2:18 pm

The Ag Index is approaching what may be a massive Head & Shoulders neckline at 571.00. There is some argument that the neckline may be at the March high of 592.02, with a possible target closer to 950.00. Regardless of the location, this possible formation cannot be ignored.

ZeroHedge observes, “Infant formula is in short supply as US retailers begin rationing. A combination of COVID-19-related snarled supply chains and a major baby formula recall earlier this year exacerbated shortages.

At least 29% of the top-selling baby formula products were out of stock by mid-March, according to an analysis by Datasembly, which tracked baby formula stock at 11,000 retailers.

“This is a shocking number that you don’t see for other categories,” Ben Reich, CEO of Datasembly, told CBS News.

“We’ve been tracking it over time and it’s going up dramatically. We see this category is being affected by economic conditions more dramatically than others,” Reich added. “

ZeroHedge notes, “Ukraine is one of the world’s top exporters of corn, sunflower oil, and wheat. Disruptions stemming from Russia’s invasion of Ukraine have stoked fears the war-torn country could experience a 50% decline in crop output this year, according to Bloomberg.

Forecast data from ag expert UkrAgroConsult show Ukraine’s corn output could be as low as 19 million tons, about half of last year’s 41 million tons.

UkrAgroConsult’s pessimistic outlook follows huge production uncertainties as farmers experience shortages of diesel and fertilizer and bombed-out infrastructure. ”

2:03 pm

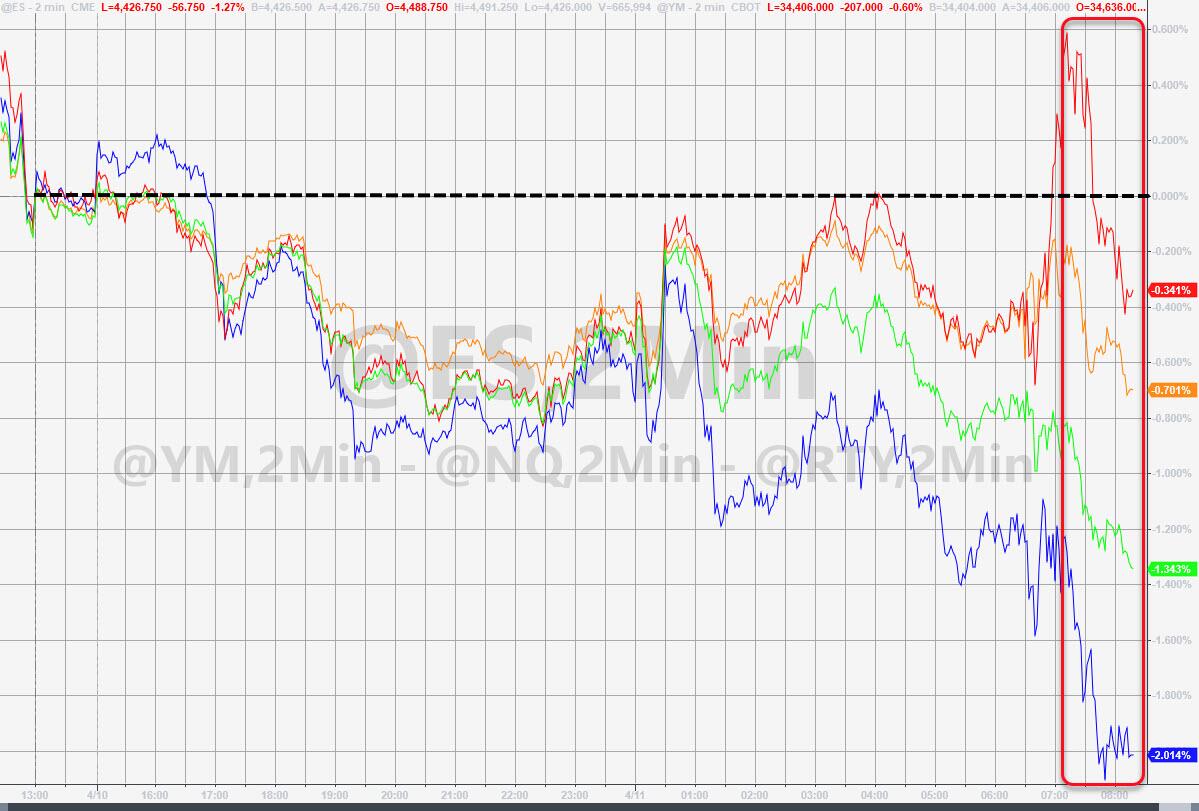

SPX is testing te 50-day Moving Average at 4425.25. It may bounce, but may not go far. On the other hand, should it fall through support, the decline intensifies dramatically.

ZeroHedge remarks, “The major US equity markets have all extended losses this morning, breaking below key technical support levels.

S&P broke below its 200DMA (and is testing towards its 50DMA). Dow failed at its 100DMA and is testing down to its 50DMA. Nasdaq and Russell 2000 broke below their 50DMAs…

…all tumbling as the yield curve steepens dramatically back up to pre-March-FOMC levels (reminder, it is the un-inversion that sets the clock ticking on recession, not the inversion itself)…

7:50 am

Good Morning!

NDX futures lead the way down this morning making new lows at 14154.80 and declining. It has declined beneath the 50-day Moving Average at 14334.34 and Intermediate-term support at 14219.45. Although there is some support at the Cycle Bottom at 13630.30, the true target is likely to be The Lip of the Cup with Handle at 13000.00. While NDX is in short gamma territory beneath 14350.00, short gamma intensifies at 14300 and every 50 points beneath it. Thus, NDX may have hit the trip wire for a panic decline this morning.

ZeroHedge observes, “Two weeks ago, Goldman’s head of hedge funds sales Tony Pasquariello unexpectedly took a contrarian position to the conventionally bullish house view, warning that over the next few weeks, “he called the market lower.” So far he has been spot on, and stocks indeed are now lower than they were at the end of March as the retail driven melt up that started in mid-March has once again collapsed.

So what happens next? Well, it depends on whom one listens to: Goldman or Goldman, because while the bank’s traditionally permabullish chief equity strategist (for common consumption) David Kostin continues to push the bank’s retail clients to buy whatever Goldman has to sell, and as we noted on Friday, Goldman has been selling a lot…

… Pasquariello still refuses to jump on the bullish bandwagon, and instead in his latest Markets and Macro note says that while he is not yet ready to fully subscribe to the recession narrative, he is very close and adds that when all is said and done, “bulls are fighting uphill.”

SPX futures have collapsed beneath the 200-day Moving Average at 4492.82 and are headed for the 50-day Moving Average at 4423.65. Today’s options expiration show a wall of (8573) puts at 4450.00. Should SPX close beneath that level, a self-reinforcing panic decline may ensue. To make matters worse, short gamma is deeply entrenched at that level for Thursday’s options expiration. Markets are closed on Good Friday.

ZeroHedge reports, “US futures slumped on Monday amid renewed concerns around surging bond yields, high inflation and rising Covid-19 cases in China. Contracts on the technology-heavy Nasdaq 100 were down 0.8% by 7:15 a.m. in New York, with S&P 500 futures slipping 0.4% and Dow futures fell 0.2% after the French election revealed an outcome largely as expected with Macron facing Le Pen in the second round in two weeks…

… and as 10Y yield soared as high as 2.78% overnight, up almost 10bps on the day and the highest since 2019, with US yields briefly rising above China’s 10Y for the first time since 2010, before reversing some of the move.”

VIX futures rallied to a morning high of 23.10 and appears to be rising. Trending Strength is especially strong today, suggesting VIX may make new highs. The answer to the question of why the VIX Master Cycle low was extended to day 279 may be explained below.

YahooFinance relays: (Bloomberg) — Ever since Barclays Plc halted sales and issuance of a popular stock-volatility product last month, it’s traded at a large premium to its underlying assets due to the sudden lack of supply.

But unexpectedly the exchange-traded note known as VXX has seen 20% of its shares redeemed since March 28 — instead of being sold in the open market at a higher price.”

TNX continues its advance with a triple measure of trending strength this week and extending to the Master Cycle high next week. The Cup with Handle target may be within reach in the next week or so.

Mises.org comments, “The Federal Reserve states that it “conducts the nation’s monetary policy to promote maximum employment, stable prices, and moderate long-term interest rates in the U.S. economy.” However, let’s look at how well the Fed has done that job since its founding in 1913.

Economy and Long-Term Interest Rates

Since 1913, the US unemployment rate has ranged from 2.5 percent in the early 1950s to 25.0 percent during the Great Depression. Inflation has ranged from positive 24 percent to negative 16 percent. Inflation is currently 7.9 percent, well above the Fed’s 2 percent target. While the Fed has some influence over money supply, they have no control over money demand or how money is spent, which has a significant impact on employment and inflation.

The Fed’s goal to “moderate long-term interest rates” below free market levels is a form of price fixing. Since price fixing never works for long, it is no wonder the Fed has been unsuccessful in this goal. Since 1913, ten-year Treasury rates have ranged from 0.5 percent in 2020 to 16 percent in 1981. Interest rates have been much more volatile than before the Fed, as shown below.

USD futures are consolidating inside Friday’s trading range as it enters what may be the final highs this week. Today is day 255 of the Master Cycle and USD did make 100.00 on Friday as suggested. The Cycles Model infers some trending strength by mid-week, but a reversal may be imminent at any time.

ZeroHedge observes, “The dollar reserve system is facing its greatest threat yet.

Russian Finance Minister Anatoly Siluanov said on Saturday that the five BRICS countries – Brazil, Russia, India, China and South Africa – could mitigate the backlash of Western sanctions against Russia on their economies by pooling their efforts and using a range of financial instruments at their disposal.

“The current crisis is man-made and BRICS countries have all the instruments necessary to mitigate its consequences for the national and global economies,” Siluanov was cited as saying by the Russian Finance Ministry.”

Crude oil futures made a new low at 92.95 this morning, extending the correction. Today is day 255 of the Master Cycle and the last day of trending strength (down). We may see a reversal by the end of the week, so stay on the alert. The highest probability is a final decline to mid-Cycle support at 81.65 before the reversal.