11:11 am

NDX rose to the Max Pain level, but could not escape short gamma. A decline beneath 16973.94 puts the NDX into serious short gamma which may accelerate the decline. Gamma is at the most negative reading year-to-date, but has room to become even more negative.

7:45 am

Good Morning!

NDX futures have risen to 17171.30 this morning. Having broken through the 100-day Moving Average at17360.00 on Friday, it is likely to bounce back to test resistance there. The Cycles Model suggests a possible 2-day bounce before reversing back to the downside. Hedge funds and CTAs appear to be buying the dip.

Today’s options chain shows Maximum Investor Pain at 17130.00. Long gamma begins at 17175.00 while short gamma starts at 17100.00.

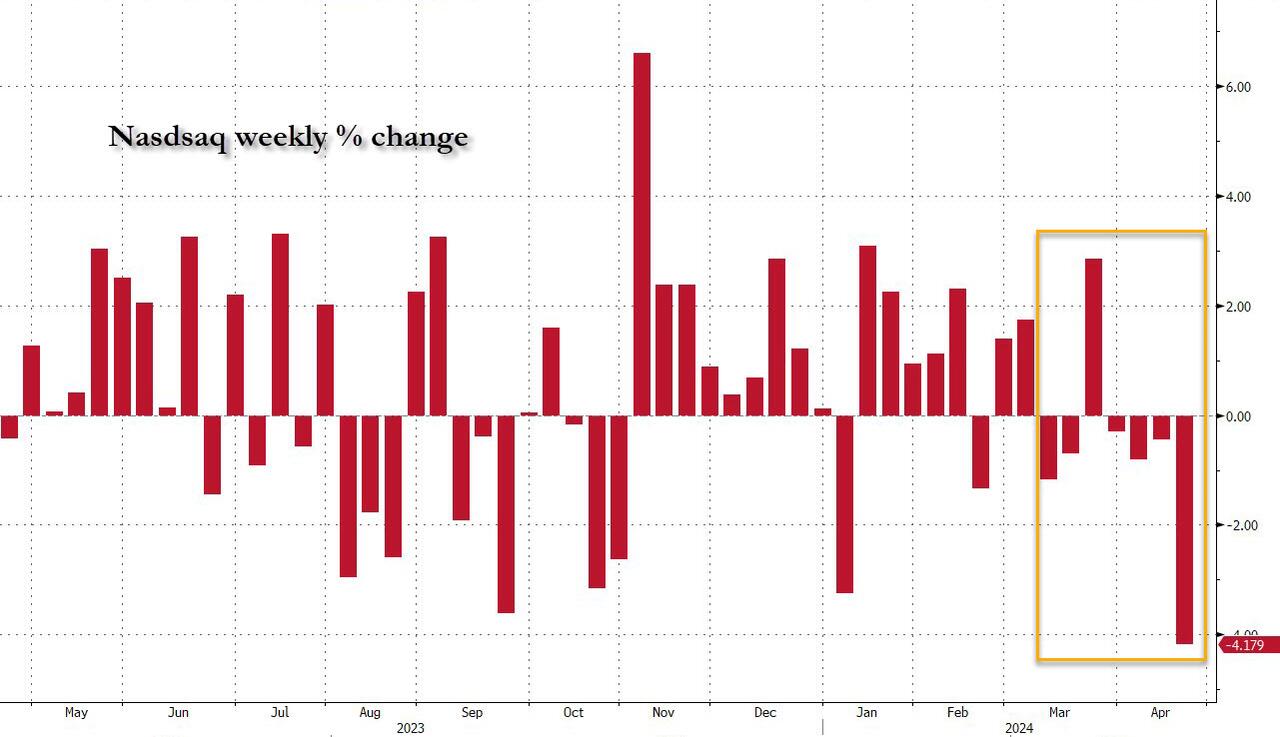

ZeroHedge comments, “It’s been a very ugly week for momentum names, but since these days that really means AI and/or mega tech, we can just saw this has been a very ugly week for the Nasdaq. And sure enough, with the QQQs down 0.4%, the Nasdaq is now pacing for its worst week in over a year – and is down 6 of the past 7 weeks…

… on what Goldman trader Peter Callahan calls a complicated technical backdrop (CTAs, lower retail participation, Nasdaq now testing 100-dma, seasonality), sideways earnings revisions thus far (ASML, TSM and even Sheridan’s NFLX EPS revisions were only 1-2% last night), a tense geopolitical backdrop (overnight headlines) and elevated positioning are testing conviction into a busy week of earnings. ”

SPX futures bounced at the 1987 trendline and have risen to a morning high of 4998.40 thus far. The Cycles Model allows a possible 2-day bounce that may ease the oversold condition. Overhead resistance lies at 5026.00-5050.00. While hedge funds may be taking downside profits, the chances of a short squeeze may be limited.

Today’s options chain shows Maximum Investor Pain at 4995.00. Long gamma may begin at 5005.00 while short gamma starts at 4975.00. Long gamma may assist the bounce.

ZeroHedge reports, ” US equity futures rose, putting the S&P on pace for its first gain after 6 straight days of losses, as focus shifted from Middle East tensions to a raft of company earnings this week, including four of the Mag7 tech megacaps which got hammered last week. At 7:40am, S&P emini futures gained about 0.5% after the index recorded its worst week since March 2023; Nasdaq futures were 0.6% higher while Europe was green across the board. Demand for havens eased as traders took comfort from the absence of further escalation from Iran following Israel’s retaliatory strike. A Bloomberg dollar index was steady as geopolitical tensions eased and the Fed entered a blackout period before its May 1 policy decision, while the yield on 10-year US Treasury yields rose three basis points. Oil reversed an earlier slide while gold dropped around 1.4% as demand for haven assets fades.”

VIX futures declined to 17.02 this morning. The Cycles Model suggests another possible day of correction before resuming its rally. The structure appears to be an expanded flat correction or possibly an irregular correction (requiring a deeper correction).

Wednesday’s op-ex shows Maximum Investor pain at 17.00. Short gamma resided between 13.00 and 15.00. Long gamma starts at 19.00 and remains strong to 39.00.

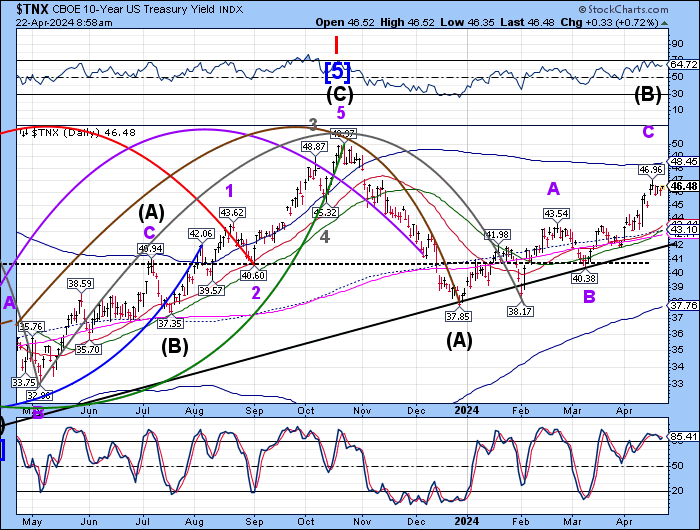

TNX futures have started climbing again. While the prior high on April 16 occurred on day 256 of the Cycles Model, the structure may not be complete. A probe to a new high mayb alleviate the situation and complete the current Master Cycle.

USD futures appear to be consolidating beneath the April 16 high. Should the USD decline beneath 106.50, the USD may have a i-month decline ahead. However, a rally above 106.32 may produce a month-long extension of the rally. An interesting conundrum.

Gold futures declined to 2347.10 thus far this morning. A decline beneath 2340.00 may create an aggressive sell signal. This signal should not be ignored, as the Cycle Model indicates a potential decline until early June.