3:45 pm

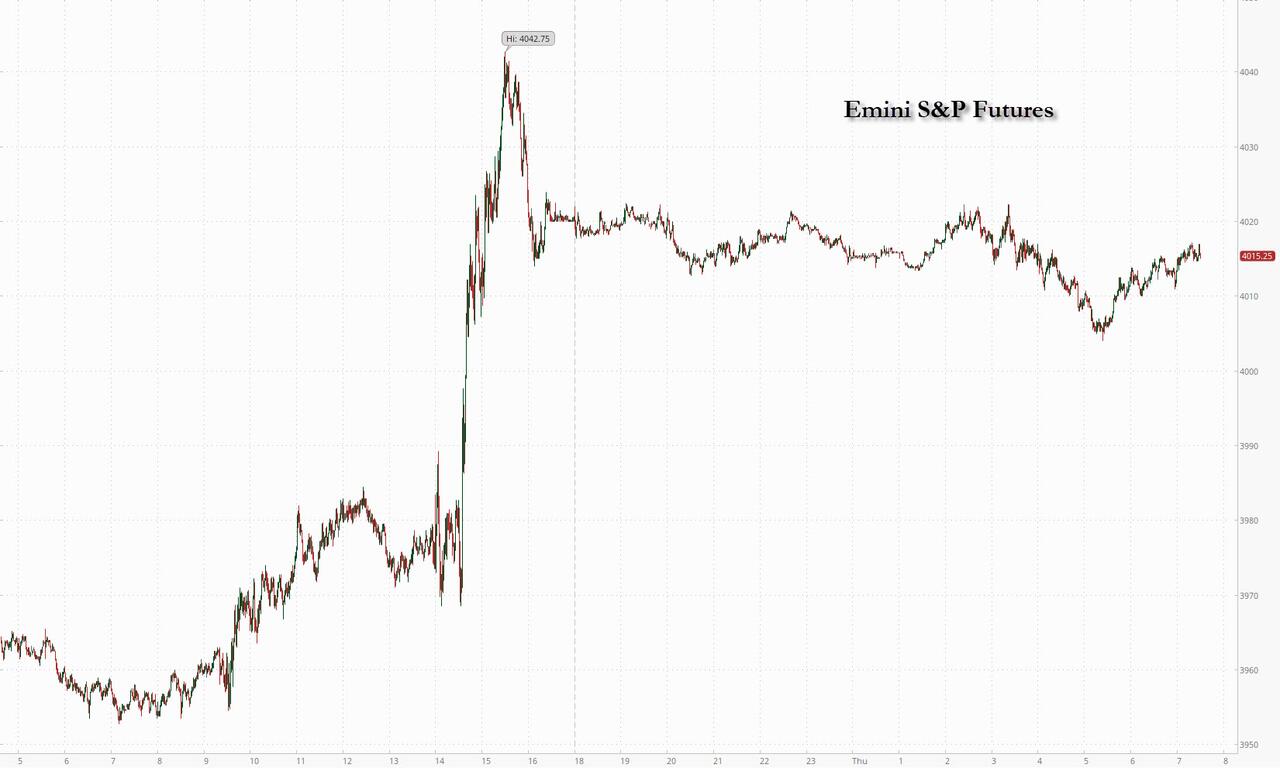

SPX has risen nearly to the 38.2% retracement of the entire decline from January 4 to June 17, approximately 5.5 months. Today is calendar day 41 out of the low and 28 market days have elapsed since then. The Cycles Model suggests another possible day of strength tomorrow. The alternative may be a violent reversal, but that is more likely to happen early next week. Yesterday I was marveling at the accuracy of the Cycles. One or two days of extension does not alter the analysis. It may fall within the “normal” range that allows these discrepancies.

Today is day 248 of the current Master Cycle. While not common, a Master Cycle may turn in as little at 241 days. There are three nearby resistance levels. The first is the 38.2% Fibonacci level at 4085.07. Next, Wave Equality is reached at 3091.00. Finally, we have round number resistance at 4100.00.

ZeroHedge remarks, “The market’s dovish price-action response to the perception of “past peak tightening” from the Fed remains mutually exclusive from what was a “still hawkish on inflation” message, as Chair Powell did not stand-down there – repeating that it is the only mandate and largest challenge right now, outweighing any growth (i.e. “recession”) concerns.

“We’re going to be focused on getting inflation back down and as I’ve said on other occasions, price stability is really the bedrock of the economy. Nothing works in the economy without price stability. We can’t have a strong labor market without price stability for an extended period of time. We want to get back to the kind of labor market we had before the pandemic where differences between racial and gender differences and that kind of thing were at historic minimums. That’s not going to happen without restoring price stability. So, that’s something we see as, as something we simply must do. And we think that in the — we don’t see it as a trade-off with, with the employment mandate. We see it as a way to facilitate the sustained achievement of the employment mandate in the longer term.”

And Nomura’s Charlie McElligott points out that this is how things can get “awkward” again in coming months to keep things “uneasy” versus the perception of “dovish pivot,” as Powell’s repeated emphasis on the June SEP (which shows ongoing rate hikes into 2023) looked clearly “intentional,” which would then seemingly push-back on the market’s “quick turn” pricing of early rate CUTS seen in start 1Q23…”

8:15 am

Good Morning!

SPX futures rose to 4027.20, then eased back toward 4000.00, as suggested at the close. This is a very options-driven market, since today’s Max Pain is at 4010.00. Long gamma may begin at 4025.00. Puts take over beneath 4000.00. In tomorrow’s op-ex however, Max Pain is at 3945.00. The dealers’ dilemma is how to keep the market from going too far in either direction.

ZeroHedge reports, “One day after the Nasdaq 100 posted its biggest jump since November 2020 when the market exploded higher after it interpreted Powell’s forward guidance purge and comment that it is “likely appropriate to slow rate increases at some point” as more dovish than expected, US stocks were set to pull back as downbeat earnings and a dire outlook from bad to Metaworse weighed on demand. Futures contracts on the technology-heavy Nasdaq 100 dropped 0.5% by 7:15 a.m. in New York, after the underlying gauge rallied 4.3% in the previous session. S&P 500 futures were down 0.2% after the benchmark index jumped to its highest level in seven weeks. Treasury yields were little changed and the dollar and bitcoin edged up.

VIX futures declined further to 22.84, an 85% retracement. The August 3 op-ex Max pain appears at 24.00 while long gamma begins at 26.00. It is on an aggressive buy signal, confirmed above the mid-Cycle resistance at 24.78.

TNX appears to be consolidating in place, awaiting it’s reversal after a Master Cycle low. The Cycles Model reveals no particular strength, suggesting that yields may flop around for a while before giving a directional push.

ZeroHedge observes, “Did He, Or Didn’t He? That Is The Question

Did Powell come across as dovish? Did he make the case that the Fed would take into account economic risk? That the Fed was data dependent? That the Fed was almost done hiking?

I’ve read the transcript several times and keep thinking that:

- He did a very good job suggesting that we are near a neutral rate. That is positive for markets and dovish.

- He mentioned data dependency several times and did mention some concerns about the economy. Slightly dovish.

- On the other hand, he tried to drive home the point that fighting inflation was still the priority. That he would sacrifice the economy and jobs for lower inflation, since inflation is so problematic. He didn’t take even 75 bps off for September and did say they could hike above neutral to fight inflation. Hawkish.

USD futures declined to 105.93 before moving higher. The Cycles Model projects growing strength starting today and lasting the next two weeks. A “normal” final push higher may take USD to 111.00-112.00. Additional Cyclical strength may push it higher.

Crude oil futures rose to 99.83 in the overnight session, as it begins to test round number resistance at 100.00. The Cycles Model suggests a bounce to mid-August with a potential target at the 50-day Moving Average at 108.16.