7:50 am

Good Morning!

NDX futures are lower, having reached a low of 11465.10 this morning. Yesterday’s bump higher may have delayed this Cycle low to a Tuesday-Wednesday time frame. The unusually long Wave 4 was options driven and may have given a false signal to most investors. There are two possible outcomes. The favored path is a 4.3-day decline down to 8000.00 or lower to a Master Cycle low. However, his decline may be a zigzag A-B-C which allows another 2 days of rally, to 12000.00 instead, with a Master Cycle high on Friday.

In today’s op-ex, Max Pain is at 11540.00. Long gamma starts at 11575.00, while short gamma begins at 11530.00. NDX nay begin its day in short gamma, making it more volatile.

ZeroHedge comments, “There has been a surge in the number of advancing NYSE stocks which is typically a very reliable sign of further positive equity returns in the coming weeks.

The bounce off the recent lows in stocks has been impressive. Negative sentiment and short positioning found the spark they needed in the sharp fall in the JOLTS job openings survey on Tuesday. As one wag on Twitter put it, firms finally figured out that all they needed to do to force the Fed to pivot was offer fewer jobs.”

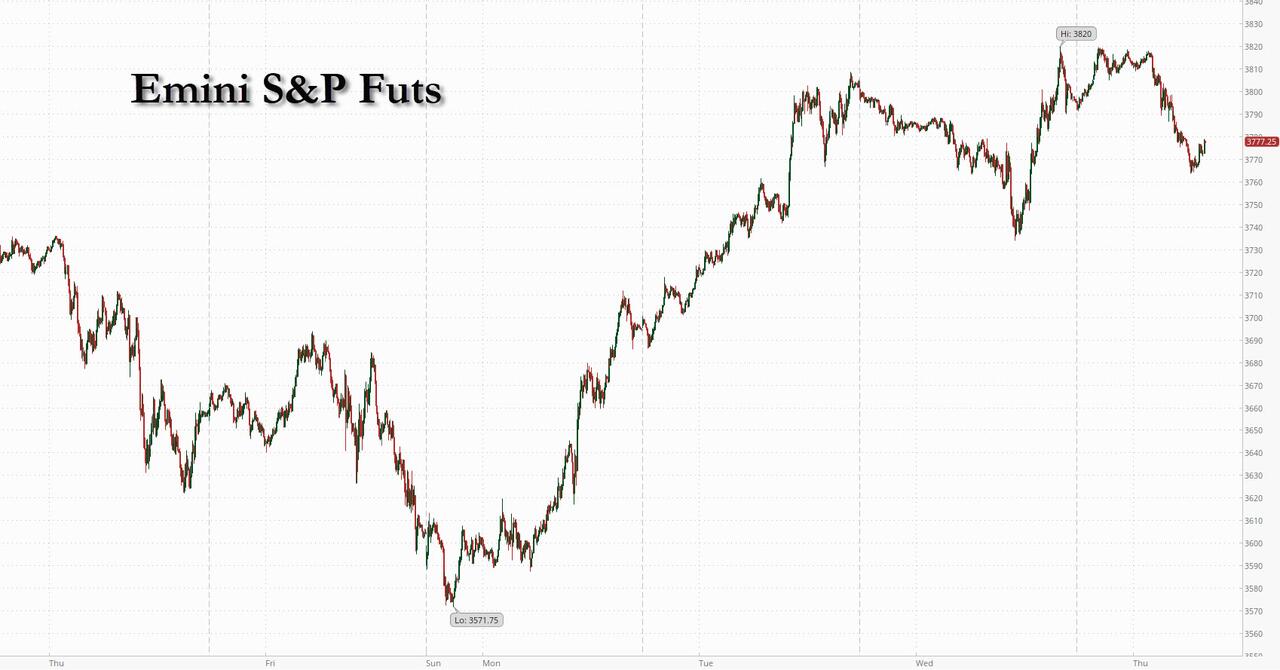

SPX futures are down again this morning, reaching a low of 3750.80. Yesterday’s late day surge may have clarified the location of the favored Master Cycle low which is due next week. It also confirmed how strong a hold the options market has on Equities. Today may begin a 4.3-day decline to the anticipated Master Cycle low. The alternate is an extended rally, possibly ending on Friday along with the current Master Cycle at a high, instead of a low.

In today’s op-ex, Max Pain is at 3770.00. Long gamma may begin as low at 3780.00 while short gamma starts at 3750.00. Short gamma intensifies at 3700.00.

ZeroHedge reports, “Two days ago, when stocks were melting up even as oil was storming higher and threatened to rerate inflation expectations sharply higher, we mused that algos were clearly ignoring this potentially ominously convergence.

And while yesterday we saw the first cracks developing in the meltup narrative as oil extended gains following OPEC’s stark slap on the face of the dementia patient in the White House, it was only today that the “oil is about to push inflation sharply higher” discussion entered the broader financial sphere, with JPM writing this morning that “OPEC+ presents inflation risk”, Bloomberg echoing JPM that “OPEC+ alliance’s plan to cut oil supply stoked inflation fears and as traders awaited labor-market data to gauge the risk of recession” and Saxo Bank also jumping on the bandwagon, warning that OPEC+ supply cut will worsen global inflation which “raises the risk of inflation staying higher for longer” and “sends the wrong signal to the US Federal Reserve… It could send a signal that they have to keep on their foot on the brake for longer.”

And sure enough, with oil rising above its 50DMA for the first time since Aug 30, futures have slumped overnight as oil kept its gains, with S&P and Nasdaq 100 futures both sliding 0.5% as of 730am, while Europe’s Stoxx 600 erased an advance and traded near session lows. US crude futures held on to weekly gains of about 11% after the oil cartel said it would cut daily output by 2 million barrels. Treasuries were steady, the 10Y trading around 3.77%, with the 2Y rate hovering about the 4.15% level.”

VIX futures consolidated overnight, staying at the lower end of the trading range. Should SPX continue to rally, we may see VIX decline to the mid-Cycle support at 26.10. In either event, the VIX is near its inflexion point to move higher.

TNX is consolidating in a very tight range. However, despite yesterday’s strong move, TNX may be setting up for an even stronger move higher, starting today.

USD futures remained at the upper end of its trading range, not making new highs, but showing strength, nonetheless.

Investing.com observes, “The bout of profit-taking on long dollar positions begun last week has carried into the start of this week. Despite the escalating rhetoric, the yen is not participating today and is trading within the pre-weekend ranges. The greenback’s lows have been set in the European morning and have stretched the intraday momentum indicators, suggesting that North American dealers may not follow suit. ”