.53 that may prove to be a stopper. The decline may resume in strength by Friday. The Cycles ae suggesting a possible event over the weekend that may accelerate the decline into next week. The Head & Shoulders neckline may come into play by then.

Today’s op-ex shows Maximum Pain at 4050.00. Long gamma may begin at 4075.00, while short gamma may start at 4025.00.

Friday’s (month-end) op-ex shows Max Pain at 4080.00. Long gamma has the edge above 4100.00, while short gamma is heavy at 4050.00 and worsens at 4100.00 as the shorts are making gains over the longs.

ZeroHedge reports, “US index futures gained on Thursday halting a two-day drop, led by the tech stocks, after Meta’s better-than-expected results helped mitigate investor concerns about the F(ailing)irst Republic Bank, economic outlook, inflation and monetary policy. S&P 500 futures traded just above 4,100, rising 0.7% as of 8:00 a.m. ET, while Nasdaq 100 futures rose 0.9%, extending Wednesday’s gains as the tech-heavy benchmark continues its outperformance of the broader market this year. According to JPM, “this week’s Equity performance highlights the divergence due to low market breadth” something we discussed yesterday. European stocks gained and were set to snap a three-day losing streak as Barclays, AstraZeneca and Unilever all rise after their respective updates. Asian markets were also green after a rebound in Chinese stocks. USD is weaker, longer-dated yields are higher, and commodities are mixed before US GDP and jobless claims to gauge the strength of the US economy. Yields on five-year notes dropped the most in a month on Tuesday, spurred by a wave of quant investors. The Federal Reserve’s preferred inflation gauge, the core PCE deflator, is due Friday.”

VIX futures pulled back to 17.90 and is likely to test hourly support at 17.50 today. Tomorrow may begin a period of strength that may last through next week.

Next week’s op-ex shows Max Pain at 19.00, with lagging short gamma. Long gamma begins at 21.00 and intensifies to 33.00.

TNX probed higher this morning, challenging Intermediate-term resistance at 34.91. The next resistance to be recognized is the 200-day Moving Average at 35.31. A breakout above the resistance zone (34.91-36.26) may lead to a rally in yields lasting to early July. The 7-year Note goes to auction today. Watch closely.

ZeroHedge reports, “One day after a strong 2Y auction, moments ago the Treasury sold $43BN in an even stronger sale of 5Y paper.

Stopping at a high yield of 3.500%, this was not only below last month’s 3.665% but it was also the lowest 5Y yield since August 2022 when the tenor priced at 3.23%. It also stopped through the When Issued 3.506% by 0.6bps, the second straight stop through in a row.

The bid to cover was also solid, rising to 2.54, the highest since January and well above the 2.49 six-auction average.”

Crude Oil is consolidating today after breaking the Broadening Wedge trendline near 75.00. The target for the Broadening Wedge may be 56.00. The Cycles Model suggests the decline may last to the end of May.

Reuters reports, ” Oil prices dropped by almost 4% on Wednesday, extending the previous session’s sharp losses, even after a report showed U.S. crude inventories fell more than expected, as recession fears grew for the world’s biggest economy.

Brent crude settled at $77.69 a barrel, losing $3.08, or 3.8%. U.S. West Texas Intermediate crude settled at $74.30 a barrel, shedding $2.77, or 3.6%.

Energy Information Administration (EIA) data showing U.S. crude inventories fell last week by 5.1 million barrels to 460.9 million barrels helped to limit the price fall, far exceeding analyst forecasts of a 1.5 million drop in a Reuters poll.”

Gold futures continue to decline, approaching Intermediate-term support and a confirmed sell signal at 1981.40. The Cycles Model proposes a double strength event over the weekend which may retest the Cycle Top resistance at 2039.17 early next week. Should that happen, the Cycles Model suggests the decline may resume with confirmation of a sell signal beneath Intermediate-term support. Meanwhile the gold crowd continue their onslaught of misinformation.