1:30 pm

GKX (Ag Index) is on day 256 of its current Master Cycle, suggesting an imminent reversal may be at hand. It has made a classic “running correction “where Wave C is higher than Wave A. We are so close to the reversal that an immediate long position may be made. Confirmation of the reversal comes at the trendline at 590.00.

ZeroHedge reports, “A food insecurity expert said the world has only about 10 weeks of wheat supplies left in storage amid the conflict in Ukraine and as India has moved to bar exports of wheat in recent weeks.

Sara Menker, the CEO of agriculture analytics firm Gro Intelligence, told the United Nations Security Council that the Russia–Ukraine war “simply added fuel to a fire that was long burning,” saying that it is not the primary cause of the wheat shortage. Ukraine and Russia both produce close to about a third of the world’s wheat.”

12:00 noon

SPX fell to 3875.00 this morning, then bounced. Thus far the bounce is under the 31.8% retracement at 3916.06 as I write. While the decline appears to be impulsive, it must decline again beneath 3875.00 to maintain the crash scenario. Most analysts are expecting a rip-your-face-off rally back to 4100.00 as this week is seasonally one of the more positive weeks of the year. A further decline to new lows is not expected and will cause the most pain among the unprepared. Should the rally continue above the 61.8% retracement level at 3941.20, the chances of a rally to 4100.00 are heightened.

ZeroHedge comments, “Following the cataclysmic drop in new home sales, notably weak PMIs, and ugly Richmond Fed data, reality is starting to bite this morning as ‘real’ economic data confirms the apparent collapse in ad-spend that Snap’s warning signals.

The reaction to all this was dramatic to say the least.

Stocks puked back all their gains from yesterday and then some, with Nasdaq and Small Caps now at Friday’s lows (before the late-day melt-up)…

7:50 am

I will be on a week-long hiatus from the markets and, hopefully getting a much-needed rest. I’ll be back in a week.

Good Morning!

NDX futures declined to 11762.30 after making a 50% retracement of the decline. All of yesterday’s gain has been lost as I write. In tomorrow’s expiring options, Max Pain is at 12060.00, with puts ruling the levels beneath that, intensifying beneath 12000.00. Short gamma begins at 11750.00. Calls ae scarce at nearly all levels.

ZeroHedge comments, “Equity liquidity is horrible

S&P 500 futures top-of-book depth now nearly matches the lows reached in 2008 and 2020

Source: Goldman

Liquidity generational lows

The picture in bonds mirrors the one in equities. Chart shows Top-of-book depth, 5-day average, $ mln.

SPX futures declined to a morning low of 3912.20, erasing all of yesterday’s gains. In today’s expiring options, Max Pain sits at 3955.00-3970.00. SPX options are now traded 5 days a week. Long gamma resides above 4000.00. Short gamma begins at 3925.00. Margin become a problem beneath 3900.00.

ZeroHedge reports, “It’s not every day that a relatively small social media company (whose market cap is now less than Twitter) slashing guidance can send shockwaves across global markets and wipe out over a trillion in market cap, yet SNAP’s shocking crash after it cut its own guidance released one month ago which hammered risk assets around the globe, and here we are. Add to this the delayed realization that Biden was just spouting his usual senile nonsense yesterday when he said Chinese trade tariffs would be discussed and, well, wave goodbye to the latest dead cat bounce as futures unwind much of Monday’s rally.

US futures declined as technology shares were set to come under pressure after Snap warned it would miss second-quarter profit and revenue forecasts amid deteriorating macroeconomic trends. Nasdaq 100 futures slid 1.5% at 7:30 a.m. ET and S&P 500 futures retreated 1.0% just as the benchmark was starting to pull back from the brink of a bear market amid fears the Federal Reserve’s tightening could hurt growth. Meanwhile in other markets, Chinese tech stocks fell by more than 4%, while Europe’s Stoxx 600 Index dropped 1%, led by losses in shares of utilities and retail companies. The dollar was little changed, while Treasuries advanced.

VIX futures are rising, but remains within yesterday’s trading range. In Wednesday’s expiring options Max Pain resides at 29.00. VIX appears to go into long gamma above 30.00.

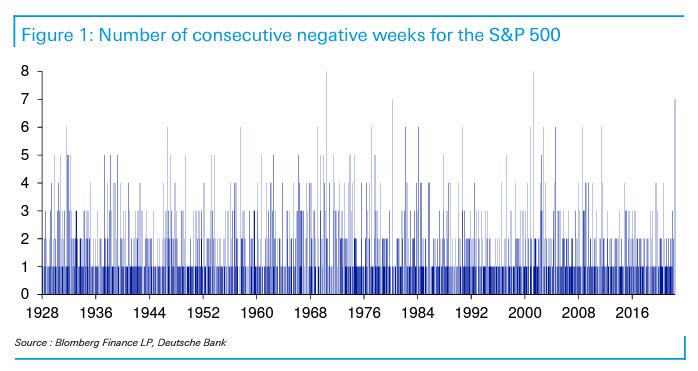

ZeroHedge reminds us, “The sheer relentlessness of the equity market sell-off continued apace last week with the Dow capping off its first run of 8 successive weekly declines since 1923. Meanwhile, the S&P 500 saw its first run of 7 successive weekly declines (tumbling 15.1% over this period) since the dotcom bust aftermath in 2001.

As DB’s Jim Reid notes in his Chart of the Day on Monday, there have only been three previous declines of 7 or more successive weeks. We had a 7-week losing stretch ending in March 1980 (total -15.8%) and two 8-week stretches ending in March 2001 (-16.9%) and May 1970 (-21.5%). We have never had a 9-week stretch of losses: will Biden take the the first ever credit for that? In any case, we are around record-breaking territory.”

TNX has declined beneath Intermediate-term support/resistance at 28.66. The Cycles Model suggests another week of decline, most likely to (or beneath) the 50-day Moving Average at 26.74.

USD futures continue to slide with a new overnight low of 101.75. The Cycles Model suggests a continued decline through mid-June. There may be a bounce at the lower trendline of the Broadening Wedge formation.