9:05 am

It’s been a couple of weeks since I last reported on the GSCI Ag Index and it is due for an update. It now appears that GKX may stretch its correction at least through options expiration next week and possibly through mid-August as well. It is currently resting on a Head & Shoulder neckline at 384.00 and may break down in response to liquidity flight from the markets. While the consequences in the Ag Index may not be as dire as in the stock indexes, it would pay to know the “lay of the land.”

A standard 61.8% retracement would decline to 336.80, which falls inside the Cycle boundaries. However, this decline may be much stronger, so be warned.

We are already seeing food inflation at the retail shelves, called shrinkflation. I have noticed at Kroger that they have stacks of the old, larger cereal boxes at the end of the aisles on sale while the new, smaller cereal boxes are on the shelves at a shrinkage of more than 10%. Most shoppers won’t notice the difference.

ZeroHedge reports, “World food prices fell in June for the first in 12 months, offering some relief for consumers and easing inflationary pressures.

According to a new Food and Agriculture Organization of the United Nations (FAO) report, the FAO Food Price Index, which measures monthly changes for a basket of cereals, oilseeds, dairy products, meat, and sugar, dropped 2.5% in June, coming off a decade high, but still 33.9% higher than its level in the same month last year. The decline in the index was the first in 12 months.”

However, even higher prices due to supply and demand may be just around the corner. ZeroHedge notes, “Kirk Hinz, a meteorologist with BAMWX, published an agriculture note Thursday which outlines “persisting rains” in some parts of the Southwest but “expanding dryness” in the north.

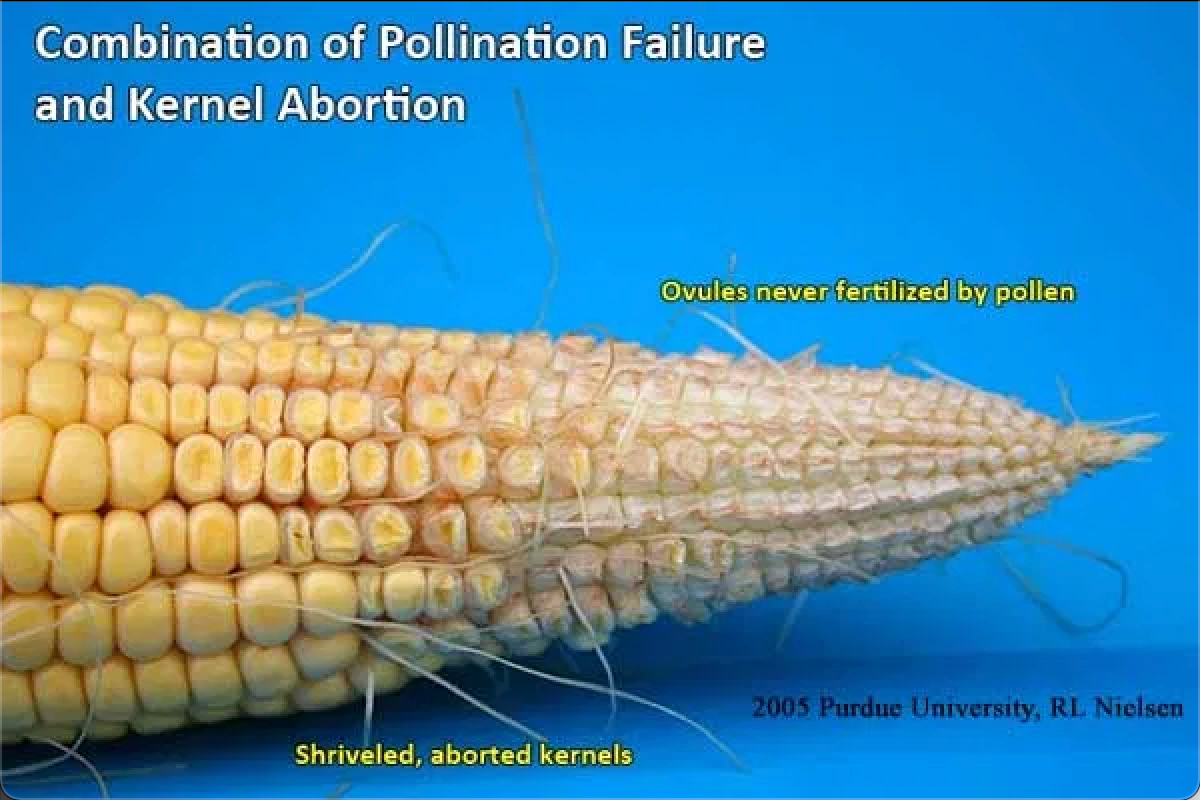

Hinz concentrates on the corn belt, which spans the Midwest. He said, “expanding drought into a crucial time of the year ahead of pollination.” This means that persistent dry conditions could affect pollination success – and if pollination is not successful this year because of drought and lack of water, then harvest yields this season could come under pressure.

“A lack of consistent rainfall across a big chunk of the US major corn production areas in the Midwest and northern Plains this year continues, with the expanding drought into a crucial time of the year ahead of pollination as well. Weather models have remained volatile recently in regards to how much of these major production areas will receive timely rainfall, but the trend recently has been to push previously forecast widespread nourishing rains further south that’s starting to be a growing concern (plus more heat building back in a mid-to-late month) ahead,” Hinz wrote.

Here’s what happens to corn if pollination is unsuccessful. “

7:10 am

The Shanghai Composite Index made a new low this morning, setting off the Head & Shoulders formation (upper right). This may be a short-term formation, but with long-term consequences. It appears that it may also trigger the Cup with Handle formation while meeting the Head & shoulders target.

Chinese officials at the PBOC may be aware of the implications of this formation. However, no amount of money can reverse a loss of confidence.

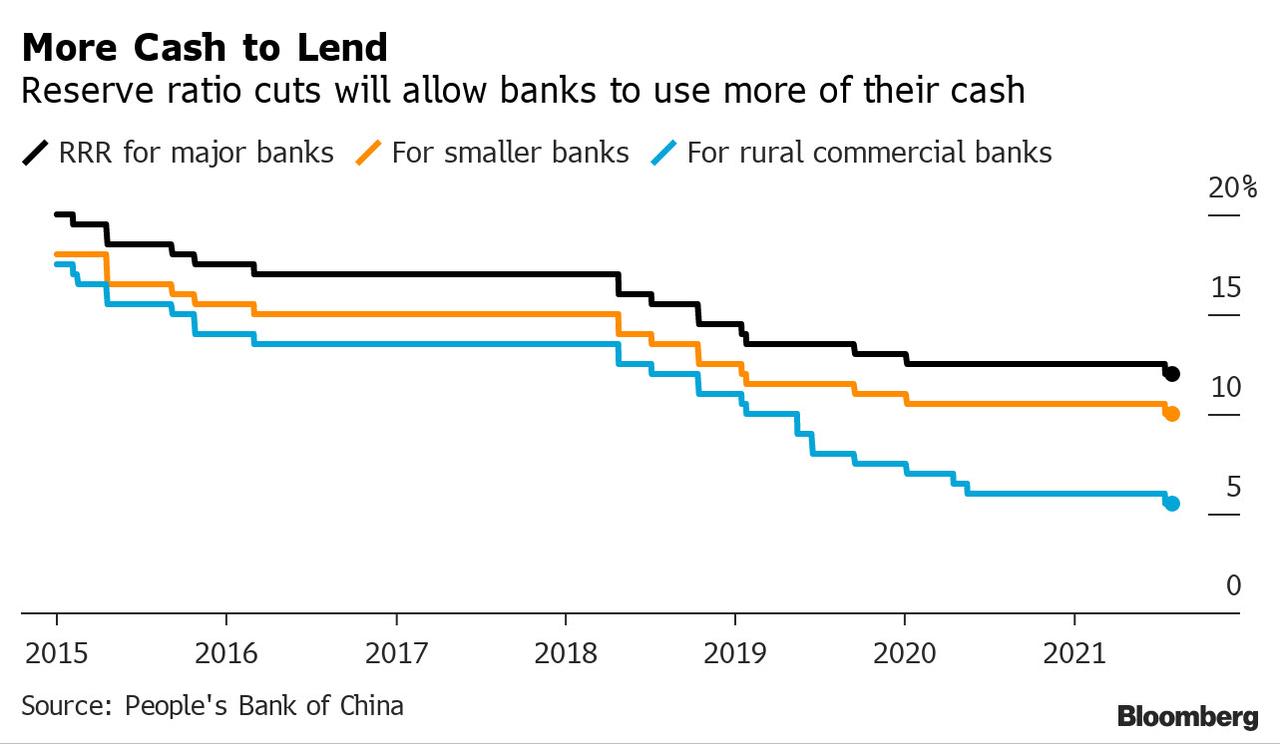

ZeroHedge reports, “Just two days after we said that “China Prepares To Cut Rates As Economy Stalls“, this morning China did just that when the PBOC announced it is cutting the Required Reserve Ratio by 0.5% for most banks, a move that will unleash about 1 trillion yuan ($154BN) of long-term liquidity into the economy and will be effective July 15.

The announcement reduces the amount of cash most banks must hold in reserve in order to boost lending to the economy as growth has sharply waned, and is expected to prop up China’s slowing economy, which as noted earlier this week saw its Caixin Service PMI drop to the lowest level since the covid crisis, badly missing expectations.

Liquidity may be boosted in China but it may be tightening here in the U.S., the largest market. The BKX (proxy for liquidity) tested its Head & Shoulders neckline at 118.70 yesterday and bounced to 121.11, but closed only 104 ticks from triggering the formation. Should it slip through at anytime today, the liquidity plug may be pulled for it and the stock market. Next Wednesday may be the Master Cycle low for the BKX with 4 out of 6 momentum indicators at full strength next week. The average Master Cycle low only needs 1-2 momentum indicators at strength. This may be a doozy.

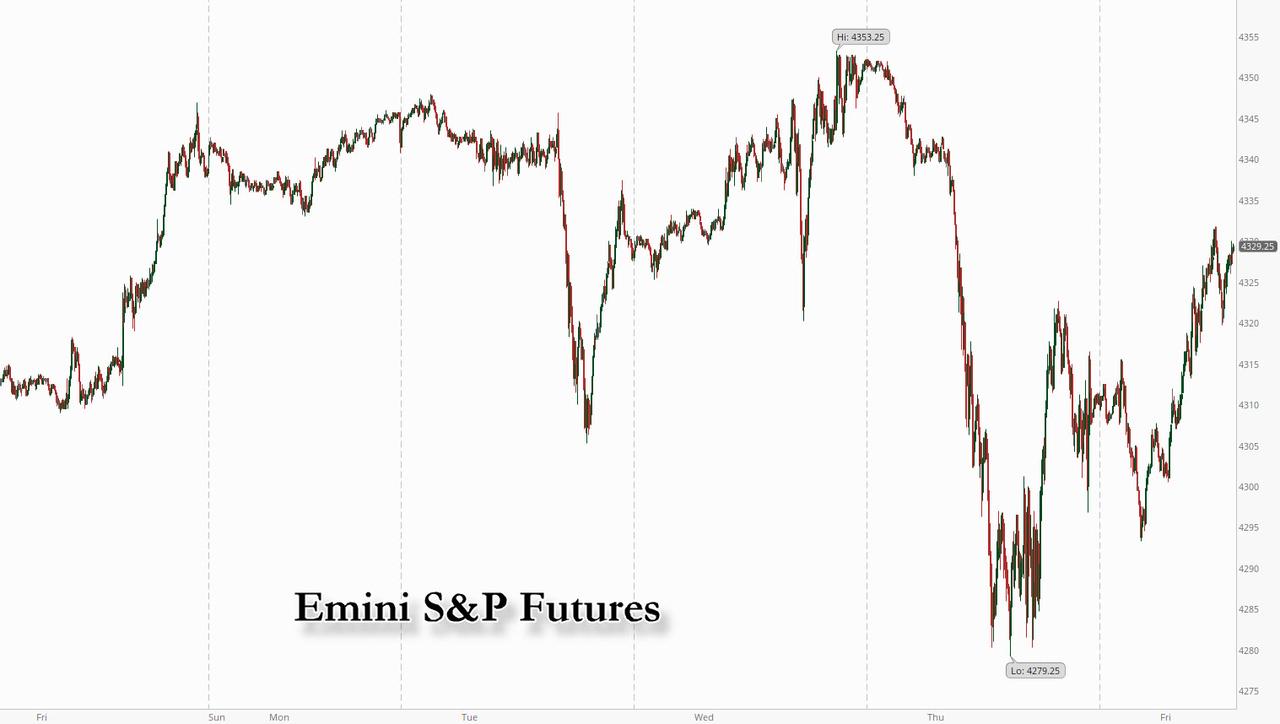

SPX futures ventured higher in the overnight market to 4336.88 early this morning after yesterday’s rout. Dealer gamma is net positive, so it makes sense to keep the market in line for options expiration. The net open interest in calls is positive from 4300.00 and up, with the largest number of net call contracts at 4325.00 (4269, to be exact). Dealers walk a fine line to keep payouts on either side at a minimum, so pressure is on to close near 4300.00.

ZeroHedge reports, “After a mini-rout on Thursday which briefly pushed the S&P into negative-gamma territory below 4,300, European stocks and US equity futures rebounded on Friday as energy and banking shares rose from a sharp selloff that was triggered by growth worries and has put the indexes on track for their biggest weekly fall since mid-June. At 7:30 a.m. ET, Dow e-minis were up 216points, or 0.61%, S&P 500 e-minis were up 18.5 points, or 0.43%. Nasdaq e-minis were down 3.75 points, or 0.02% after a report that Joe Biden is taking aim at big tech by encouraging regulators to reinstate net-neutrality rules. The dollar weakened against a basket of major currencies.”

VIX futures declined beneath the 50-day Moving Average to 17.16 this morning and may be completing a corrective move. Every effort is being made to “steer” the market and the VIX applies the most leverage with the least outlay. However, should the SPX close beneath 4300.00, the VIX may explode higher.

TNX futures rose to an overnight high of 13.48, opening the cash market at 13.38. The new Master Cycle has nearly a month to go with its target near 19.71. The short-term target is the 50-day Moving Average at 15.45.

ZeroHedge remarks, “While stocks have been a (mostly) one-way ticket higher, 2021 has been a rollercoaster for interest rates: after 10 year yields rose +83bps in Q1, they fell -27bps in Q2 and have started Q3 by already falling another -12bps.

So yesterday, when commenting on the latest violent move in yields lower which left a majority of rates traders (who have been blindsided by the move) dazed and confused, we quoted JPM’s rates strategist Jay Berry who said that “the 10+bps decline in 10-year yields since Friday morning seems outsized all considered” and added that 10-year Treasury yields was 25bps too low relative to model-implied fair value, a 3-standard deviation divergence, and the largest such deviation since the early fall 2020.”

USD futures appear to be consolidating in a narrow range. There appears to be a 2-week correction just ahead. The probable target may be the 50-day Moving Average at 90.88, a near-50% retracement.