2:26 pm

Try as it might, BKX is having trouble making a normal retracement (79.77). There are just a couple hours left. The Cycles Model suggests all hell may break loose over the weekend. Brace yourselves.

11:00 am

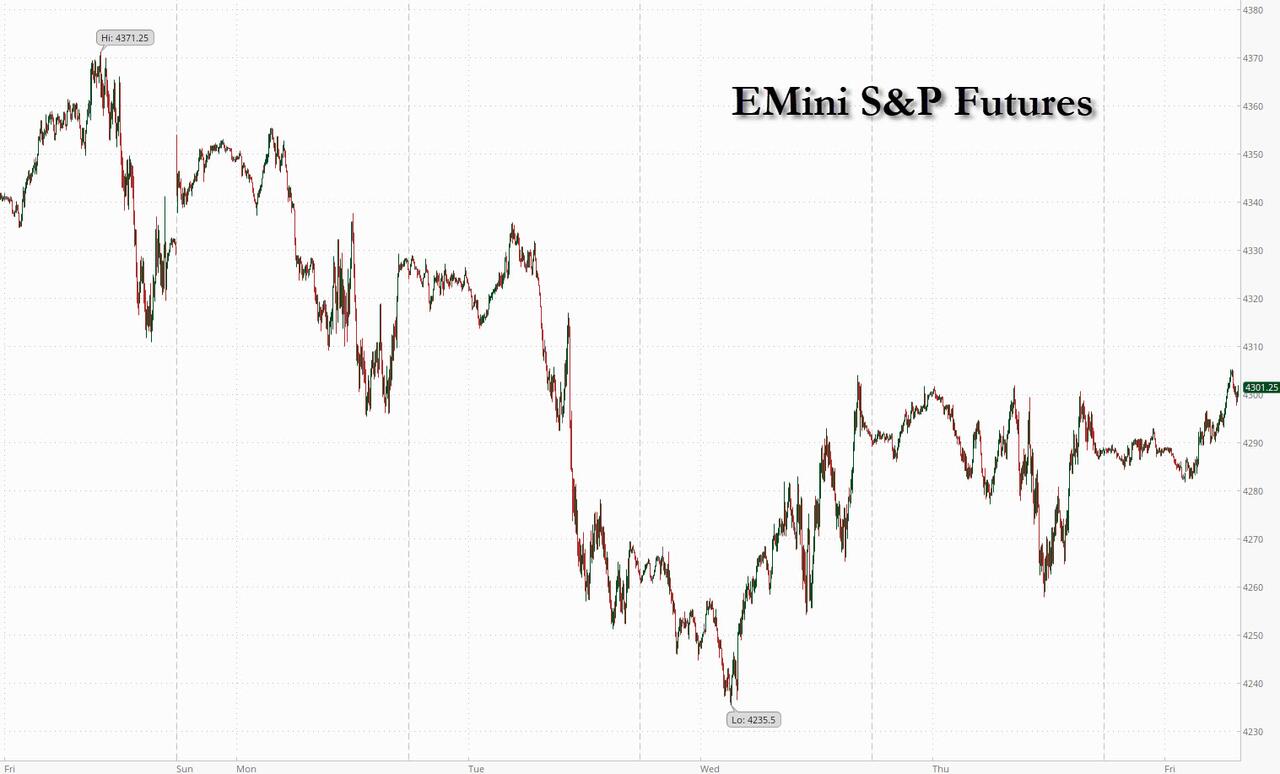

It is fascinating that the SPX sold off to the trading Cycle bottom at 4219.53, then rallied back up to a near round trip. As indicated in the Cycles Model, the collapse may start in the next hour or two…

ZeroHedge observes, “Risk sentiment has been hit lately and while investors can find some green shoots of market stabilization in the past few days, it would be brave to call a bottom just yet.

Markets have been served a toxic cocktail of higher real and nominal yields, a strengthening US dollar and rising oil prices in combination with automated selling and forced de-risking of portfolios. This big multi-asset wave came at the wrong time for a stock market left vulnerable by summer weakness and low liquidity.

“What’s scary is that thematically, we are seeing cross-asset markets voting with their feet and lending credibility to the idea that the recent shock tightening move in US financial conditions is indeed going to accelerate hard landing risk,” notes Nomura strategist Charlie McElligott.”

7:55 am

Good Morning!

NDX futures are pressing at yesterday’s high at 14786.69. Its intended target may be the 100-day Moving Average at 14949.25. The Cycles Model suggests that time for this rally may be running out by mid-day, regardless whether it makes its intended target or not. Don’t let the gradual glide path thus far fool you. There is a potential for 2-3 limit down days in the next 2-3 weeks.

Today’s op-ex shows Maximum Investor Pain at 14720.00. Long gamma starts at 14750.00, while short gamma begins at 14700.00. There’s not a lot of room for error.

ZeroHedge remarks, “Investors are anticipating the Federal Reserve is close to the end of its tightening cycle.

Every surge in bond yields spurs fresh speculation the economy will break badly enough for policy makers to pivot rapidly away from their hawkish stance. That may set up bonds and stocks for a tough time even if Friday’s payrolls report comes in on the soft side.

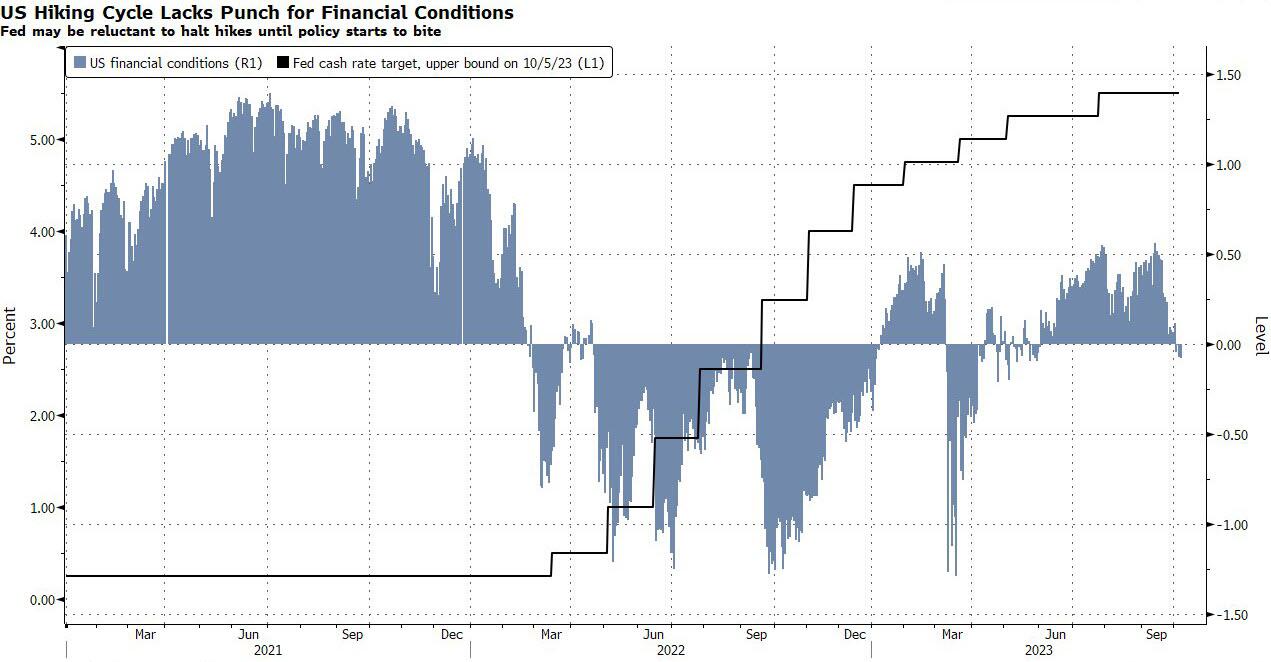

That’s because even the recent rout in Treasuries only managed to push US financial conditions to a neutral level, based on a Bloomberg gauge, well short of the sort of restrictive impact the Fed would seem to be wanting to achieve. That also helps explain the still-resilient state of the economy — Bloomberg’s US data surprise index remains at elevated levels.”

SPX futures made a new retracement high at 272.20 as it probe toward the Head & Shoulders neckline. The Cycles Model suggests the uptick may be over by noon today. Be prepared for a possible waterfall event, with multiple “limit down” days due to surges in trending strength over the next 2-3 weeks.

Today’s op-ex shows Max Pain at 4255.00. Long gamma starts at 4270.00 while short gamma erupts at 4250.00 and remains strong to 4050.00. The market is on a tightrope with no nets.

ZeroHedge reports, “Global stocks and US index futures gained ahead of the September payrolls report (exp. payrolls 170K, unemp 3.7%, full preview here) that could potentially ease pressure on the Federal Reserve to raise interest rates again. At 7:45am ET, S&P futures rose 0.1%, after falling by a similar amount on Thursday while the tech-heavy Nasdaq 100 rose 0.2%, after slipping 0.4% the day before. Shares climbed in Asia and Europe, while mainland Chinese markets remain shut for a weeklong holiday. Treasury yields extended their advance, with the 10-year hovering around 4.74% after reaching 4.88% earlier this week. The Bloomberg dollar index was little changed. Oil was also little changed, halting its decline this week. All eyes on today’s NFP release at 8.30am, which is the near-term focus to set narrative: consensus expects NFP to print 170k and the unemployment rate to print 3.7%.”

VIX futures are consolidating this morning, poised to go in either direction. A normal retracement may take the VIX down to 16.50, but the mid-Cycle support at 17.27 may hold, instead. Expect to see a shock to the markets either today or early next week.

Next Wednesday’s op-ex shows Maximum Investor Pain at 18.00. Short gamma is in short supply while long gamma reaches from 19.00 to 42.50.

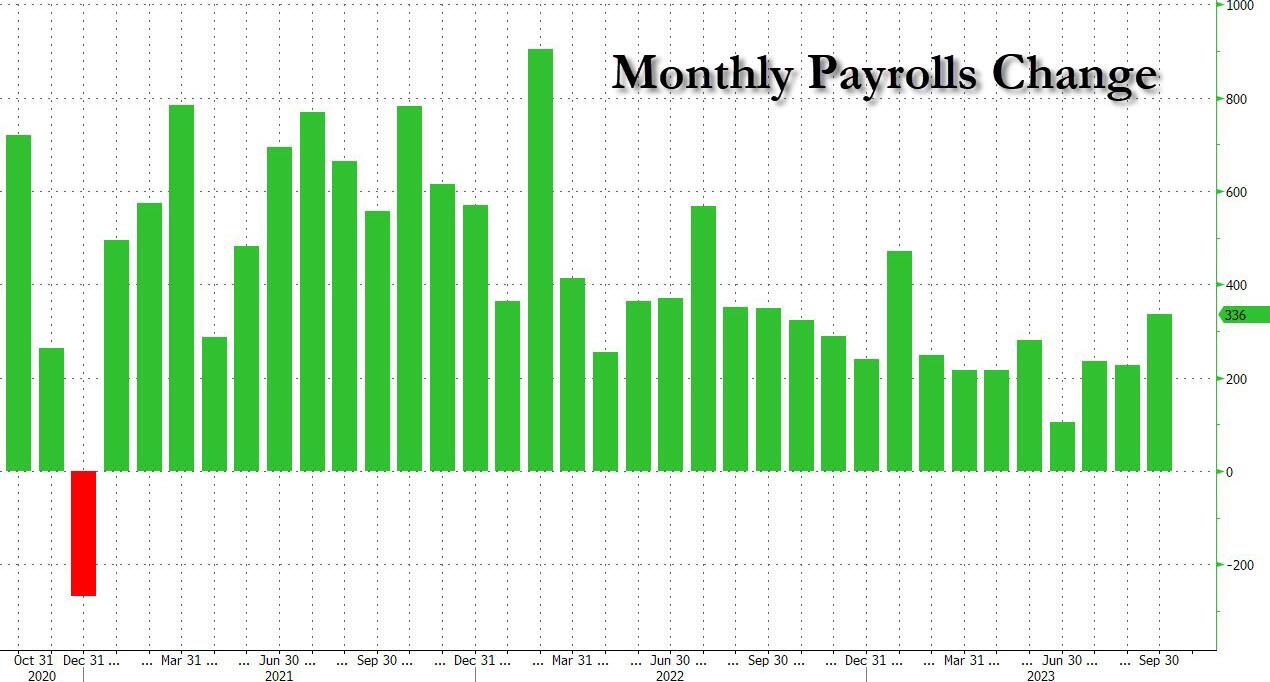

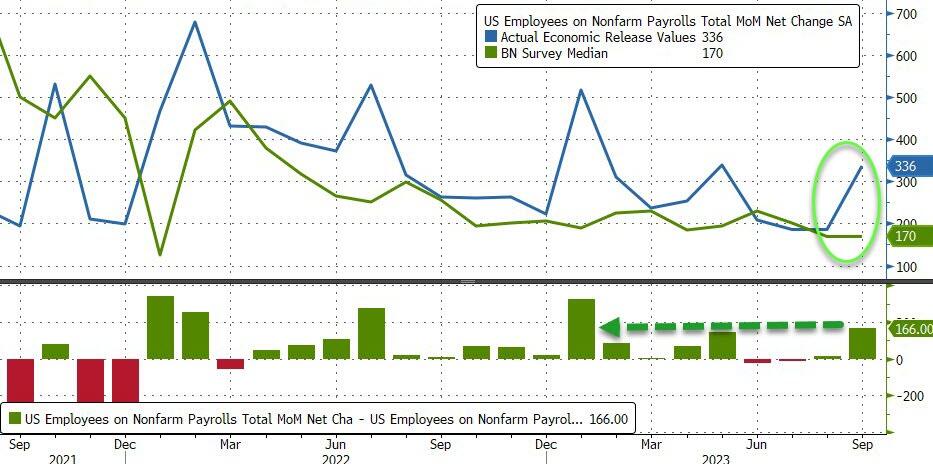

ZeroHedge reports, “With everyone – even the most hardened bulls – expecting the September jobs report to be not only the weakest of 2023 but to presage a big drop in future payrolls data, moments ago the BLS reported that in September the US added a whopping 336K jobs, the highest monthly increase since January…

… and not only double the consensus estimate of 170K, but above the highest sellside estimate of 250K!”

TNX surged to a new high this morning on the monthly Employment Situation Survey. The surge is likely to bring chaos to the markets. Yields continue to rise as I report this event.

ZeroHedge speculates, “Can the system take it?

DB’s Jim Reid with a serious question, although the calculations are a bit simplified. Things that make you go hmmm: By H1 2023, global debt reached $307tn. Not all is tradable, with the Bloomberg Global Agg peaking at $70tn two years prior. Since then, it’s down 23%, indicating a $16tn global market value loss. Projecting this drop across all global debt hints at a $70tn loss. For context, global equities are worth $107tn, and the 2023 global economy is projected at $105tn. These estimates have caveats, but the scale of losses in the debt markets is historically unprecedented both in dollar terms and relative to GDP, raising questions about the system’s resilience.”

USD futures surged to 106.71 this morning on the Jobs Report. More to come.