2:15 pm

NDX may be due for a bounce, but overhead resistance may prevail at 17721.15. NDX may be completing the 5th week of a 9-week decline. The next segment may be much worse than the first. Signals abound for the wary.

ZeroHedge remarks, “A technical sell signal for the Nasdaq has hit levels not seen since the tech bubble.

However, it should be taken in the context of a still supportive economic backdrop, with buoyant excess liquidity and low near-term recession risk.

The Hindenburg Omen compares the percentage of stocks in a stock index making new 52-week lows versus 52-week highs.

When both are rising above a certain threshold, and we are near a one-year high in the index, the signal activates.

For the Nasdaq, more omens have triggered so far this year than in any calendar year since the 2000 tech-driven top.”

7:50 am

Good Morning!

NDX futures have risen to a morning high of 17781.40, unable to overcome yesterday’s bounce high at 17817.73. The 50-day Moving Average is at 17973.58. This show of weakness suggests another decline in the making. The next substantial support may be the 100-day Moving Average at 17320.00.

Today’s options chain shows short gamma well entrenched at 17800.00 and below.

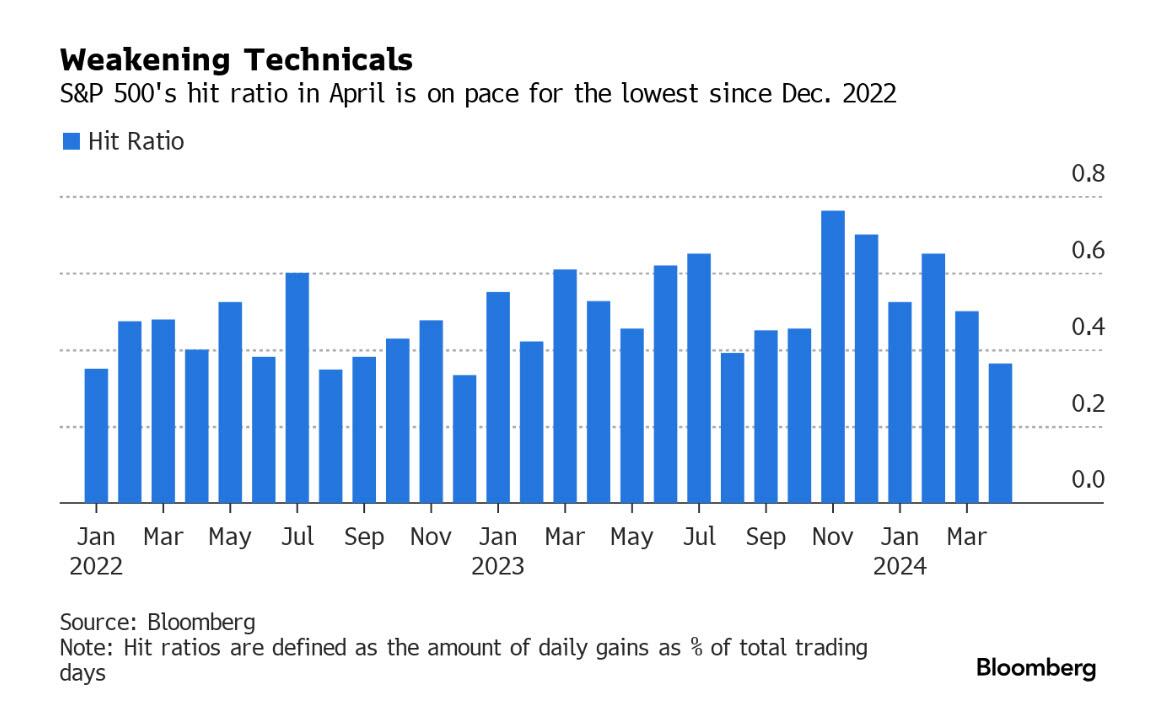

ZeroHedge observes, “The stocks selloff is displaying features that were often seen back when shares plunged in 2022, which is a warning for equities now.

The S&P 500 has fallen for seven of the past 11 trading sessions through Monday, leaving its hit ratio — the amount of daily gains as percentage of total trading days — at 36.4%, on pace for its weakest since December 2022.”

SPX futures peaked at 5075.90, short of yesterday’s high. The path of lease resistance appears to be lower, with the 1987 trendline neat 4950.00 and the 100-day Moving Average at 4921.45 as reasonable targets for the nest decline.

Today’s options chain shows Max pain at 5075.00. Long gamma starts at 5100.00 while short gamma begins at 5050.00.

ZeroHedge reports, “US equity futures and European markets are higher, reversing several days of losses after positive earnings from some of Europe’s biggest companies lifted the mood as markets were roiled by a more hawkish outlook for interest rates. Futures on the S&P 500 rose by 0.4% reversing three days of losses that saw the S&P drop by 2.9% to close Tuesday near a two-month low. Nasdaq 100 contracts edged higher, while consumer products and services led an advance of 0.7% in the Stoxx Europe 600. Treasury yields retreated from a 2024 peak helping small-caps outperform pre-market, and a gauge of the dollar snapped five days of gains that took it to a five-month high after Powell said it would likely take longer to have confidence that inflation is headed toward the central bank’s target. Commodities are mixed with metals stronger and oil weaker even as tensions in the Middle East persisted, while Israel weighs a response to Iran’s weekend attack. Macro data is light today with Beige Book, TIC (keep an eye on CB sales), and mortgage apps (which rose 3.3% after rising 0.1% last week).”

VIX futures declined to a morning low at 17.03. The normal retracement level may be closer to 16.66.

Today is the monthly options expiration for the VIX. Max Pain resides at 15.50. Short gamma fills the space between 13.00 and 15.00. Long gamma may begin at 17.00 and strengthens above 20.00.

TNX has pulled back from its high, but may have another day or two of strength in its rally. The Cycle Top resistance at 48.37 may still be its target, or something very close.

USD futures spent the last two days testing the high at 106.44. Today, it appears to be consolidating beneath that high, after spending 273 days in the Master Cycle. The new Master Cycle appears to run through the month of May. There is nonew target for this move.

Gold futures appear to be consolidating today, but it has developed a clear aggressive sell zone beneath 2340.00. Should it fall beneath that level by the week-end, we may expect to see some drama in the decline.