1:30 pm

ZeroHedge remarks, “While some were more interested how banks did in Q4 – a quarter which we already knew would see catastrophic banking revenues (due to the lack of IPOs and bond offerings thanks to the plunging market), and mediocre at best for FICC and equity trading offset by very strong net interest income courtesy of soaring credit card fees – we were much more curious in how banks saw the future not by their always cheerful conference calls, but by how much loan loss reserves they took out in anticipation of the coming recession.

The results were concerning: let’s start with the largest US commercial bank, JPMorgan, which in Q4 almost double its reserve build from $808MM to $1.4 billion, the biggest reserve build since the fateful Q2 2020 quarter when covid locked down the US economy and nobody knew what would happen.

10:21 am

BKX , our liquidity proxy, put in its Master Cycle high yesterday, day 269 of the former Master Cycle. It has declined beneath mid-Cycle support/resistance at 105.59 and is on a sell signal. It may retest yesterday’s high, but the reversal has been overdue. Today starts the earnings season for banks and one can see massive increases in loan loss reserves due to deteriorating conditions and rising rates. The Cycles Model warns that something may break over the weekend. Here ae the headline articles:

Losses ‘Accelerate’ For Goldman’s Credit-Card Division

JPM Slides … As It Boosts Credit Loss Reserves By $1.4BN

BofA Reports Solid Q4 Earnings… As Credit Loss Provisions Soars Above $1 Billion

BOJ Loses Control Of Bond Market As New YCC Band Breaks Amid Selling Panic

FitchRatings reports, “Fitch Ratings-New York/Chicago-10 January 2023: U.S. banks face rising deposit costs and sustained higher unrealized losses on securities portfolios given the growing probability that the Federal Reserve (Fed) maintains elevated interest rates for an extended period to combat inflation, Fitch Ratings says.

Weaker credit performance is expected to be the primary focal point for U.S. banks’ financial performance in 2023, but the industry response to meaningfully declining deposits will also be an important issue to monitor.”

9:00 am

Good Morning!

SPX futures have declined to the mid-Cycle support at 3943.18 after reversing at the 200-day Moving Average at 3994.39 at 2:00 pm yesterday. What is interesting about that time is that it is 12.9 market days from the December 22 low and 30 days (4.3 weeks) from the December 13 high. Crossing beneath mid-Cycle support gives us a sell signal. We are now in the midst of earnings reports, so buckle up for a rough ride for the rest of the month.

In today’s options-driven market, Maximum Pain for options investors is at 3935.00. Long gamma starts at 3950.00, while short gamma begins at 3900.00. One may conclude that this morning’s decline may be dealer driven to maximize options pain.

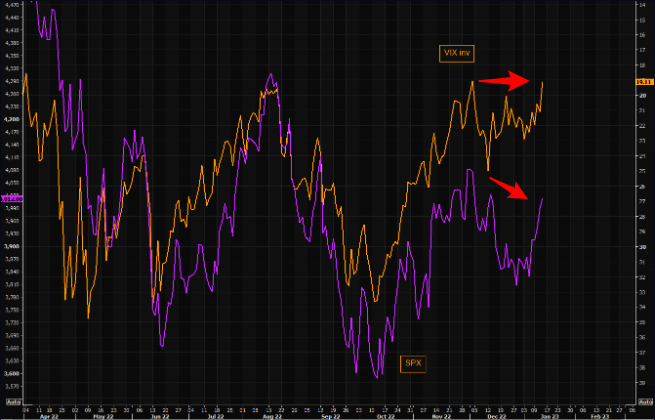

VIX futures have rebounded to a morning high at 19.41 after making a new low not seen since April 4. Yesterday’s new low takes the form of a double zigzag, which was totally unexpected since the prior low in early December had fulfilled all the requirements of a completed Triangle formation. Unfortunately, Wave (E)s are rogues and can go “outside the box.” Today is day 256 of the current Master Cycle. A closer look at the Cycles Model suggests the reversal may come over the weekend, catching many unawares.

“Buy Protection when you can…”

Next Wednesday’s monthly VIX expiration shows Max Pain at 24.00 with 101,725 put contracts (short gamma) starting there. Long gamma begins at 24.00 with 114,243 call contracts. A low VIX at op-ex would be an unmitigated disaster for the dealers, as there are over 600,000 put contracts between 18.00 and 24.00. However interest in calls is growing.

ZeroHedge remarks, “Last time VIX was here…

Expect to see a few of those calls soon, but they are wrong. Volatility is mean reverting, while the underlying assets can trend. Anyway, the VIX is puking further today and could be closing at the lowest levels since April 2022. Second chart shows the slightly shorter term view. The gap between VIX and SPX that started forming in mid December remains wide as people “suck fear” out of this market.”

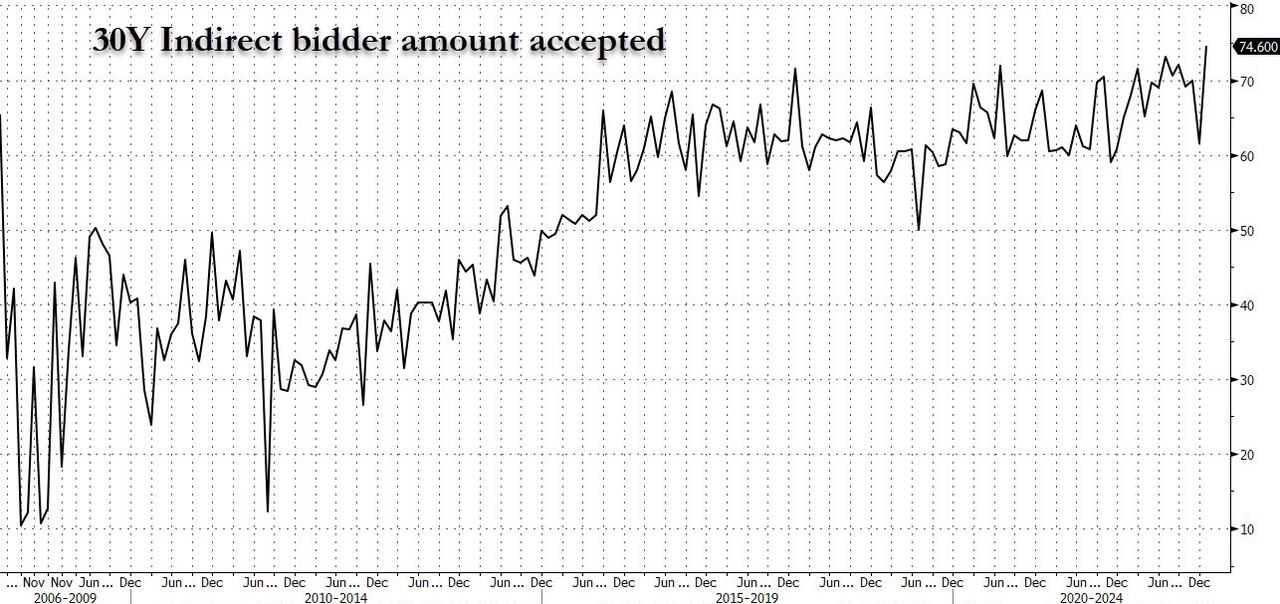

TNX futures may have bottomed out last night at 34.18, but the morning cash market shows a higher low, leaving yesterday as a potential Master Cycle low at day 266. Yesterday’s 30-year Treasury auction may have laid a trap for unexpected investors, not anticipating the market could turn on a dime.

ZeroHedge observes, “What a blowout auction.

After a stellar 3Y, an impressive 10Y (both of which came in far stronger than expected, prompting us to correctly say there were zero jitters about today’s CPI print in the bond market), moments ago we got an absolutely blowout, record 30Y auction.

The high yield of 3.585% was fractionally above last month’s 3.513%, but stopped through the When Issued by 2.4bps, one of the biggest stop throughs on record which was especially remarkable when considering the powerful rally across the curve going into the auction and lack of concession as the curve had tried to steepen on several occasions, and failed.

Th Bid to Cover of 2.451 was well above last month’s 2.249 and was the highest going back all the way to September 2021.

But it was the internals that were blowout, with foreign buyers, or Indirect bidders including central banks, private investors and sov wealth units, awarded a record 74.63%, the highest on record (and far above last momth’s 61.57%) as foreigners just couldn’t get enough.”

USD futures may have made a new Master Cycle low in the overnight session at 101.72. However, it appears to be bouncing off that low. Today is day 260 of the current Master Cycle. The Model suggests a possible reversal over the weekend, with potential strength.