10:15 am

The Ag Index is heading into its last week of decline prior to its proposed Master Cycle low. As reports of the harvest season come inwe may gain insights on the adequacy of the harvest. However, world wide news shows shortages already rising. This (week) is the time to accumulate food and food-related investments while at the low. The weekly target may be 380.00 to 387.00.

ZeroHedge warns, “We live in perplexing times. It’s almost inconceivable to think that there’s a war being waged against food, an absolute and undeniable necessity of life. Yet, here we stand, on the precipice of what looks like a catastrophic agenda against global sustenance.

So, what’s this newfound hostility against the thing that keeps us alive?

Take a deep breath. Farming uses nitrogen, and suddenly, nitrogen is the new antagonist in the tale of global warming. The narrative is simple: eliminate nitrogen, save the world. Yet, in the name of “preservation,” entire segments of our food production are under siege.

Consider rice – a staple for half the world’s population. Renowned agencies claim, “Rice accounts for roughly 10% of global methane emissions,” emphasizing the urgent need to curtail its production. But the ramifications? Starvation for billions.”

9:55 am

BKX, our liquidity proxy, has declined beneath Intermediate support at 85.43, which may change its signal to a confirmed sell. The Cycles Model affirms that the decline may continue through the end of the month. The Head & Shoulders target is currently in play.

ZeroHedge reports, “Money-market funds saw inflows and banks’ usage of the Fed’s emergency BTFP facility hit a new high this week, so what malarkey does The Fed have in store when it tries to explain what happened to bank deposits.

Seasonally-adjusted, total deposits rose by $17.6 billion last week (the 3rd straight week on SA inflows)…

Source: Bloomberg

And for once, non-seasonally-adjusted deposits rose too (by a huge $121 billion!)”

ZeroHedge further comments, “In the euphoria of buoyant equity markets over the last few months, the many challenges facing regional banks have receded into the background. While it certainly has not been our view, a narrative has emerged that the issues in the sector which erupted in March are largely behind us. Moody’s rating downgrades of 10 US banks last week provide a reminder that the headwinds of increasing capital requirements, higher cost of funding, and rising loan losses continue to challenge the business models of the regional banking sector. While the total volume of debt downgraded thus far is relatively small at around $10 billion, Moody’s put six banks on review for possible downgrade and changed the outlooks of 11 banks to negative from stable. Thus, the volume of bank debt facing the prospect of a downgrade is much higher – well over $100 billion.”

900 am

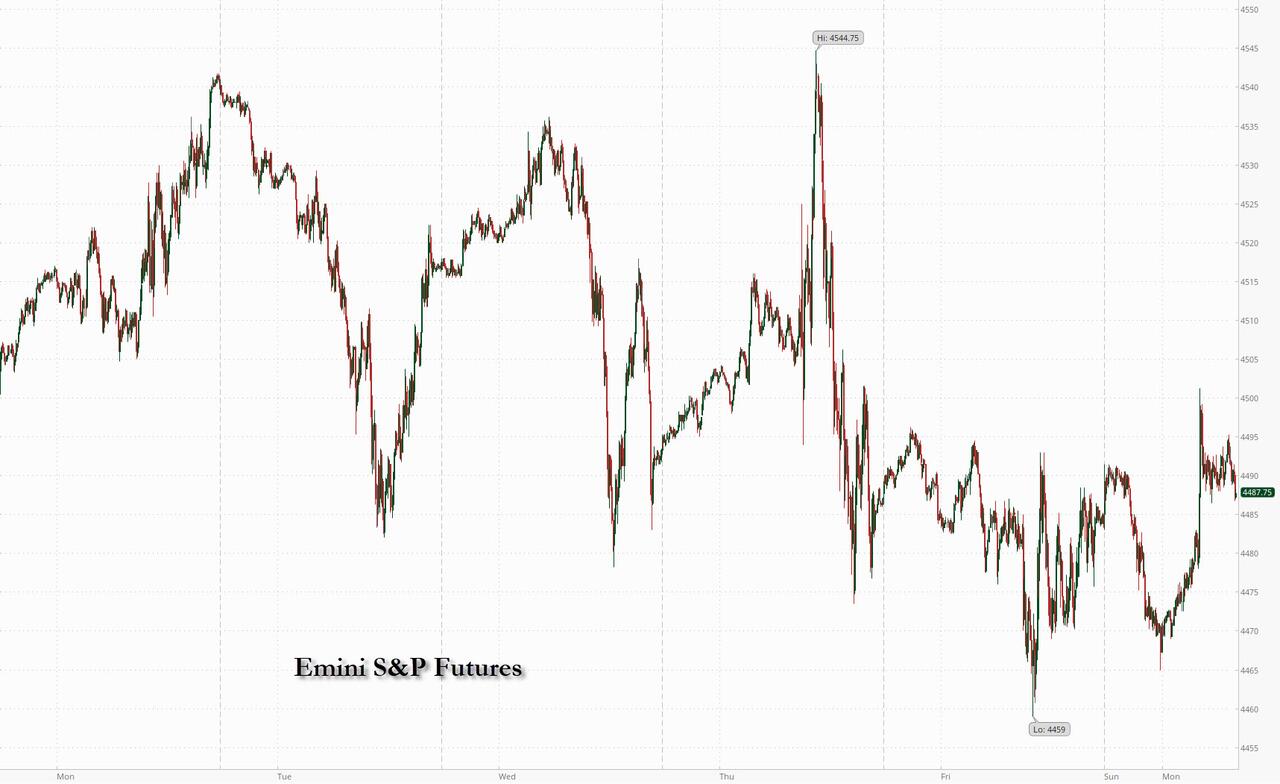

SPX futures have been hovering between 4448.90 and 4485.60 over the weekend session. It is trapped in short gamma. Any jolt or quiver may send the SPX into a self-reinforcing spiral as short gamma forces dealers to sell low and buy high, chasing the ebb and flow of the markets. This week is monthly options expiration, which may lead to a panic decline, especially after the SPX breaks through the 50-day Moving Average at 4428.82.

In today’s op-ex, Maximum Pain for options investors is at 4475.00. Long gamma starts at 4500.00 while short gamma may begin at 4450.00.

ZeroHedge reports, “Futures have reversed earlier losses and are trading higher amid speculation (what else) for Chinese stimulus to address mounting financial and real estate risks, with European markets mixed and Asia slumping on the latest barrage of bad news out of China which however have not (yet) spilled over to the ROW. As of 7:45am ET, S&P emini futures were up 0.2% while Nasdaq futures traded 0.3% higher. 10Y TSY yields are flat at 4.15%, stabilized near their highest level since November. Commodities are lower with USD flat; energy and base metals coming for sale on weaker Chinese growth expectations while Ags mixed on Black Sea headlines. This week’s focus is on Consumer-sector earnings and Retail Sales data, but aside from that this week is an information vacuum into next week’s Jackson Hole so look for positioning/liquidity to guide markets.”

VIX futures rose to a morning high at 16.06 as it rises back toward the trendline. The Cycles Model calls for rising trending strength through the end of the week.

In Wednesday’s (monthly) op-ex, Maximum Pain for options investors is at 17.00. Short gamma is heavily populated between 13.00 and 16.00. Long gamma may begin at 17.00 and has strong support to 60.00. Remember, long or short gamma can be self-reinforcing.

ZeroHedge observes, “The Fear & Greed Index, created and popularized by CNN, is a powerful tool that captures investor sentiment and confidence levels. It rises when markets are greedy and falls when investors are fearful.

In this infographic sponsored by Fidelity Investments, Visual Capitalist’s Rida Khan and Alejandra Dander compare the Fear & Greed Index with the CBOE Volatility Index (VIX) to see the connection between volatile markets and the impulses of investors.”

TNX futures rose to a morning high of 42.00 as it seeks to overtake the August 4 high at 42.06. The Cycles Model suggests another month of rising rates which may lead to the Head & Shoulders target.

9:40 am

The 10-year futures rate just exceeded the prior high. The cash rate may soon follow.

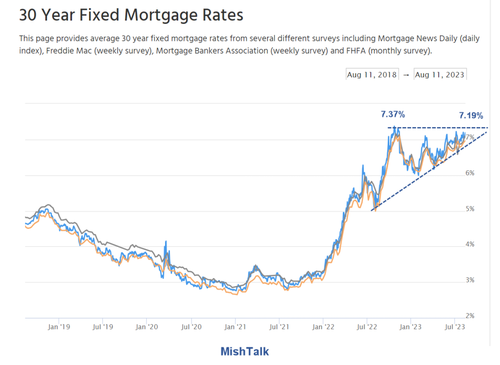

ZeroHedge (Thanks, Mish) observes, “US Treasury yields rose last week despite a relatively tame CPI report. Mortgage rates rose as well. What’s going on?

30-Year Mortgage Chart Notes

- On Friday, August 11, 2023, mortgage rates jumped to 7.19 percent and approach the October 20, 2022 high of 7.37 percent as noted by Mortgage News Daily.

- The 7.37 percent rate was the highest since October of 2000, nearly 23 years ago.”

USD futures rose to a morning high of 103.33, crossing above the mid-Cycle resistance at 102.95. USD is on a buy signal \. Above the 200-day Moving Average at 103.48, the target may be the Cycle Top at 106.15. The Cycles MOdel suggests the USD may rise through the end of the month.