The Lord’s Prayer

Our Father, who art in heaven, hallowed be thy name. Thy Kingdom come, Thy Will be done, on earth as it is in heaven. Give us this day our daily bread and forgive us our trespasses, as we forgive those who trespass against us. And lead us not into temptation, but deliver us from evil. Amen

8:00 am

Good Morning!

SPX futures continued their descent to 6595.20 thus far after closing deep in short gamma beneath 6700.00. The Head & Shoulders formation has been activated and may follow through to its target in the next several days. The implications of short gamma are that the the dealers have stopped taking the opposite side of the bearish transactions (puts) and have added shorts as well. In this case, the tail (options) is (are) wagging the dog. Fuel shocks are adding to the malaise.

Today’s options chain is beyond Max Pain at 6700.00. There is a small put wall at 6600.00 that may be taken out. Should the SPX go lower, 6600.00 may act as resistance to a bounce. Another put wall lies at 6550.00 which may incite a bounce. The largest put wall is at 6400.00, near the Head & Shoulders target.

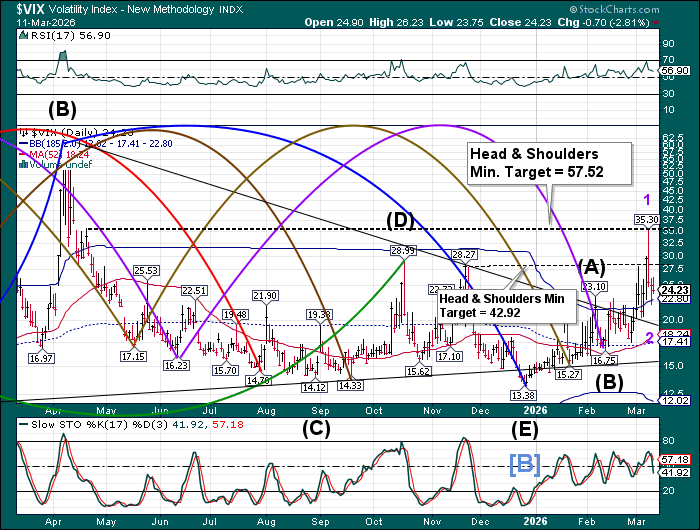

The premarket VIX rose to 26.62 thus far this morning. VIX may rise to challenge the neckline of the Head & Shoulders at 35.30. Should that occur in the next day or two, the upper target may be in play.

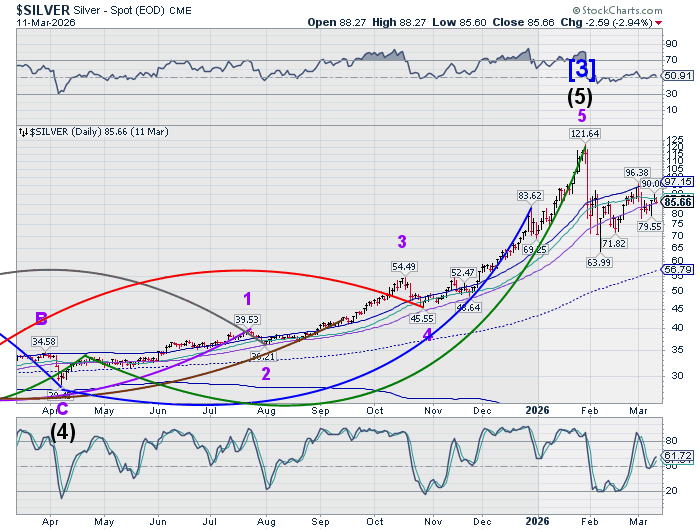

The March 25 options chain shows Max Pain at 20.00 with a call wall at 24.00 giving support to the current rally. The next call wall is at 30.00 with a strong likelihood of reaching it in the next day or two.

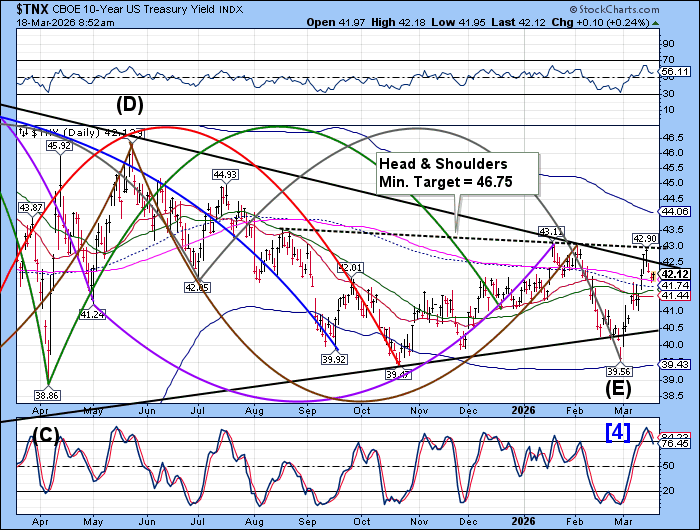

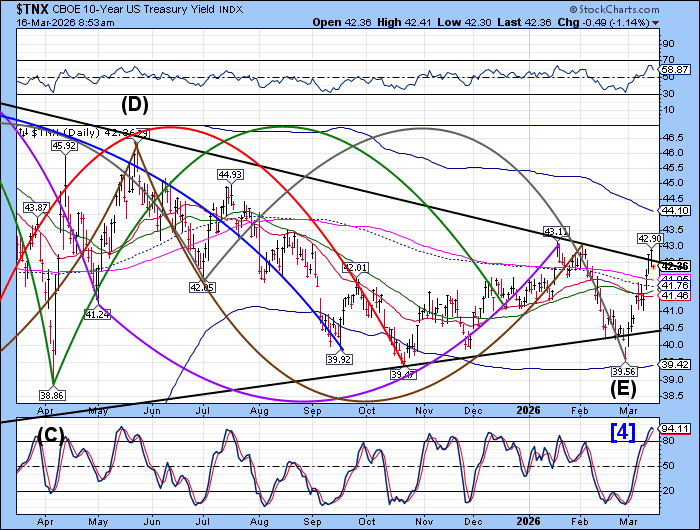

The US 10-year Bond Yield has gapped above the neckline of the head & Shoulders formation, The immediate goal may be to reach the Cycle Top at 44.07 before retesting the neckline. The loss of the oil infrastructure has been very inflationary.

USD is poised beneath its Cycle Top at 100.22 and the Head & Shoulders neckline at 100.55. The Cycles Model appears non-directional for another week, then the dollar may be energized towards the end of march and continue higher to mid-April.

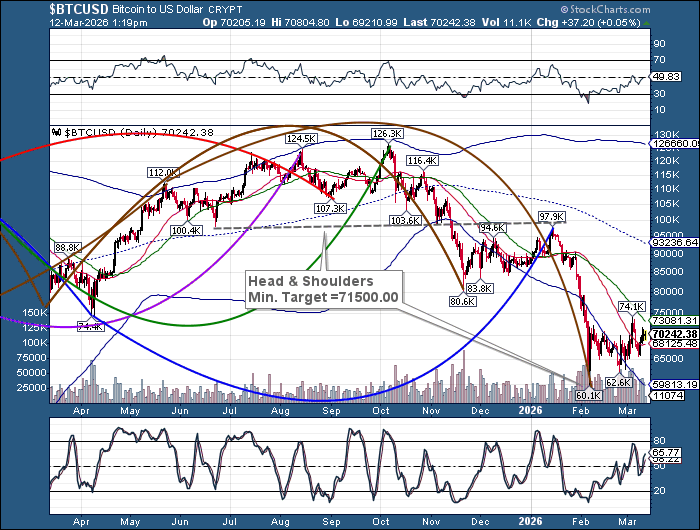

Bitcoin is testing the 52=day Moving Average at 68835.00 this morning. Should it break down, a sell signal may be given. Currently, the downside may offer support at round numbers (60000.00, 50000.00 and 40000.00). Each level may be given consideration for limiting or continuation of the decline.

Crude oil is stalling at the mid-range of yesterday’s levels. The Cycles Model suggests a neutral-to-lower stance for the next couple of weeks.

Gold declined to 4505.31 today and may be ready for a bounce. The possible target for the decline may be near 4400.00 over the next three weeks. The 52-day Moving Average at 4937.00 may act as overhead resistance to the bounce.