2:53 pm

NDX has slipped above the Lip/Neckline at 13020.00 to reach the 38.2% retracement value at 13213.31. I currently have no higher target for this rally. Mid-Cycle resistance at 14002.00 may be a faint possibility. Friday also stands as a potential reversal day. However, a decline beneath the trendline at 13020.00 is useful as a sell signal.

ZeroHedge observes, “NASDAQ – huge levels watch

NASDAQ is back to the 100 day moving average. As Bear Traps notes, this has been the longest period of tech trading below the 100 day moving average since Lehman. 13000/13200 is a huge resistance area to watch. Why not a flag here, another push higher, possibly overshoot the trend line and then another frustrating move lower. That would definitely be the main pain trade…

2:41 pm

SPX has subdivided into an Ending Diagonal with a potential target near 4200.00. The Cycles Model infers that the reversal may come on Friday, although it may come sooner. The main resistance is now at 4225.62, the 50% retracement value and location of the Lip/Neckline of the Head & Shoulders formation. In the meantime, a reversal beneath the Cycle Top at 4130.75 may call an end to this rally. The 100-day Moving Average at 4118.00 may confirm the sell signal, should SPX decline beneath it.

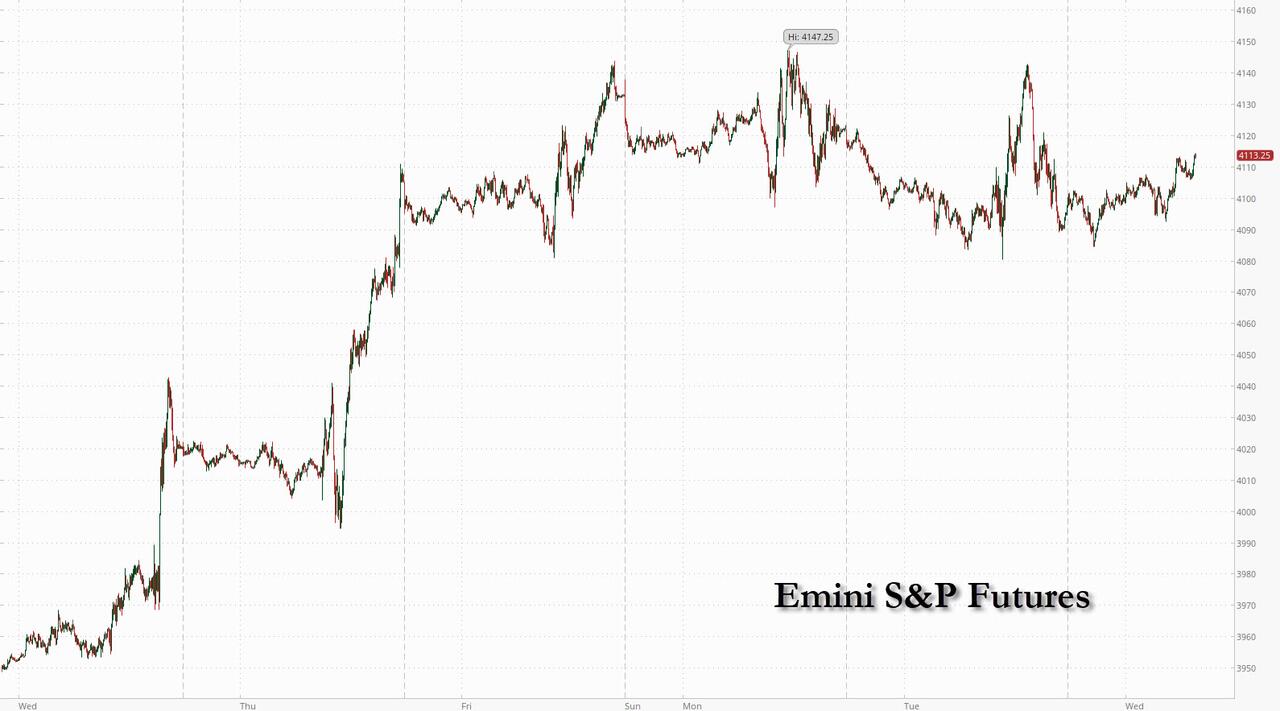

8:40 am

Good Morning!

SPX futures rose to an overnight high of 4118.90, just beneath the 100-day Moving Average at 119.80. It may be on an aggressive sell signal, subject to closing beneath the 100-day. Today is day 254 of the Master Cycle. Thus far, the high occurred on Monday, day 252, which also marked an inverted Trading Cycle high.

In today’s op-ex, Max Pain is at 4090.00 in a thinly populated market. Calls rule above 4120.00 while puts have the majority beneath 4075.00.

ZeroHedge reports, “If yesterday morning markets were losing their mind over the potential risk of World War 3 ahead of Nancy Pelosi’s arrival in Taiwan, this morning it has been a mirror image, with risk assets rising and fears unclenching as investor anxiety over tense US-China ties eased after Pelosi left Taiwan less than 24 hours after arriving after pledging solidarity and hailing its democracy, leaving a trail of Chinese anger over her brief visit to the self-ruled island that Beijing claims as its own. Meanwhile, despite all the jawboning, China’s response to Pelosi’s Taiwan visit fell short of more aggressive expectations raised by nationalists like Hu Xijin, the former editor-in-chief of the Global Times, giving markets a breather. Among them:

- Trade: Beijing added boycotts to fish and fruit imports from Taiwan and banned natural sand exports. It also prohibited dealings with some Taiwanese companies including Hyweb.

- Markets: China’s potential to weaponize its almost $1 trillion pile of US bonds became a source of chatter after yesterday’s surge in Treasury yields.

- On the ground: Pelosi flew off after vowing the US wouldn’t abandon Taiwan as she met with President Tsai Ing-wen. She was expected to meet with TSMC’s chairman.

As a result, both S&P 500 and Nasdaq 100 futures rose by about 0.5%. In New York premarket trading, while Treasuries extended a slide sparked by hawkish Federal Reserve comments (and the lack of world war). The dollar fell against most G-10 peers, gold fluctuated and oil was lower ahead of an OPEC+ meeting where some report output may be boosted by a modest 100kb/d (or less jet-fuel than Biden consumed flying on Air Force One to Jedda last month) as Saudis “appease” the president.”

VIX futures consolidated, making a low of 23.13 and a high of 23.92. Yesterday’s high tested the mid-Cycle resistance at 24.91. It is commonly believes that the VIX may give a buy signal above 25.00. Max Pain in today’s op-ex is at 24.00 with calls going gamma long at 25.00. Shorts are thinning out.

DailyFX comments, ” When it comes to implied (expected) volatility measures, there is a certain revision-to-mean characteristic that is expected. If there isn’t a crisis-level event, it is likely that the VIX volatility index and its acolytes tend to deflate over time. While there has been meaningful retreat in the capital market benchmarks these past months, it is fair to say that there wasn’t much in the way of outright panic-like price action that would charge hedging costs to exceptional heights. That said, there is a point where the market can become too complacent in the face of tangible threats, and I do believe we had already passed that threshold. My assessing markets are ‘too quiet’ is one thing, for the financial system to come to the same conclusion usually takes an overt motivator to force balance. That recognition seemed to come with the headlines around a prominent US politicians visit to Taiwan, adding geopolitics to the threat of recessionary pressures and restrictive monetary policy that has dominated the fundamental scene of late. Just like the S&P 500’s slip, a check higher from the VIX and volatility of volatility index (VVIX) is best served with a clear charge for motivation rather than taking its traction on belief.”

TNX continues its rally that may last through options expiration. This may come as a surprise for those who had watched the decline for the past month. The odds are even that TNX may make a new high in the next three weeks. If so, the chances of an extension even higher may increase.

ZeroHedge reports, “In a time when the Fed’s QT is expected to soak up sloshing investor liquidity, while the end of Fed TSY buying (and phased out rolling of maturities) is meant to lead to a (gradual) increase in Treasury auction sizes, today’s quarterly refunding announcement by the Treasury was counterintuitive, because instead of boosting the size of auctions across the curve for August and futures months, the Treasury reduced its quarterly sale of longer-term debt for a fourth straight time (in line with expectations) and laid out plans for cuts to a range of maturities in coming months, with the 20-year bond – which has long been “kinked” on the curve and paying a higher yield than even 30Y paper – singled out for the biggest trimming.

The Treasury Department said in a statement in Washington that it will sell $98 billion of long-term securities at its so-called quarterly refunding auctions next week — down from May’s $103 billion. According to Bloomberg, this marks the longest string of declines in about eight years. The offering sizes are as follows:

- $42 billion of 3-year notes on Aug. 9, compared with $45 billion at the May refunding and $43 billion at the July auction

- $35 billion of 10-year notes on Aug. 10, compared with $36 billion last quarter

- $21 billion of 30-year bonds on Aug. 11, versus $22 billion in May”

The NYSE Hi-Lo made its Master Cycle high on July 29 on day 241, the earliest it can end its Master Cycle. I’ll be watching this indicator for two reasons. First, it may offer a sell signal below zero. And, second, should the Hi-Lo reverse quickly, there may be enough time to extend the Master Cycle low during the week of August 15. this offers another anomaly, since Monday’s high counts best as a Master Cycle for the SPX. Yet there is time to make a very deep low in time for options expiration. While it may not register as a Master Cycle in the SPX due to its proximity to the last Master Cycle, it may have the same magnitude as the crash in 2020, since these are both Intermediate-term declines.

USD futures made a new high at 106.40 as it gets another boost higher. Although the USD may have only a week to go in its Master Cycle, it may get a turbo boost into options week, due to the rush to liquidity.

Investing.com comments, “Emerging markets posted a fifth straight month of portfolio outflows in July, setting the longest such streak in records going back to 2005, as global recession risk, inflation and a strong dollar drew away cash, data from the Institute of International Finance (IIF) showed on Wednesday.

Non-residents pulled $9.8 billion out of emerging market portfolios in July, the data show, compared with an outflow of $3.8 billion in June and a $35.1 billion inflow in July 2021.

Net outflow over the past five months totaled $39.3 billion, according to the IIF.”