8:00 am

Good Morning!

NDX futures rose to an overnight high at 17607.90, but then have pulled back . It closed yesterday just under the 38.2% Fibonacci retracement value at 17489.54. This morning’s probe may attempt to reach the 50% retracement value at 17651.41, but is running out of time. Should it continue to rally at the open, it may not last more than an hour or so. In the meantime, investors anticipate the end of the buyback blackout period, starting this Friday..

Today’s options chain shows Maximum Investor Pain at 17500.00-17510.00. Long gamma does not emerge until 17700.00, while short gamma appears to be in short supply. A neutral options market.

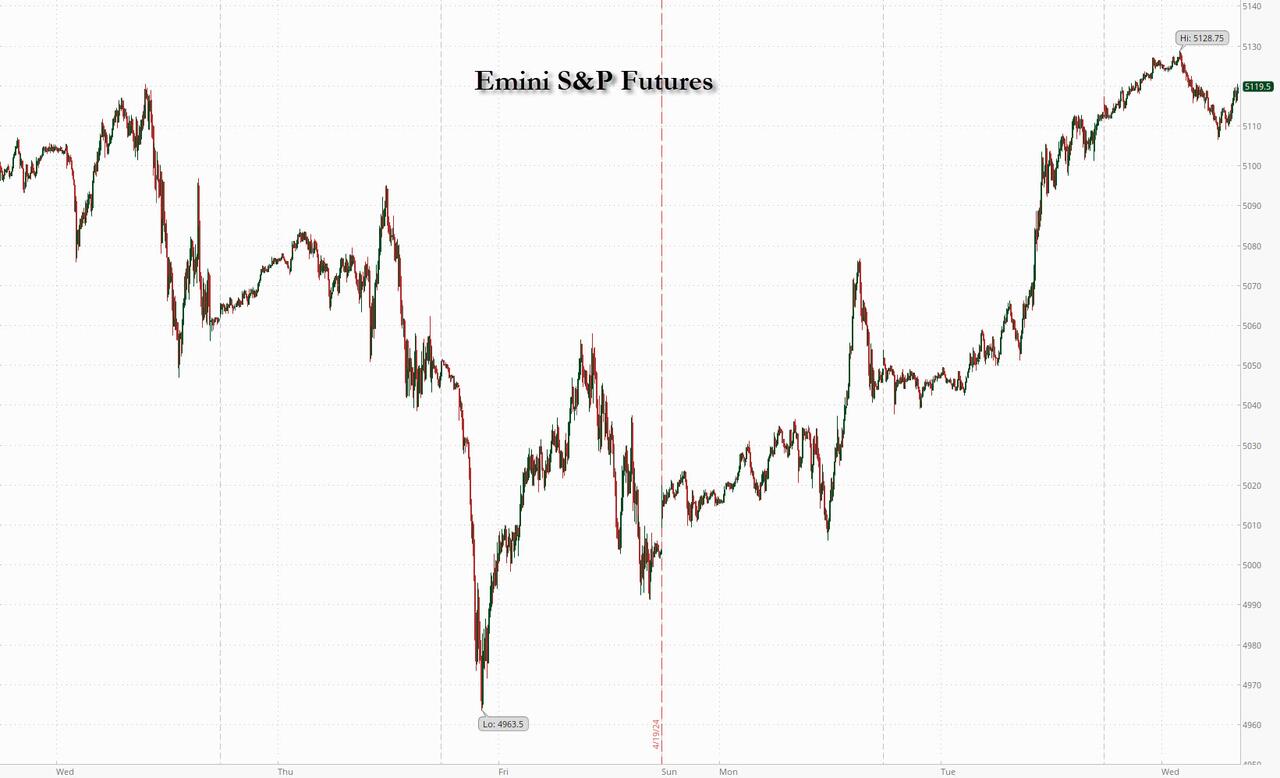

SPX futures rose to 5092.00 in the overnight session after closing at the 38.2% Fibonacci retracement value at 5070.16. The 50% retracement value lies at 5100.19. A positive cash open may only last another hour or so. There is a potential new Head & Shoulders structure which targets the right shoulder at 5081.00-5083.00. Its potential target may be beneath the 200-day Moving Average at 4680.00.

Today’s options chain shows a highly contested Max Pain level at 5050.00. Long gamma may start at 5075.00, but only gathers strength above 5095.00. Short gamma becomes strong beneath 5040.00.

ZeroHedge reports, “Equity futures rose for the third day in a row – last week’s brutal drubbing a distant memory – with tech outperforming as Tesla soars premarket after Elon Musk vowed to launch less-expensive vehicles as soon as late this year while Texas Instruments jumped 7% after it forecast revenue above the average analyst estimate. The tech rally has kept stocks afloat after disappointing earnings in the European banking and luxury sectors. Technology shares stood out in the US, with contracts on the Nasdaq 100 rising 0.6% compared with a 0.3% gain for S&P 500 futures. Bond yields are 1-3bps higher, helping to boost the USD. Commodities are lower though base metals are positive. The macro data focus is on Durable/Cap Goods with META headlining today’s earnings releases. Keep an eye on macro read throughs from F, HAS, NSC, ODFL, SYF, WHR earnings, among others. ”

VIX futures made their low this morning at 15.55. VIX is in a consolidation that allows it to begin its upward journey today. A breakout may put the VIX in a position to rival the 2020 rally.

Wednesday’s op-ex shows Max Pain at 16.00. Short gamma dwells between 13.00 and 15.00. Long gamma starts at 18.00 and may go as high at 50.00.

TNX futures rose to 46.58 this morning and the cash market is not far behind. As indicated earlier this week, TNX may complete this week in strength, allowing it to reach the Cycle Top resistance at 48.50.

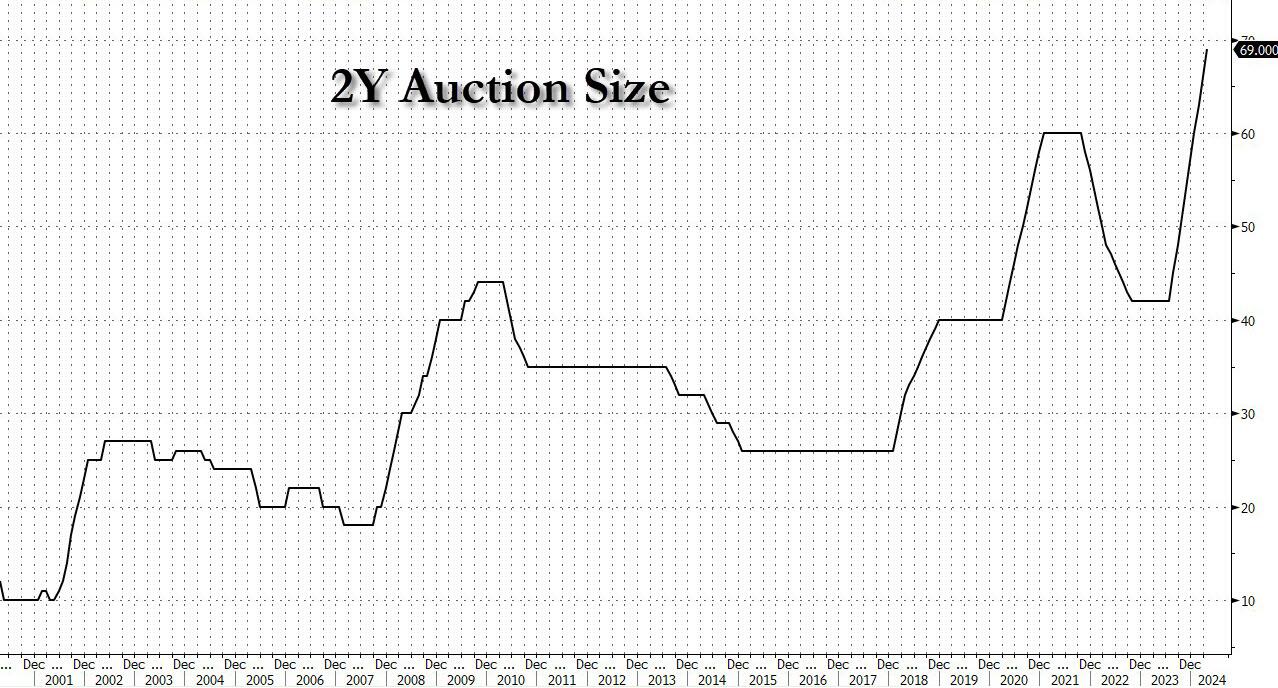

ZeroHedge reports, “Bond traders were paying close attention to today’s 2Y auction not only because at $69 billion in size, it would once again break the record for biggest 2Y auction issuance on record, but also because it comes at a time when yields are trading just shy of 2024 highs. The results, which were announced moments ago, however were solid and helped push yields to session lows, however briefly.

Here are the details: the size of today’s 2Y auction was $69 billion, $3 billion more than the March issuance of $66 billion and the biggest on record.

So considering that the high yield of 4.898% (which was well above last month’s 4.595% but below the record high of 5.085%) stopped through the When Issued 4.904% was a bit of an achievement.”

USD futures continue to consolidate instead of declining. This suggests there may be more strength in the rally than it has been credited for. If so, we may look for a resumption of the rally after a shallow decline later this week.

Gold futures may be consolidating after having made an aggressive sell signal beneath 2340.00 on Monday. Confirmation of the sell signal lies beneath the Cycle Top support at 2292.88. While gold may be a store of value, it is not an alternate currency. Its rise in value parallels the rise in market liquidity. However, it may also fall with the decline in liquidity.