2:25 pm

SPX appears to be declining to 4100.00 or possibly deeper, then a probable bounce back to 4130.00 to 4138.00.

1:25 pm

BKX, our liquidity proxy, has been lingering near its Cycle Top resistance at 115.77 for a week. I have been warning that a panic in the bond market may devastate the banks. Not only will their holdings in loans and bonds decline in value (assuming their payments are timely), but the dealer banks must buy what is not purchased by other institutions in the Treasury auctions. We saw an aversion to the 3-year Treasury notes yesterday. The next few auctions may show the true demand for the Treasury auctions, thereby overwhelming the capacity of the dealer banks to absorb the spillover. In conjunction with that, the new Master Cycle may face a decline in BKX lasting up to 2 months. This has the earmarks of a probable panic.

Note: The 10-year Treasury auction was a success. That in no way minimizes the warning.

ZeroHedge notes, “The better-than-expected non-farm payroll report for January along with the smaller interest rate hike delivered by the Federal Reserve at its February meeting increased optimism that the central bank can bring price inflation back to 2% without tanking the economy. But the shrinking money supply undercuts this soft landing narrative.

While Fed rate hikes and balance sheet reductions aren’t likely big enough to permanently take down inflation, they are shrinking the money supply and that generally means a recession is looming.

Money supply growth went negative for the first time in 28 years in November and fell again in December.”

11:11 am

The Ag Index completed its Master Cycle on January 31, in line with the high inequities. The new master Cycle extends to early April and is twice as long as the new equities Cycle. While Equites may be entering a panic phase it is uncertain whether the Ag Index may fully participate or only partially so. I am looking for a decline down to the 50-day Moving Average at 460.10. Should that level hold, the Cycle may rally for the duration, instead. Stay tuned for further developments.

ZeroHedge remarks, “The worst case scenario that many of the experts feared is starting to play out right in front of our eyes. Throughout 2022, I repeatedly warned my regular readers that there were all sorts of indications that the emerging global food crisis would go to entirely new level in 2023, and that is precisely what is happening. In response to tightening supplies of food, prices are surging all over the planet and the number of desperately hungry people is exploding. Unfortunately, this crisis is not going to be just temporary. As I will explain at the end of this article, the global nightmare that we are facing is inevitably going to intensify in the years ahead.

Most of us in the western world simply do not understand how badly conditions have already deteriorated in much of the world.”

8:20 am

Good Morning!

SPX futures have declined to a morning low of 4142.90, in line with options Max Pain at 4145.00. A hourly Cycle may have completed at the close leaving the probability of a further decline on the table. Yesterday’s spike high failed to overcome The February 2 Master and Primary Cycle high. I was asked what the catalyst for this and my answer is simply “exhaustion.” The 50% retracement of last year’s entire decline is 4142.03. Each Fibonacci level (38.2%, 50% and 61.8%) offer a progressively higher level of resistance. In this case, the Cycles completed the time element as well, leaving no further energy for the rally. The tide has turned and now we look at supports which lie below. The two main levels of support lie at the December low at 3764.49 and the October low at 3491.58. The Model suggests one of those two supports may be hit by monthly options expiration on February 17, where the Model suggests the decline may accelerate.

Today’s options chain shows Maximum pain for options investors at 4135.00. Long gamma may begin at 4150.00, while short gamma begins at 4100.00. Retail buyers appear to remain on the long side, but there are some large short positions down to 3960.00 and possibly lower. Next Friday’s (Feb 17) op-ex shows huge “collar” positions every 50 points all the way down to 4000.00 as a possible attempt (by dealers) to control the decline.

ZeroHedge reports, “US futures dipped after Tuesday’s furious last hour reversal rally sparked by Powell’s “disinflation” commentary which refrained from pushing back against investor optimism, even as stocks in Europe and Asia were still buoyant, with the FTSE 100 posting a new record high. S&P 500 eminis slipped 0.4% at 7:45 a.m. while Nasdaq futures were 0.2% lower. The underlying benchmarks jumped 1.3% and 2.1%, respectively, in the latest session as investors brushed off Fed chief Jerome Powell’s comments that borrowing costs may need to peak higher than previously expected, choosing to focus instead on his outlook that 2023 will be a year of significant declines in inflation. The dollar slid, Treasuries reversed some of Tuesday’s losses, and an index of commodities rose a second day.”

VIX futures have consolidated within yesterday’s trading range and are treading above the close. The Cycles Model infers the rally may continue through the end of February. While VIX may be on an aggressive buy signal, confirmation comes on a rise above the 50-day Moving Average at 24.80.

TNX is pulling back from yesterday’s new high and may be declining for a retest of the 50-day Moving Average at 35.89. That may be only a short term move, since the Cycles Model shows a strong trending strength pattern forming by this weekend.

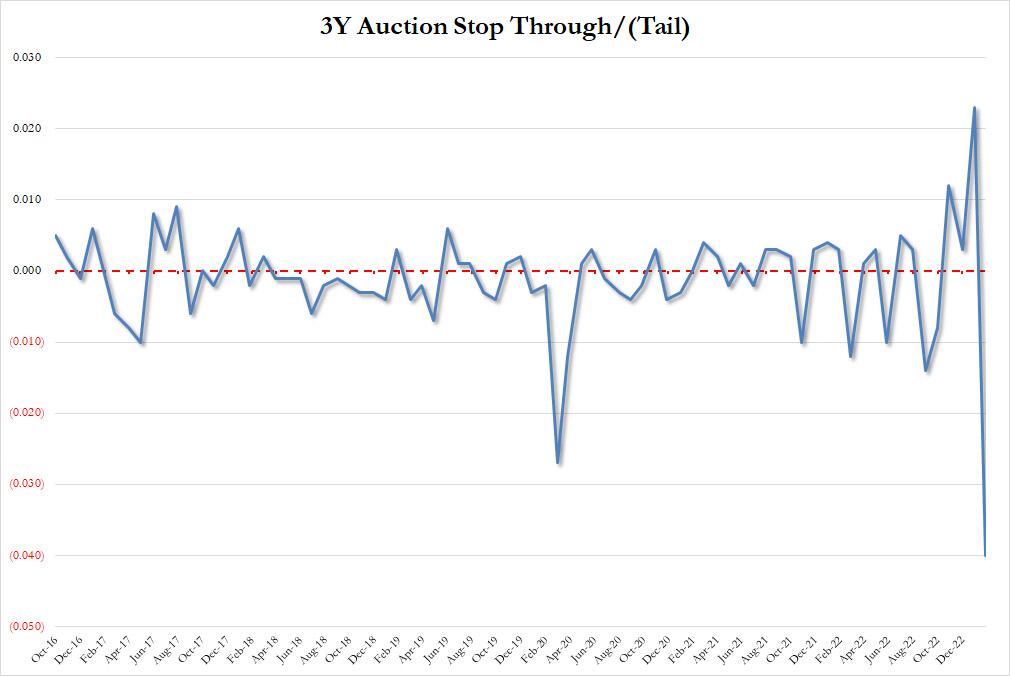

ZeroHedge reports, “One month ago, when commenting on January’s 3Y auction, we said that it could “only be described as an absolute whopper” with record foreign bidder demand and “blowout” metrics including record indirects and a record stop through. Today’s 3Y auction was an absolute mirror image, with the auction about as horrific as they come.

The high yield of 4.073% was not only well above last month’s 3.977%, but also stopped through the When Issued 4.033% by a 4bps which was a record in our data set which goes back to 2016. More remarkably, it was the polar opposite of last month when the 3Y was also a record, only in the other, stop through direction!”

USD futures are declining to the bottom of yesterday’s trading range this morning. The most likely outcome may be a retest of the Declining Wedge trendline near 102.00. The Cycles Model shows a possible low by the weekend, with a resumption of the rally next week on growing strength. A buy signal is confirmed above the 50-day Moving Average, currently at 103.68.

WTIC futures are challenging the 50-day Moving Average at 77.30 this morning. A close back beneath that level indicates the decline may resume. The Cycles Model suggests a possible new low by the end of February while the strength of the decline beginning to accelerate by early next week. The consequences of a break of the trendline near 72.00 are enormous.

ZeroHedge comments, “Oil prices soared today after reassuring comments from Fed Chair Powell built on growing confidence in China’s reopening (as Aramco increased its selling prices for shipments to Asia) and that was all helped by a weaker dollar. Additionally, the devastating earthquake on Monday that left thousands dead in Turkey and Syria also led to a halt in operations at Turkey’s Ceyhan oil export terminal, with has a capacity of 1 million barrels a day.

“In the grand scheme, essentially you have contrasting forces of rising inventories and a bullish outlook on demand,” said Daniel Ghali, a commodity strategist at TD Securities.

The last few weeks have seen some rather shocking series of inventory builds across crude and the products – not exactly reassuring for the demand picture (even if some of it was affected by the nationwide deep freeze).”

Gold futures are consolidating this morning inside yesterday’s trading range just above Intermediate-term support at 1880.00. The Cycles Model urges caution for the longs, as trending strength resumes on Thursday after Tuesday’s Master Cycle high. Gold is on an aggressive sell to be confirmed beneath Intermediate-term support and the 50-day Moving Average at 1847.48. The new Master Cycle suggests the decline may continue through the end of February with a possible extension through early April. Unfortunately, most commentary only shows what has already happened, assuming it may continue. Remember, past performance is no guarantee of future results.

Zerohedge observes, “Central banks closed out 2022 with reported net purchases of 28 tons of gold in December. Including large unreported purchases, this brought total central bank gold buying in 2022 to 1,136 tons. It was the second-highest level of net purchases on record dating back to 1950, and the 13th straight year of net central bank gold purchases.

China officially started buying gold again in November and made another large purchase of 30 tons in December. That raised China’s total gold reserves to over 2,000 tons for the first time.”