10:15 am

BKX ahs plunged beneath the Lip of the Cup with Handle formation and has entered a bear market with a 22% loss from the all-time high. Today is day 262 of the current Master Cycle. Should BKX not reverse here, this proxy of liquidity may show a serious strain on liquidity which may only get worse over the next 10 weeks.

ZeroHedge observes, “The second half of March came to an end and so did the meltup. Building on yesterday’s losses – as we detailed here – this morning’s breakdown has snapped all the major US equity markets below critical technical support levels.

The S&P is back below its 200DMA. The Dow and Russell 2000 are back below their 50DMA, and Nasdaq is rapidly accelerating down towards it 50DMA…

This comes as former NYFed President Bill Dudley issues another post-service op-ed warning that “If Stocks Don’t Fall, the Fed Needs to Force Them”…

It’s hard to know how much the U.S. Federal Reserve will need to do to get inflation under control. But one thing is certain: To be effective, it’ll have to inflict more losses on stock and bond investors than it has so far.”

9:59 am

The Ag Index is held beneath mid-Cycle resistance at 550.95 but may not remain there as Trending Strength is about to make a comeback. The Cycles Model suggest very strong upward momentum through the end of April, starting tomorrow. We may see ag prices double by the end of the year.

ZeroHedge reports, “America’s largest farmer cooperative sounded the alarm Wednesday about possible disruptions of fertilizer supplies from Russia due to Western sanctions on Moscow.

CHS Inc., the largest agricultural cooperative in the US, said in an SEC filing that it’s concerned about obtaining Russian fertilizer because of sanctions making it “more expensive and difficult to do business with Russia.”

CHS warned that sanctions could “cause delays with respect to, or prevent, shipments of fertilizer to us, cause inflationary pressures on and impact our ability to purchase fertilizer, disrupt the execution of banking transactions with certain Russian financial institutions and result in volatility in foreign exchange rates and interest rates, all of which could have a material adverse effect on our business and operations.”

8:15 am

Good Morning!

SPX futures have been consolidating inside yesterday’s trading range, with a midnight low of 4458.80 and a morning high of 4500.40. Having been repelled by the mid-Cycle resistance at 4503.91, it is now declining to test the 50-day Moving Average at 4418.38. Options expiration for tomorrow shows SPX in short gamma beneath 4500.00 with the heat turned up dramatically beneath 4450.00. The Cycles Model shows trending strength increasing on Friday which suggests a breakdown beneath supports. It also shows a probable six weeks of decline.

ZeroHedge reports, “U.S. index futures edged higher, along with European shares, after the sharpest two-day drop in almost a month, as investors digested Federal Reserve’s hawkish path and were jerked higher by a fleeting moment of Ukraine ceasefire hope when Emini futures initially spiked to session highs on the following Reuters headline:

- RUSSIAN FOREIGN MINISTER SAYS UKRAINE PRESENTED A NEW DRAFT AGREEMENT TO RUSSIA ON WEDNESDAY – IFX

… only to reverse the entire move two minutes later when the following headline hit:

- LAVROV: UKRAINE PROPOSALS ON CRIMEA, DONBAS UNACCEPTABLE: IFX

Mini hiccup aside, S&P futures were about 0.1% higher at 4,481 while Nasdaq futures gained 0.5% to 14,574, signaling an end to a selloff in the underlying index that erased $850 billion in market value over two days. Ten-year Treasury yields were flat around 2.61%, the dollar extended its rally to a sixth day, the longest streak in almost 10 months, and oil rebounded from yestereday’s IEA reserve release-driven plunge.”

VIX futures declined to a morning low of 21.54 and has bounced from mid-Cycle support. The Cycles Model shows trending strength increasing this weekend (Friday, perhaps?) and gaining momentum through the end of April.

The NYSE Hi-Lo Index fell to -200.00, confirming an equities sell signal.

SeekingAlpha explains, “Summary

- The VIX ETPs have quite a few quirks and as a result of these quirks and their high volatility, there are considerable risks for both longs and shorts.

- From the 30,000-foot perspective, the big risk in being short volatility is that a big one-day VIX spike can theoretically destroy the value of your entire position.

- While the number of VIX ETNs is dwindling, ETNs have their own set of issues, as these are debt securities – essentially a promise to pay the value of the underlying index – rather than a portfolio of VIX futures, as is the case with VIX ETFs.”

TNX continues making new highs this morning. Normally we may see a pullback to Cycle Top support at 22.96. However, TNX trending strength comes roaring back on Monday and continues through the end of the Master Cycle shortly after options expiration, suggesting a very short correction, if any.

ZeroHedge explains, “Everywhere we look we see short gamma – TLT edition

TLT is trading around the max short gamma pain level. Expect more erratic moves…

Source: Nomura

USD futures made a new overnight high at 99.85 before easing back. USD is in the final stage of its Master Cycle with a potential 5 days left. The potential target for this move may have a minimum of 101.00 and may go as high at 105.00.

Crude oil made a new low at 95.47 before bouncing to test the 50-day Moving Average at 98.83. The Cycles Model suggests increasing downward momentum through April options expiration. Wave C may equal Wave A near its trendline at 70.00. A panic decline may go to the Cycle Bottom at 55.17.

ZeroHedge reports, “Western oil majors have quit Russia altogether, taking billions of dollars in vague impairment charges on Russian energy assets, and now comes the hard math. This morning energy giant Shell Plc said that it will write off between $4 and $5 billion in assets in a first-quarter 2022 outlook.

Thursday’s announcement provides investors with an early glimpse at the costs of fracturing global supply chains for oil majors following Shell’s decision to exit Russia after the invasion of Ukraine.

“For the first quarter 2022 results, the post-tax impact from impairment of non-current assets and additional charges (e.g. write-downs of receivable, expected credit losses, and onerous contracts) relating to Russia activities are expected to be $4 to $5 billion,” Shell said.

“These charges are expected to be identified and therefore will not impact Adjusted Earnings,” it continued.

The charge surpasses the company’s earlier estimate of $3.4 billion worth of oil-producing assets in Russia.

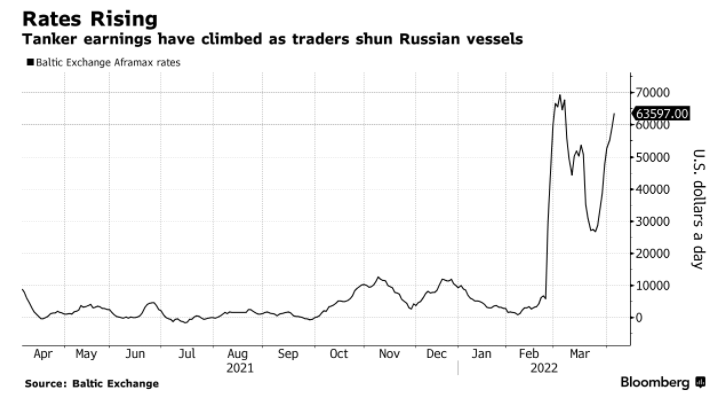

On a similar note, ZeroHedge observes, “Since Russia invaded Ukraine, many Western countries have banned Russian crude imports. Now, however, countries and companies are shunning the use of Russia’s massive fleet of oil tankers, which has driven up tanker rates, according to Bloomberg.

Shipping analyst Peder Nicolai Jarlsby at Oslo-based Fearnley Securities wrote that Sovcomflot PJSC, a state-controlled company with the largest Aframax-class fleet in the world, has been shunned by global oil traders. The result is fewer oil tankers available to haul crude, which has pushed up tanker rates.

Rising freight costs add to inflationary headwinds for the energy market that will only boost costs for refineries and, in return, continue to increase the costs for producing crude products, such as gasoline and diesel.