9:10 am

SPX spiked higher on the “in line” CPI print. It challenged the 200-day Moving Average at 3987.35, then reversed. This may trap “lazy long” investors who may not be ready for a Key Reversal ( when the share price accelerates in an ascending trend, exceeds the current peak and after a high opening on the next day, the price falls and closes below the previous day’s trading range), as we did in December.

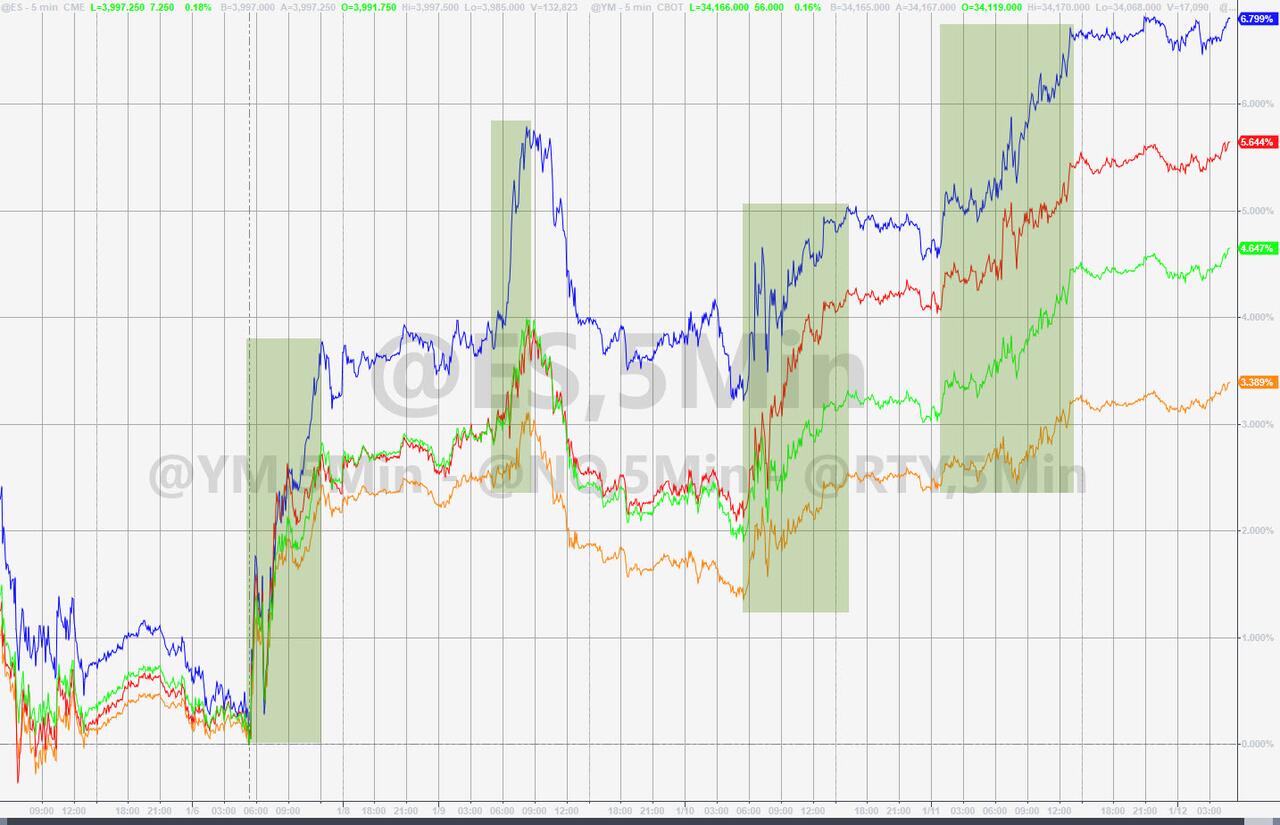

ZeroHedge remarks, “Once again, US equity markets have squeezed dramatically higher in the last few days (post-payrolls) ahead of this morning’s all-important CPI print…

All of which, as Nomura’s Charlie McElligott notes, shows strong evidence of “fear of the right tail” yet again in Equities, due to “trending” expectation of a “dovish CPI” print today (set-up for disappointment on “just in-line”?)”

8:15 am

Good Morning!

SPX futures rose to 3984.10 this morning, above the 61.8% Fibonacci retracement value of 3971.40. The CPI print may dictate the direction of the markets. A lower CPI may give the SPX a burst of energy taking it to a possible high near 4150.00 over the next two weeks. A higher CPI print may push the SPX o a new low.

Today’s op-ex shows Maximum pain for options investors at 3935.00. Long gamma begins at 3950.00, while short gamma starts at 3900.00. Friday’s Max Pain is near 3900.00 with long gamma starting at 3950.00 and short gamma beginning at 3850.00.

ZeroHedge speculates. “We previously showed a CPI-dependent market matrix from both JPMorgan and Goldman, as well as an analysis by Morgan Stanley why tomorrow’s CPI print is likely to miss big. Now, we take a look at what consensus expects.

According to Wall Street economists, tomorrow at 830am, the BLS will report the following data for the month of December:

- CPI MoM: exp. -0.1%, down from 0.1% in November

- CPI Core MoM: exp. 0.3%, up from 0.2%

- CPI YoY: exp. 6.5%, down from 7.1%

- CPI Core MoM: exp. 5.7%, down from 6.1%

Broader picture, market is already pricing in a lower inflation path than Fed’s SEP shows for 2023. Specifically, CPI fixings imply headline PCE inflation below the Fed’s 2% goal by July and around 2% goal by year-end.”

ZeroHedge reports, “US futures are trading near session highs after earlier fluctuating between gains and losses ahead of make-or-break inflation data which many expect will show price pressures continuing to ease. S&P 500 futures traded 0.1% higher as of 7:30am ET, just shy of 4,000, one day after the S&P 500 clocked this year’s first back-to-back gains on Tuesday and Wednesday. The gains stem from bets that cooling inflation ill give the Federal Reserve room to slow its pace of rate hikes, a take substantiated by Boston Fed chief Susan Collins, who said she was leaning toward a quarter-point move at the bank’s Feb. 1 meeting. Treasuries steadied after gains in Wednesday’s session, with the 10Y trading at 3.52%, while a gauge of dollar strength edged lower as investors looked beyond the drumbeat of hawkish comments from Federal Reserve officials. The yen rallied on a report that the Bank of Japan will look into the side effects of its ultra-loose monetary policy. Commodities are mostly higher with the dollar weaker.”

VIX futures consolidated in a narrow range ahead of the CPI print. The corrective pattern appears complete as of Tuesday, day 253 of the Master Cycle. A reversal may be imminent.

ZeroHedge asks, did you know,”In the final days of 2022, Goldman’s economists predicted that “the biggest political risk” of 2023 will be the Congressional showdown over America’s favorite periodic drama: the debt limit.

This is what the bank’s chief economist Jan Hatzius said then: “The debt limit likely poses the greatest political risk next year, and we expect it to rival the 2011 episode in its disruption to financial markets and the economy. That said, we do not expect Congress to enact major fiscal changes. Republicans might press for spending cuts in a debt limit deal, but we do not expect substantial cuts next year. The White House might press for increased fiscal support, but this also looks unlikely as we believe a soft landing is more likely and a divided Congress would have difficulty responding to a recession even if one occurs.”

TNX extended its (declining) Master Cycle this morning, on day 266 of the current Master Cycle. A reversal may be imminent, with a possible four weeks of rally ahead.

ZeroHedge reports, “Headline and Core CPI printed ‘as expected’ (which is likely disappointing for the whisper numbers and remember the last CPI printed ‘cooler than expected’). Goods inflation continues to slow but Services inflation continues to soar (highest in over 40 years). Shelter costs continue to soar.

* * *

Expectations for this morning’s headline CPI ranges from +6.3% to +6.8% YoY, with consensus seeing a 0.1% decline MoM – something the world and his pet rabbit has bid stocks up into anticipating this as the signal for an about face by The Fed on their higher for longer narrative as it ‘proves’ inflation has peaked.

The headline print came in right as expected with a 0.1% decline MoM (leaving the YoY print at +6.5% as expected)…”

USD futures made a new Master Cycle low at 104.06 on day 259. This sets up a potential reversal into an USD rally through the end of February.