8:30 am

Good Morning!

SPX futures are challenging the mid-Cycle support at 4492.00 this morning, giving the first hint of a reversal. The mid-Cycle line offers an aggressive sell signal. Today’s expiring options are positive above 4475.00 and turn negative beneath 4435.00, so there is a very narrow range of neutrality that may be kept through today’s close. It does, however, indicate room for a decline. The 200-day Moving Average is at 4473.04 which, if crossed, may encourage short sellers.

ZeroHedge reports, “A torrid rally that pushed US stocks higher on 5 of the past 6 days appeared set to end, as US index futures drifted lower on Wednesday while bond markets stabilized from a historic rout driven by an increasingly hawkish tilt from the Federal Reserve took a breather after record losses. Contracts on the Nasdaq 100 were down 0.5% at 7:15 am in New York, while S&P 500 and Dow futures fell 0.4%; European bourses were also pressured sending the Euro Stoxx 50 -0.6%, with the exception of the FTSE 100 +0.4% amid crude action. Asia stocks closed higher, led by Nikkei 225’s 3% advance. The dollar rose to session highs amid hawkish Fed rhetoric and the USD/JPY continues to climb. Bonds bounce as risk wobbles and bulls pounce, but sellers remain prevalent; 10-year Treasury yield fell to about 2.37%, after hitting its highest since May 2019 on Tuesday and rising as high as 2.42% overnight.

After sliding to session lows, around 22.7 yesterday, the VIX has reversed the entire Tuesday move and was last seen just shy of 24.

VIX futures have risen to 24.00 this morning, short of the 50-day Moving Average at 26.74. The number where analysts sit up and take notice may be 25.00, so we may use that as an aggressive long entry. Of course, the Master Cycle low was on day 266, which suggests the risk of a further bearish extension is minimal.

NDX futures appear to be rapidly declining, having hit a morning low of 14523.00 and still dropping. The 50-day Moving Average is at 14444.47, where an aggressive sell signal lies.

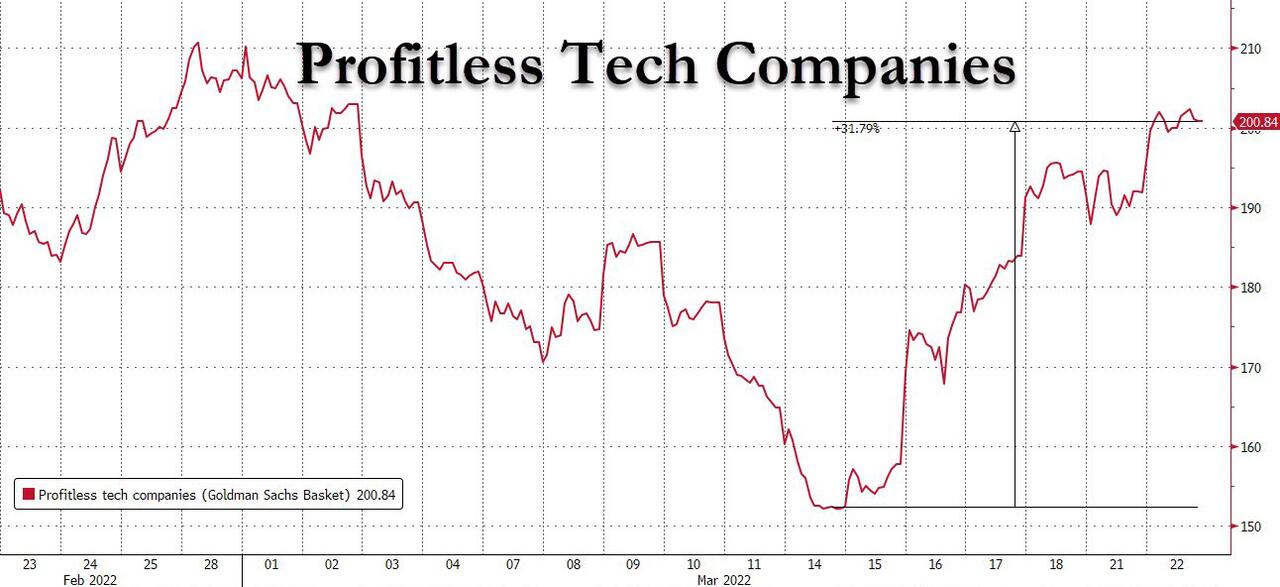

ZeroHedge exclaims, “Last week’s short-lived tech rally pushed some unprofitable tech stocks up nearly 50%. As remarkable as such a move is, strong temporary moves to the upside are nothing unusual in a market that is crashing. And “crash” is the best description of what some areas of the technology sector are going through.

Tech stocks, as measured by NASDAQ, peaked on November 19, 2021. However, if we look at the subset of unprofitable growth stocks, former unicorns that have seen tremendous growth in their stock prices in recent years or former SPACs, then the peak in many of these stocks occurred a few months earlier shortly after the meme stock mania. Chinese tech stocks, in turn, peaked in late 2020 as the Chinese government clampdown on tech companies began.”

The rally in TNX is taking a pause, as anticipated by the EW structure. The Cycles Model suggests a correction may be underway for the next two weeks. A pullback to the Cycle Top support at 20.98 is possible.

ZeroHedge remarks, “US 10 year – the long term view

The US 10 year yield is approaching huge levels. This needs to pause, or…

Source: Refinitiv

US 10 year – the perfect trend channel

Us 10 year continues trading inside the big (and perfect) trend channel. Rising yields has become very consensus lately…

USD futures have risen back above the Cycle To support/resistance at 98.53 this morning. Today is day 259 of the old Master Cycle, which may be modified to show a top near 100.00, should it rally into the end of the week.

WTI futures have rallied to an overnight high of 113.88. however, I have been warning since Monday that it is at its Master Cycle end. Today is day 260. Should the reversal occur today, there may be three weeks of decline. The mid-Cycle support is the normal target. However, should a liquidity crisis occur, the decline may test the bottom of the Broadening Wedge formation or possibly the Cycle bottom at 56.26, near the 61.8% retracement point.

ZeroHedge warns, “While the world has been obsessively focused on crude oil and gasoline in recent weeks, we instead alerted readers to a far more dire scenario playing out in diesel, a source of energy which is absolutely critical in keeping the “just in time” world running on time.

As a reminder, here are some of the articles we have published on the topic in recent weeks, many even before the Ukraine war:

- Diesel Is The U.S. Economy’s Inflation Canary – Feb 8

- U.S. Diesel Stocks Set To Fall Critically Low – Feb 18

- China Asks State-Owned Refiners To Halt Gasoline, Diesel Exports – Mar 10

- Global Diesel Shortage Raises Risk Of Even Greater Oil Price Spike – Mar 12

Fast-forward to today, when our warning was echoed by the heads of one of the largest commodity trading houses and the biggest independent oil trader who were speaking at the FT Commodities Global Summit in Lausanne, Switzerland on Tuesday.”