3:09 pm

TNX faded after 10-year auction, then stabilized. The Cycles Model remains neutral at this point, but the uptrend may resume.

ZeroHedge comments, “One day after what may have been the strongest 3Y auction in history (and if not, then certainly one of the top 3), moments ago the Treasury sold $32BN in 10Y paper (in the form of 9Y-10M reopening of Cusip FV8), in what was another stellar auction.

The high yield of 3.575%, was the second consecutive drop since the 10Y auction peaked at 4.14% in November, and was also down from 3.625% in December. More importantly perhaps, compared to the When Issued 3.580%, today’s auction stopped through by 0.5bps. This was the first 10Y auction that did not tail since August, and it certainly was better than last month’s auction when the tail was a record 3.7bps:”

2:50 pm

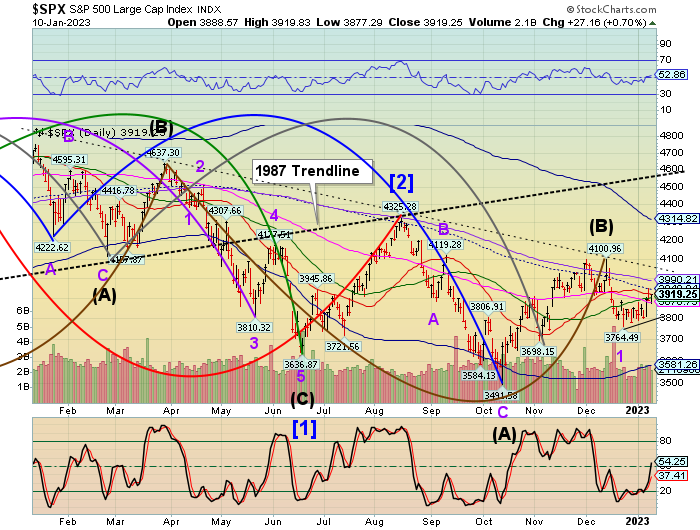

SPX is approaching its 61.8% retracement value at 3971.40 and has completed 19 market days since its inception on December 13. It still has 17.2 probable days of decline ahead, starting this afternoon. Most investors are looking up. A reversal here may surprise many, followed by the CPI print tomorrow morning.

ZeroHedge remarks, “Nomura’s Charlie McElligott began this morning’s note by warning investors that tomorrow’s CPI print “is a bigger deal than the market is already giving it credit for.”

Specifically, he notes that while straddle pricing is for around a ~2.0% SPX move, we’ve continued to “over-realize vs implieds” consistently on CPI prints, which is why owning Gamma for this day has been the right trade for most of the past 9 months…”

10:14 am

The Ag index may have put in its Master Cycle low yesterday, on day 266. Should that be correct, the new Master Cycle may only last to the end of the Month, but may be buoyed with unexpected strength.

ZeroHedge remarks, “Most Americans have watched their food expenses at grocery stores ballon in recent years. The one item that likely shocked consumers the most is the skyrocketing price of a dozen eggs.

Avian flu has decimated the US egg-laying hen population at commercial farms. Tens of millions of hens have been culled to prevent one of the worst bird flu outbreaks on record from spreading, though efforts have failed as the virus continues to decimate US egg production, sending retail prices sky-high.

Readers have known about the dire egg situation for many quarters, but the evolving story is that people are now posting images of supermarkets across the country running out of eggs.”

8:10 am

Good Morning!

SPX futures are hovering in a narrow range near the close. The high at 3950.57 remains intact, but there seems to be a hesitancy to decline. There are three weeks left in the current Master Cycle. Whichever way the market goes may set the tone for the rest of the year.

ZeroHedge reports, “US equity futures were set to rise for a second day as upbeat sentiment ahead of tomorrow’s key CPI print – which JPM gives 85% odds of pushing stocks at least 1.5% higher – lifted global markets despite a freak outage of key FAA advisory system this morning led to a nationwide ground halt for all domestic flights (until at least 9am) pre. Contracts on the S&P 500 and Nasdaq 100 ticked up 0.1% as of 7:15am ET while Europe’s Stoxx 600 Index rose 0.8%. The FTSE 100 climbed within striking distance of a record high; Asian equities were supported by China lifting Covid restrictions. Among the top corporate news, Credit Suisse weighs cutting by half the bonus pool for 2022 after a turbulent year and Apple plans to start using its own custom displays in mobile devices as early as next year. Treasury yields dropped and the dollar gained for the second day in a row.”

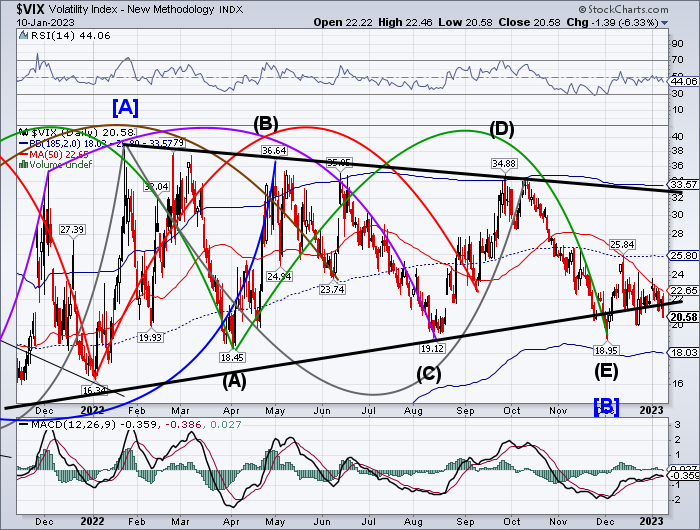

VIX futures appear stuck at the lower end of yesterday’s trading range. This may be due to the weekly op-ex this morning. At the last count, there were 40,229 put contracts with a strike at 21.00 expiring this morning. This may be a good example of short gamma suppressing the VIX. At the same time, VIX may spring out of its box as the expiry is settled. Today is day 254 of the Master Cycle, suggesting a low may be put in by the end of the week.

Today’s op-ex shows why the VIX remains near the low, as there are 40,330 put contracts at the 21.00 strike price. While investors are loading up on puts for next week’s op-ex, there are some very large investors buying calls for next week’s expiry. Someone invested over over a half million dollars for nearly 225,000 contracts at a strike of $70.00!

TNX is making a corrective pullback from yesterday’s test of the trendline. Having made its Master Cycle low on January 9, it may be gathering energy for the next leg up. The new Master Cycle is about 4 weeks long and the Cycles Model suggests trending strength may be about to appear.

ZeroHedge observes, “And we’re off: the first coupon auction of 2023 is in the history books and what a blowout it was.

Today’s sale of $40 billion in 3Y paper can only be described as an absolute whopper, starting at the top: the 3.997% high yield was the 2nd consecutive drop in the yield, and the first sub-4.00% since September; more importantly it stopped through the 4.000% When Issued by 2.3bps, the biggest stop through since at least 2016 (which is how far back our series goes.)

The Bid to Cover was also stellar: at 2.839, it was not only above last month’s 2.551 but also above the six-auction average of 2.518; in fact it was the highest since April 2018.

The internals were also stellar, with Indirects taking down a record 69.5%, and with Directs awarded 13.8%, that meant that Dealers were left with just 17.3%, the lowest on record.”

USD futures may be challenging the trendline near 103.00. Today is day 258 in the current Master Cycle. I have marked Monday’s low as the possible terminus of the Cycle, but await further developments, including a clear rally above the trendline for confirmation.

WTI futures hit a new high at 77.14 this morning as it emerges out of a probable Master Cycle low on January 5. Crossing above Intermediate-term resistance at 76.63 may have created a buy signal, to be confirmed above the 50-day Moving Average at 80.35. If so, the new Master Cycle may be nearly two months long and bullish for crude oil.

ZeroHedge remarks, “Oil prices eked out gains today (4th straight day higher) with WTI back above $75 as fears of a hawkish Powell speech passed painlessly (despite some hawkish FedSpeak from his underlings) and a flat dollar didn’t impact direction.

“Technically, the energy complex remains stuck in neutral, with a wide range for prices to swing inside of without creating a new trend,” analysts at wholesale-fuel distributor TACenergy wrote in a note to clients.

“Fundamentally, the case for prices bottoming is getting stronger as lingering supply issues coincide with demand picking up both domestically and abroad.”