2:59 pm

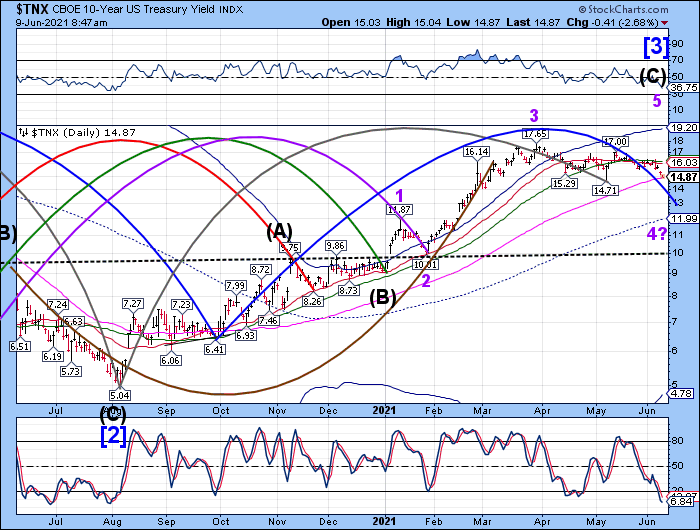

TNX swept past the 100-day Moving Average at 14.87, then bounced back for a retest. There may be another probe lower before the retracement is over. Today’s 10-year Treasury auction benefitted from this move. How will those buyers feel when the yield goes to 2.00%?

ZeroHedge reports, “Having seen yields in the secondary market plunge to 3-month lows during the morning, Treasuries were sold ahead of the $38 billion reopening 10-year sale (backup to a When Issued yield of 1.507% – from 1.4705% intraday lows). The Fed may have had a direct hand in lowering prices because they do not need pressure to raise rates in their repo facility…an accident waiting to happen?

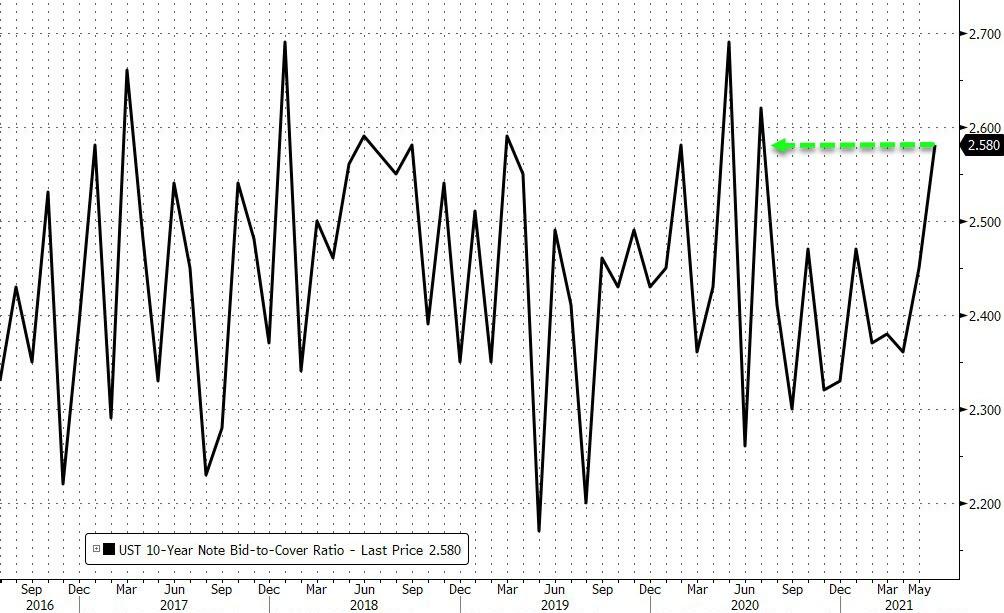

Demand was stellar with the bid-to-cover (2.58x) surging to its highest since July 2020…

Source: Bloomberg

Today’s high yield was 1.497% (almost 20bps below the 1.684% at the last auction), trading through the WI yield by a very significant 1bps”

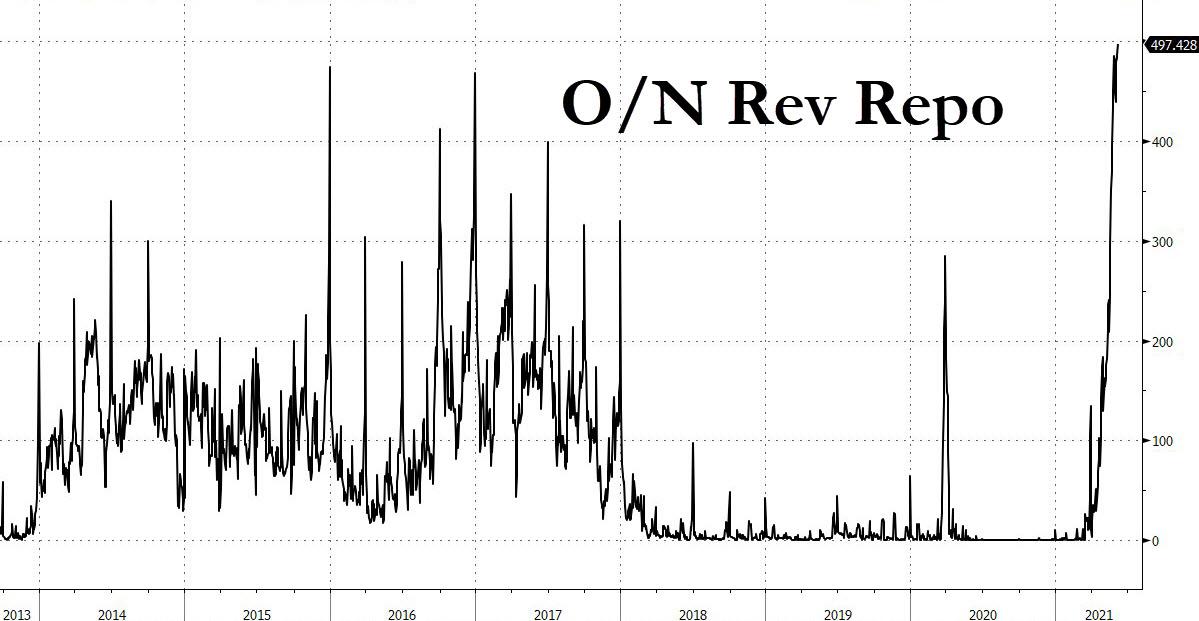

Zerohede further reports, “With usage of the Fed’s overnight reverse repo facility again hitting a new record high on Tuesday, rising to an all-time high of $497.4 billion…

… rates traders are trying to decide if the Fed will tweak the rate on either the IOER (Interest on Excess Reserves) or the Reverse Repo Facility, collectively the Fed’s “administered rates” in order to ease the liquidity congestion that has parked half a trillion dollars at the Fed where it is sitting inert, doing nothing.

One strategist who believes there is a “small chance” the Fed will adjust its IOER/RRP rate is Deutsche Bank’s Steven Zeng, who also cited concern about the quarter-end balance sheet squeeze, which is less than the futures market is currently pricing.”

10:15 am

This is very interesting. The Cycle from the March 7 high to this morning’s high is exactly 21.5 market days , top-to-top, completing the daily Cycle. Should this be the last of the retracement, this morning’s high also pinpoints the potential Master Cycle low (Wave 3 or (3) of Wave [1]) on June 25 in what may be a 12.9-market-day scorching decline.

Another surprise is that the NDX failed to make a new retracement high this morning after a 30-market-day Cycle completed. Something is brewing…

7:20 am

Good Morning!

NDX futures are consolidating beneath yesterday’s high, within a range of 13804.38 to 13860.38. It appears to be in an irregular correction that may require yet another probe higher. A decline beneath the 50-day Moving Average at 13568.88 would negate that move higher. However, NDX has yet another potential period of strength on Friday that may not be shared with the SPX. That strikingly corresponds with a potential period of weakness in the TNX, which ends over the weekend.

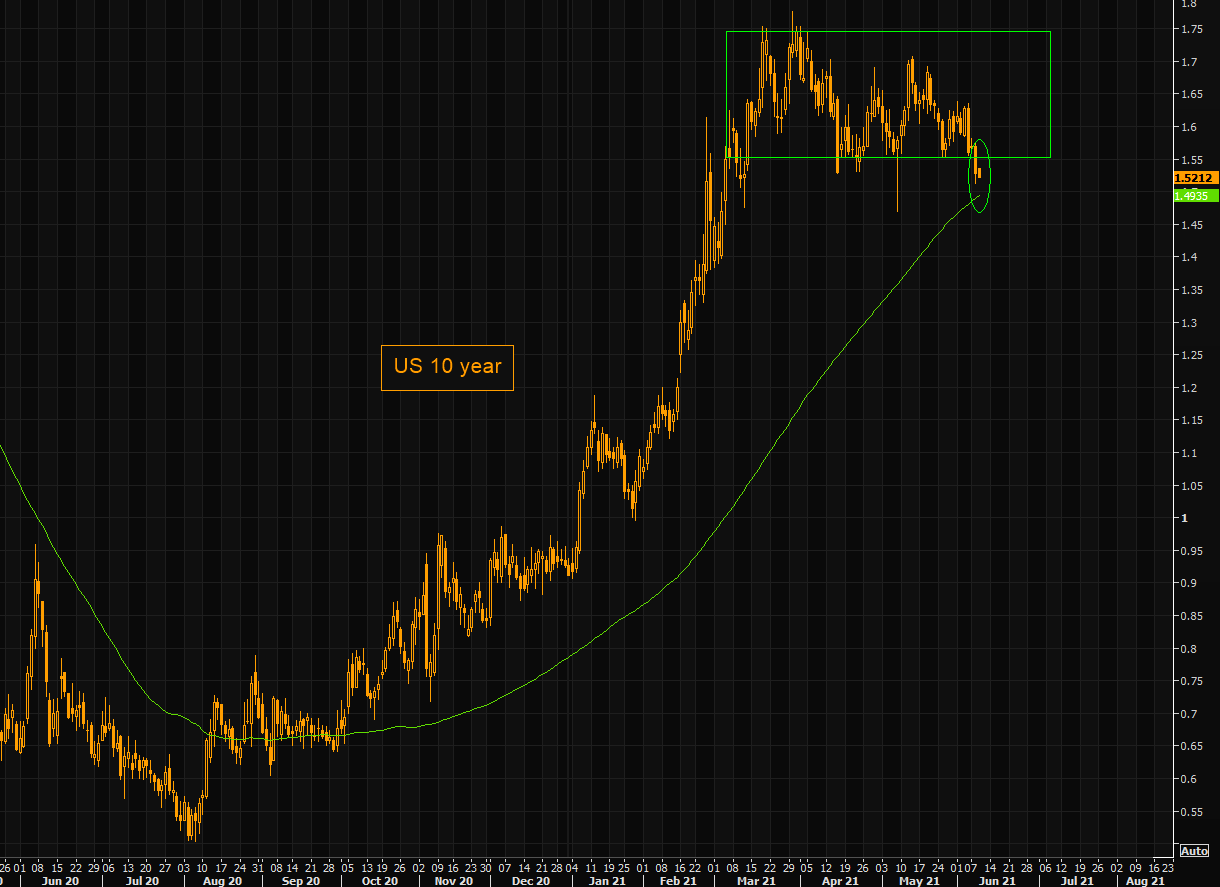

ZeroHedge observes, “Several assets are working on the range break out, although in slow motion. US 10 year at 1.51% is a new “thing”. We have not seen yields close here or lower since early March. Note the 100 day slightly lower at the big 1.5% level.

Source; Refinitiv

With yields down, the obvious question is whether or not NASDAQ will start to catch more solid bids. Note the most recent short term divergence between yields and NASDAQ.”

The Shanghai Composite appears to be due for a Master Cycle high early next week as well, which also corresponds closely with a possible high in the NDX and a potential low in the TNX. Should it go higher, the target appears to be the Cycle Top resistance at 3655.15.

ZeroHedge reports, “Update 10:00pm ET: moments after reporting a red hot PPI which was the highest since Lehman, China effectively launched price controls, with China’s economic planning agency vowing to increase supply of key consumer goods to stabilize prices, according to a statement on NDRC website on a national video meeting Tuesday.

- *CHINA VOWS TO CONTROL CORN, WHEAT, PORK PRICES AFTER PPI SURGE

- *CHINA TO KEEP PRICES OF GOODS LINKED TO LIVELIHOOD STABLE: NDRC”

SPX futures are consolidating in a narrow range between 4222.62 and 4232.12. The correction of the May 12 decline appears to be complete. This Friday’s open interest in the options market shows net puts outpace calls at 4200.00 by 2800 contracts, while calls outpace puts at 4225.00 (by 2700 net calls) to 4250.00 with over 10,000 net call contracts. Max pain lies in the 4200.00 to 4225.00 range. All of this is in a period of strength that ends on the weekend.

ZeroHedge reports, “S&P futures traded in a narrow 8 point range near all-time highs as a lack of clear catalysts kept trading slow, with investors awaiting fresh cues from inflation data this week and an upcoming Federal Reserve meeting. 10Y TSY yields dropped below 1.50% for the first time since May 7 amid a plunge in odds that Biden’s reflationary infrastructure program will pass, and easing fears that tomorrow’s CPI print will smook markets. At 07:15 a.m. ET, S&P 500 E-minis were up 3.25 points, or 0.08%, Dow E-minis were down 37 points, or 0.1%, while Nasdaq 100 E-minis were up 40 points, or 0.29%. The dollar dropped against all of its G10 peers.

On Tuesday, U.S. stocks closed within a hair’s breadth of a record high and Treasuries rose as investors debated the impact of resurgent inflation on monetary policy. “Investors are likely to be in a wait-and-see mode,” said Mitsushige Akino, a senior executive officer at Ichiyoshi Asset Management. “People will want to check how market expectations over the Fed’s policies change and how yields, whose upside has been capped recently, move following the U.S. CPI data.”

VIX futures appear to be consolidating in a range from 16.04 to 17.37. VIX options expiring today have a Max Pain range from 16.00 (puts prevail) to 20.00 (calls prevail), It is likely that the VIX may remain range-bound today. Next Wednesday’s VIX options show the puts have it over the calls by over a million contracts spread between 15.00 and 22.00. This is begging for an accident to happen. At the very least, it suggests that at next week’s expiration on the VIX is likely to be near 22.00 or possibly higher, since the number of net calls is miniscule.

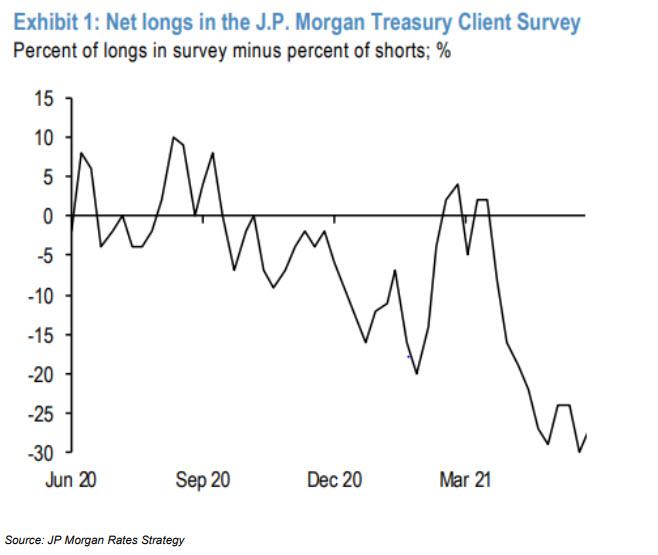

TNX made a morning low testing the 100-day Moving Average at 14.87 on day 253 of the Master Cycle. Monday is day 258, which is likely to end the decline. The only obvious target is the mid-Cycle support at 11.99. However, treasury shorts are all in, so the risk of a short squeeze grows exponentially.

ZeroHedge comments, “With the recent JPMorgan Treasury Client Survey showing that self-reported Treasury net longs were at record lows (and by extension, shorts were all time high) understandably perhaps ahead of an inflation print that is expected to be among the highest on record, there were virtually no traders left to short Treasurys, with all bears already on board.

This meant that as a result of a massive position imbalance, the risk was for a raging short squeeze on even a whiff of deflationary news, and that’s precisely what we have seen in recent days, starting with last Friday’s disappointing payrolls report which sent 10Y yields lower by 8 bps, and continued with the collapsing odds that a Biden infrastructure plan will pass, amid a breakdown in GOP talks and opposition by centrists such as Manchin.

USD futures tested yesterday’s low at 89.84 in the morning session. This is near the 61.8% Fib retracement level. That may be the extent of the correction, since the Cycles Model shows a double dose of strength by Friday.