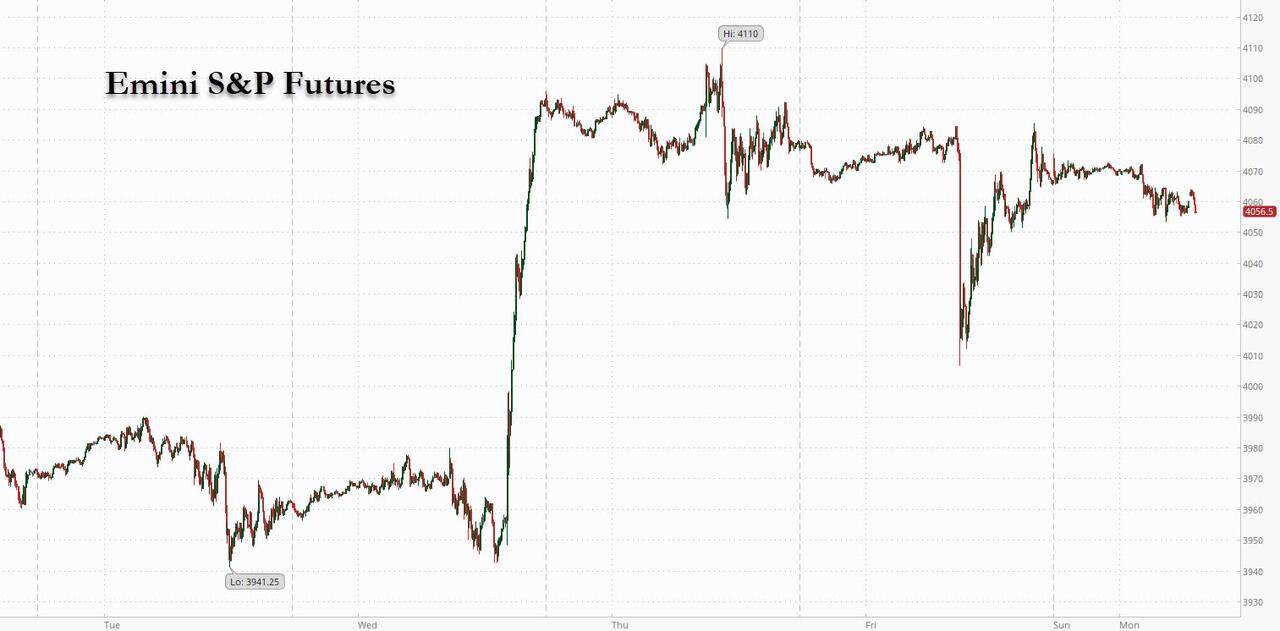

2:17 pm

SPX is testing Short-term support at 3990.95. Crossing beneath it would be a further confirmation of the sell signal. Mike Wilson was the first analyst to mention a rally to 4100.00. He is now saying, “It is done.”

ZeroHedge observes, “Two months ago, and just days after the biggest permabull on Wall Street, JPM’s Marko Kolanovic, finally turned bearish just as the S&P hit fresh 2022 lows after pimping stocks non-stop all year into the biggest bear market in years, and said to fade US equity exposure – a move which we correctly said marked the bottom in stocks…

… Morgan Stanley’s Mike Wilson, arguably the biggest bear on Wall Street (with the exception of BofA’s Michael Hartnett and SocGen’s Albert Edwards), said that he “Expects A Rally Sending S&P500 As High As 4,150.” And, as shown in the chart below, Wilson was once again right in picking a key market inflection point (while Kolanovic was as usual wrong).

12:30 pm

SPX has declined beneath it 200-day Moving Average at 4044.00 and its mid-Cycle support at 4024.00. This confirms a sell signal. The decline may last a week, in which case the target may be the 50-day Moving Average at 3814.93. However, there are multiple indicators of a longer decline, possibly 3 weeks. In that case, the target may be the Cycle Bottom at 3520.42.

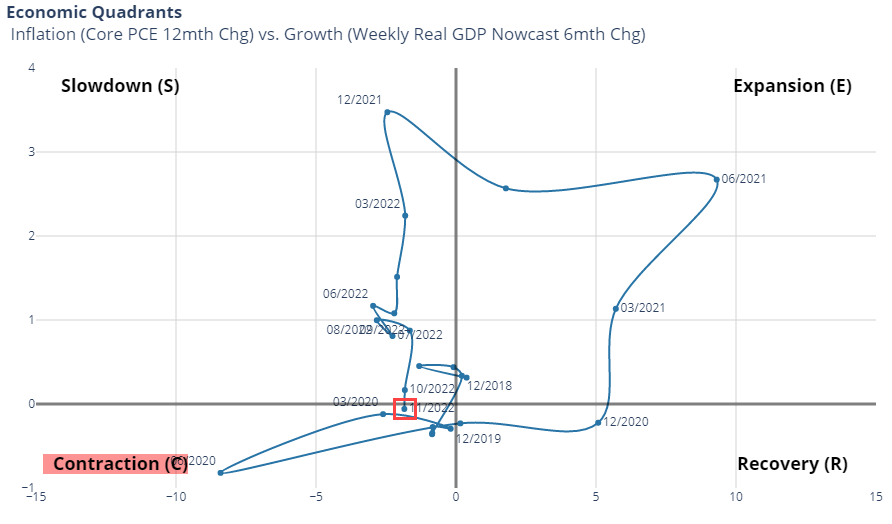

ZeroHedge remarks, “For the first time since the COVID lockdowns, Nomura’s Economic Quadrant work has transitioned from “Slowdown” to outright “Contraction”…

This follows the broad weakness signaled by the last week’s Manufacturing and Services surveys with the US economy’s composite PMI the weakest of the major global economies…

11:00 am

WTI futures may have made an early Master Cycle low on November 28, day 249 of the Master Cycle. The retracement of the rally from the 2020 low was 46% and the structure appears complete. The reversal from the Cycle Bottom suggests a major turning point for crude. However, there are some major cross-currents that may keep WTI down until the end of the year.

10:47 am

BKX, our liquidity proxy, has crossed beneath its Intermediate-term support at 104.64, confirming its sell signal. The Current decline may last through the end of the year. The 50-day Moving Average is at 102.45. It is likely that the next test of support may come from the Cycle Bottom at 92.40. It is possible that there are many banks with commercial loans may be in trouble by the year end, as many small businesses may shutter after a weak Christmas season.

8:40 am

Good Morning!

You may notice the changes on the chart. A thorough analysis over the weekend leads me to believe that the initial decline of a Primary degree, Wave [1], was completed on October 13. Intermediate Wave (A) may have been completed last week at 248 days in the current Master Cycle. Intermediate Wave (B) may now be due. It may last as little as one week with the Master Cycle low (258 days) ending at that point, or possibly to the end of the year. We will know in the next 1-2 weeks. In that case, Wave (B) may decline to the 50-day Moving Average at 3810.60, or possible lower. A Cycle of 12.9 months may be completed by the first week of February at a nominal new high. The 50% retracement of the January-October decline is at 4155.00. A 61.8% Fibonacci retracement would take the SPX to 4311.00, possibly reaching the 1987 trendline. To summarize, there may be a decline of a week or more, followed by a rally to one of the two targets by the first week of February.

SPX futures are down with a morning low of 4041.00. A sell signal may be confirmed beneath mid-Cycle support at 4026.20. Due care is noted as the decline approaches the 50-day Moving Average at 3810.60.

Today’s op-ex shows Max Pain at 4035.00. Long gamma begins at 4050.00, while short gamma starts at 4000.00. Dealers may attempt to bring SPX down to neutral territory between the tow gammas.

ZeroHedge reorts, “US stock futures fell on Monday as investors weighed the outlook for economic growth against the possibility of a softening in the Federal Reserve’s policy, or in other words, whether bad news is again bad news. At the same time, and just one week after China was swept by violent anti-covid zero protests, Chinese stocks in listed in the US rose sharply after Hong Kong-listed peers rallied and the offshore yuan strengthened past the key 7.00 level after Chinese authorities eased Covid testing requirements across major cities over the weekend. The financial hub of Shanghai scrapped PCR testing requirements to enter outdoor public venues such as parks or use public transportation starting Monday. Hangzhou, home to tech giant Alibaba dropped obligations to enter most public venues including offices and supermarkets, while Shanghai also eased rules. As a result, Hong Kong’s Hang Seng Tech Index closed at session highs, soaring some 9.2%, the biggest jump since Nov. 11, after China eased Covid testing requirements across major cities over the weekend.

Meanwhile in the US, Nasdaq 100 futures were down 0.4% by 7:30 a.m. in New York, while S&P 500 futures dipped 0.5%. The indexes shrugged off a hotter-than-expected jobs report on Friday as investors and erased almost all early losses as they remained optimistic that the Fed would slow the pace of interest rate hikes at its meeting this month. The dollar remained near session lows, boosting most Group-of-10 currencies. Treasury yields climbed across the curve. Oil advanced after OPEC+ kept its 2 million production cut and amid growing signs China is reopening, while gold was little changed. Bitcoin rose more than 1%, gaining for a second day.

The S&P 500 is on course for its biggest fourth-quarter gain since 1999 as signs of a cooling in US inflation have led to a pullback in bond yields, but market participants warn the outlook for next year remains uncertain amid the risk to corporate earnings from the specter of a recession.”

VIX futures have risen in the weekend session, but have not achieved new highs. VIX may have another two weeks to its Master Cycle Pivot. However, it has met the requirements of a Primary Cycle (lesser to the Master Cycle). It may allow for 2-3 weeks of a bounce from here.

This week’s op-ex is light and doesn’t offer a clear direction. However, the monthly op-ex (December 21) shows Max Pain at 25.00, with huge long positions above and short positions beneath. There may be a battle going on with long gamma loaded up to 70.00.

TNX has reversed from a probable Master Cycle low (276 days) on Friday. If so, it begins a rally with growing strength through the end of the year. As TNX rises, so does the VIX.

ZeroHedge observes, “After Powell’s words sparked panic-buying – and dramatic easing of financial conditions – some are wondering if The Wall Street Journal’s Nick Timiraos’ report this morning is an attempt tp jawbone back the market’s dovish perception.

Federal Reserve officials have signaled plans to raise their benchmark interest rate by 0.5 percentage point at their meeting next week, but elevated wage pressures could lead them to continue lifting it to higher levels than investors currently expect.

…

brisk wage growth or higher inflation in labor-intensive service sectors of the economy could lead more of them to support raising their benchmark rate next year above the 5% currently anticipated by investors.”

USD futures have risen, but remain beneath the 200-day Moving Average at 105.26 and mid-Cycle resistance at 105.89. Today is day 250 of the Master Cycle, so we may expect a reversal in the next week or so. Should the decline take another week. we may see the lower channel trendline at 102.00 being tested.