12:12 pm

While SPX futures have declined beneath the trendline at 4010.00, the cash market has not. This morning’s bounce keeps the SPX in positive territory…yet. However, beneath the trendline lies an aggressive sell signal. Confirmation of the sell signal comes beneath the 200-day Moving Average at 3953.84. We may end up waiting until the FOMC minutes are revealed tomorrow on day 257 of the Master Cycle. Remember, a reversal may have been made on Monday where an overlapping 12.9-month Cycle has ended.

12:00 pm

After testing the mid-Cycle support currently at 11863.00, NDX has bounced back above the 200-day Moving Average and descending trendline at 11981.00. A close beneath it reiterates the aggressive sell signal, while a further decline beneath the mid-Cycle support confirms the sell signal. These benchmarks are declining at the rate of 11 points per day, thus explaining the changing reference points.

ZeroHedge remarks, “NASDAQ’s kiss of the 200 day

From above to below the 200 day moving average. The question is, how many people got sucked into this squeeze buying stuff they never wanted to buy…?

Source: Refinitiv

The inverse to last year – time for a move lower?

JPM positioning intelligence team writes: “On a longer term basis, positioning still looks below average, but hard to argue it’s extremely light anymore and the changes in positioning are showing a much more positive swing in the recent past. Thus, perhaps it’s possible that we get a reversal in the rally sometime soon…i.e., the opposite of what happened at the end of last Jan/early Feb when the market bounced after the sharp sell-off at the start of the year.”

7:30 am

Good Morning!

NDX futures declined beneath the mid-Cycle support at 11868.00 to a low of 11388.00, confirming the sell signal. While yesterday was day 255 (within the reversal window) in the current Master Cycle, it may have also fulfilled yet a larger 12.9-month (Primary) Cycle (1 year and 27 days) starting at the January 3, 2022 high. It is not unusual to see Cycles shortened or prolonged to match up with the Cycles of other major indices or with larger degree Cycles that superimpose over smaller ones. Should the Primary 12.9-month Cycles persist, the new pattern may persist until the end of February 2024. The Primary Cycle following may be targeted for the end of March, 2025. This is only an approximation, since the new Primary Cycle may be longer than 12.9 months. This bear market may be larger than anyone has seen or expected since the 12.9 year bear market between 1969 and August 1982. I was a rookie at the time.

NDX op-ex shows Maximum Pain for options investors at 11725.00. Long gamma starts at 11800.00 while short gamma begins at 11700.00.

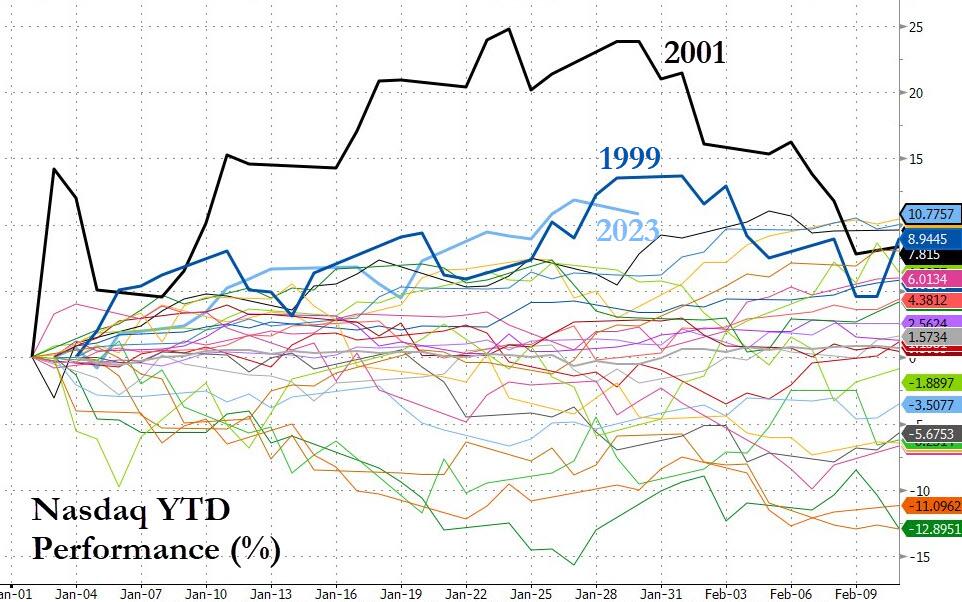

ZeroHedge comments, “Technology-heavy Nasdaq is experiencing one of its best months in two decades despite accelerating mass job cuts at tech firms and increasing risk of recession.

The Nasdaq Composite Index is up 10% so far this month, on track for its best January performance since 2001, when it recorded a 12% gain.

Stocks are flying ahead of the Wednesday FOMC meeting. What could derail optimism is Fed Chair Powell re-emphasizing that the rate hike cycle isn’t over, which would force financial conditions to retighten.”

SPX futures declined to 3993.80, challenging the trendline at 4000.00. A sell signal awaits a close beneath 4,000.00, but be aware that NDX may be taking leadership in this decline. In addition, the DJIA may have reversed yesterday from a second lower high since the December 13 peak.

There seems to be a blackout on the options chains for SPX and SPY since yesterday.

ZeroHedge reports, “US equity futures showed no sign of rebounding on Tuesday from the Nasdaq’s worst single-day drubbing in over a month, with investors growing nervous ahead of this week’s barrage of central bank meetings which include the BOE and ECB Thursday and start tomorrow, when the Fed is expected to hike rates by 25bps; a barrage of earnings reports from some of the world’s biggest companies is also keeping investors busy.

Futures for the Nasdaq 100 and the S&P 500 indexes slipped 0.6% and 0.3%, recovering from even bigger losses earlier in the session as doubts continue to grow about the sustainability of a four-month old rally, which has accelerated further since the start of the year. The Nasdaq benchmark tumbled more than 2% on Monday, its largest decline since Dec. 22 . Despite the pre-Fed jitters, however, both the S&P 500 and the Nasdaq 100 are poised for their best start to a year since 2019 as optimism over slowing inflation and resilient economic growth fueled appetite for risk. However, the start of the earnings season with corporate warnings and reiteration of the Fed’s resolve to raise rates have put a damper on the recovery. Treasury yields dipped, the dollar edged higher and oil extended its recent losses.”

VIX futures made an overnight high at 20.70 as the reversal from Friday’s Master Cycle low (Primary Wave [B]) takes hold. The Master Cycle was stretched to 270 days to fit the 12.9 month Primary Cycle which also ended on Friday. Many analysts are talking about “mean reversion” in the VIX. This does not mean a return to the mid-Cycle at 25.24. For many, the reversion will be just beginning at that level,, since elevated risk does not register until then. The minimum rally may be to the top of Primary Wave [A] at 38.94.

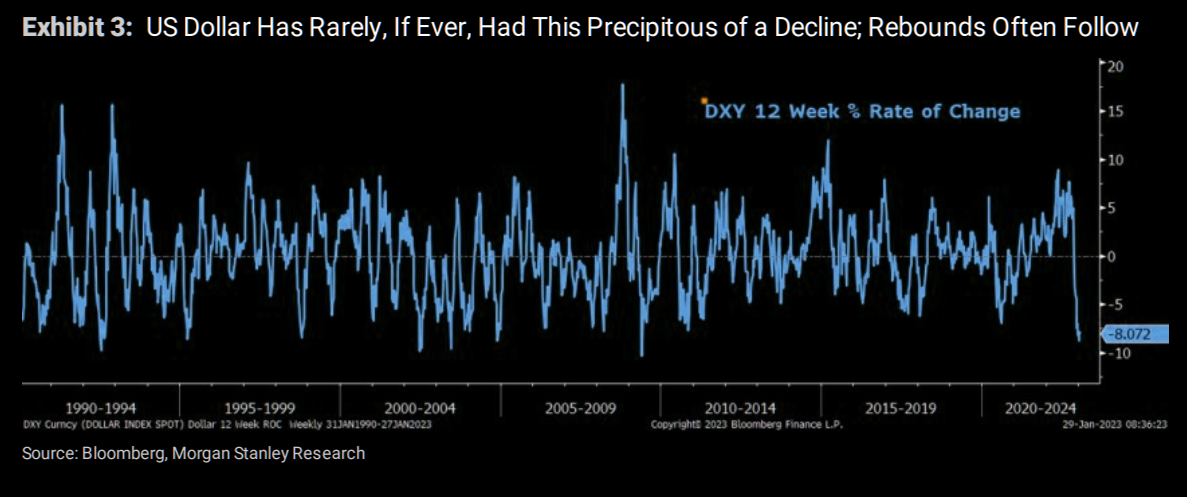

USD futures made a new high at 102.45 this morning. The Cycles Model shows trending strength coming out of the Master Cycle low on January 18. The new Master Cycle may last through the end of February.

ZeroHedge comments, “Got dollars?

The move has been extreme. Time for some mean reversion?

Source: MS

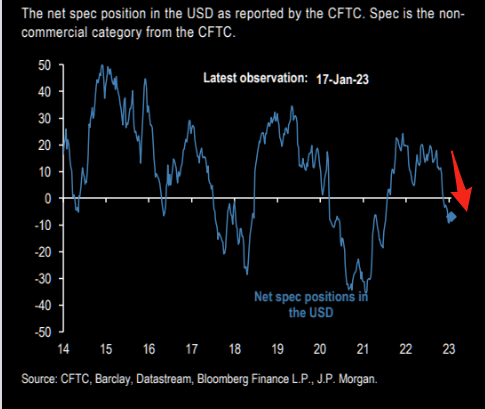

They puked the dollar

Net specs are short. Not massively, but the “sell” has been rather impressive.

TNX was repelled by Intermediate-term resistance at 35.93 and may decline over the next week to the 200-day Moving Average at 33.42. Intermediate Wave (3) of Primary Wave [4] does not appear to be complete and must decline beneath its prior low, if only for a day. Investors buying bonds may not be aware of the corrective nature of this decline in yields.

ZeroHedge observes, “2023 started with a buying-panic in bonds (approaching their best start to a year in over 30 years at one point) as confidence grew about The Fed’s terminal rate (not as high as some feared) and a soft landing (growth cooling and inflation slowing)…

Source: Bloomberg

But, as the last week’s surge in positive macro data (driven largely by better than expected labor market prints), we have seen bonds sold (and stocks bought)…

And hedge funds have piled in, building, as Bloomberg reports, the biggest bearish bet on bond futures on record…”