7:55 am

Good Morning!

NDX futures are consolidating beneath yesterday’s high. The bounce off yesterday’s low lifted the NDX to 13388.10, a 41% retracement of the decline off the top. It has since eased lower. Despite the notion that the NDX entered a bull market yesterday, it only retraced 44% of the decline from the top made on November 21.

In today’s op-ex, Max Pain is at 13310.00. Puts dominate beneath 13300.00 with no discernible gamma zone. Calls dominate at 13320.00 with long gamma at 13350.00. In today’s op-ex for QQQ (324.08), Max Pain is at 321.00. Calls rule above 322.00 while long gamma begins at 330.00. Puts dominate beneath 320.00 with short gamma also starting at 320.00.

ZeroHedge comments, “Ten days ago, when predicting why the current rally would continue indefinitely, we quoted Goldman which said that “No One Is Positioned For Any Good News” with the bank’s Prime Brokerage also revealing that hedge fund tech shorts had hit a record, which to us ensured that this ‘Most Hated Rally‘ would continue.

We were right.”

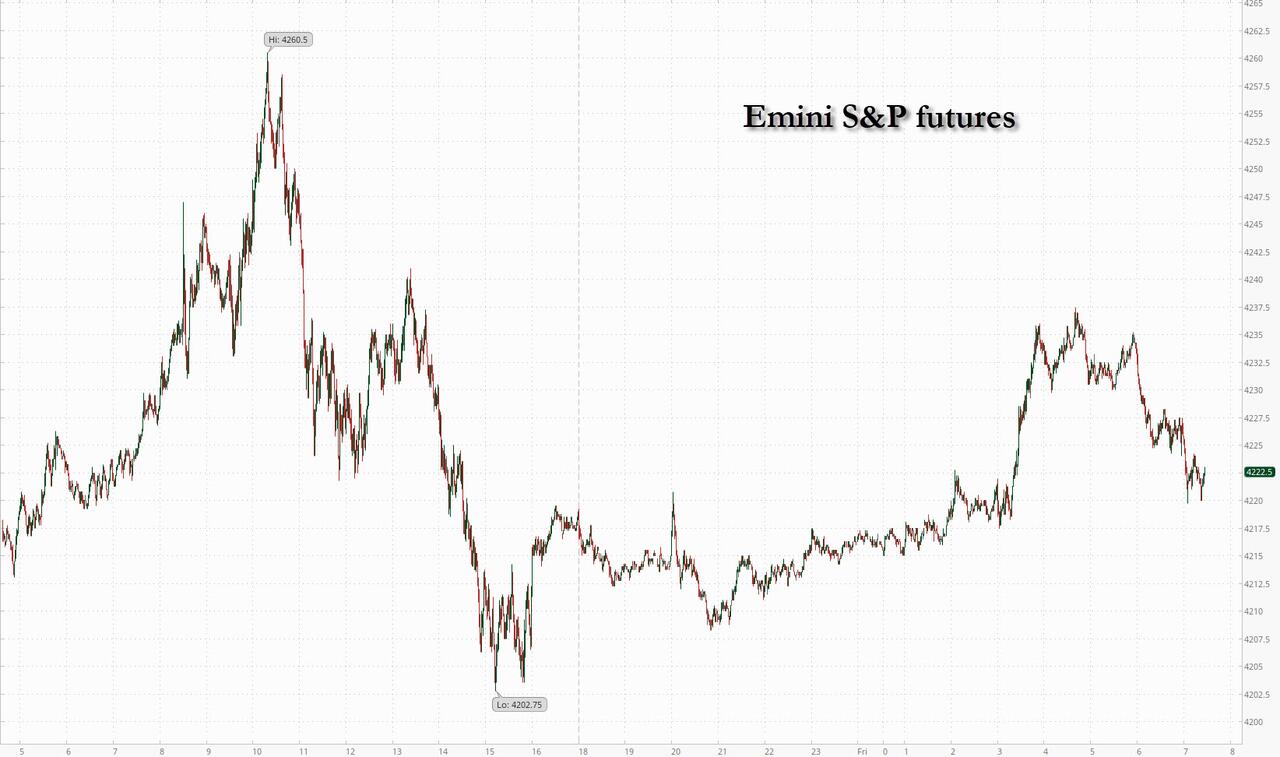

SPX futures probed at the Lip of the Cup with Handle and was reversed at 4234.90. It has since eased back beneath the trendline, after having achieved a 50% retracement at 4225.62. It is consolidating near the 50% retrace, leaving analysts scratching their heads as to the direction it will go next.

In today’s op-ex, Max Pain lies at 4180.00, leaving room for a decline into the close. Calls dominate above 4185.00 and long gamma may begin at 4205.00. Puts rule beneath 4170.00 and short gamma starts at 4150.00.

ZeroHedge reports, “European stocks and US futures rallied on the last day of the week, however traded well off session highs in extremely low-volume trading and tracked the sudden drop in oil, as investors pressed bets that easing inflation will allow the Fed to pivot to less aggressive rate hiking (if not ease outright). S&P 500 and Nasdaq 100 contracts rose about 0.3%, with both underlying indexes set to post their longest sequence of weekly gains since November. Treasury yields were steady at 2.87% and the US dollar rose but was set for the worst week since May. Crude oil fell, reducing its biggest weekly gain in about four months. Gold headed for a fourth weekly gain and Bitcoin was summarily smacked down below the $24,000 level yet again as crypto bears fight to preserve the upper hand.

For the second day in a row an attempt to void the bear market rally narrative by pushing spoos above the 50% fib retracement level is being defended by bears, with futures trading at 4222, or right on top of the critical level, which also doubles as the 100DMA. If broken through it could lead to substantial upside gains as even more bears throw in the towel.”

VIX futures traded in a range between 19.89 and 20.35, waiting for the market to make its move. The (former) Master Cycle has been stretched to 280 days, which is highly unusual.

Next Wednesday’s op-ex shows Max Pain at 14.50. Puts dominate the options chain between 15.00 and 25.00 with short gamma beneath 25.00 as well. Calls start at 26.00 and long gamma appears at 27.00.

CNBC reports, “A key measure of stock volatility is providing clues that investors should be wary of the recent market rally, according to Data Trek Research co-founder Nicholas Colas.

The CBOE Volatility Index has come off its most recent mid-June highs and now is trading around its long-term average of 20.

At the same time, the S&P 500′s top five sectors by market cap have been moving largely in lockstep up and down with the index.”

TNX is backing away from its attempt at the 50-day Moving Average at 29.68. Next week’s proposed Master Cycle pivot suggests another low may be at hand. Strength may not reappear until the end of next week.

ZeroHedge reports, “After two stellar refunding auctions to start the week, moments ago the Treasury concluded the sale of its quarterly refunding week with the sale of $21BN in 30 year paper. Surprisingly – after a solid 3Y and fantastic 10Y sale earlier this week – today’s auction could certainly have gone better.

Stopping at 3.106%, the high yield dropped fractionally from last month’s 3.115%, but what is more notable is that after 3 consecutive stropping through auctions, today’s sale tailed the When Issued 3.095% by 1.1bps, which is strange considering the notable selloff into the auction.

The bid to cover of 2.310 dropped from 2.436 in July and was also below the six-auction average of 2.37.”