10:15 am

BKX broke beneath its 50-day Moving Average at 98.19 on Friday, but recovered above temporarily. Today it may make a permanent break beneath the 50-day, confirming its sell signal.

ZeroHedge reports, “Money-market funds saw a small outflow last week (surprisingly small given how close to Tax-Day we are), leaving them still near record highs over $6 Trillion (and the trend of increased deposits at banks has been accelerating)…

Source: Bloomberg

Interestingly, amid all the talk of tapering QT, The Fed balance sheet was basically unchanged last week (-$1.4BN)…”

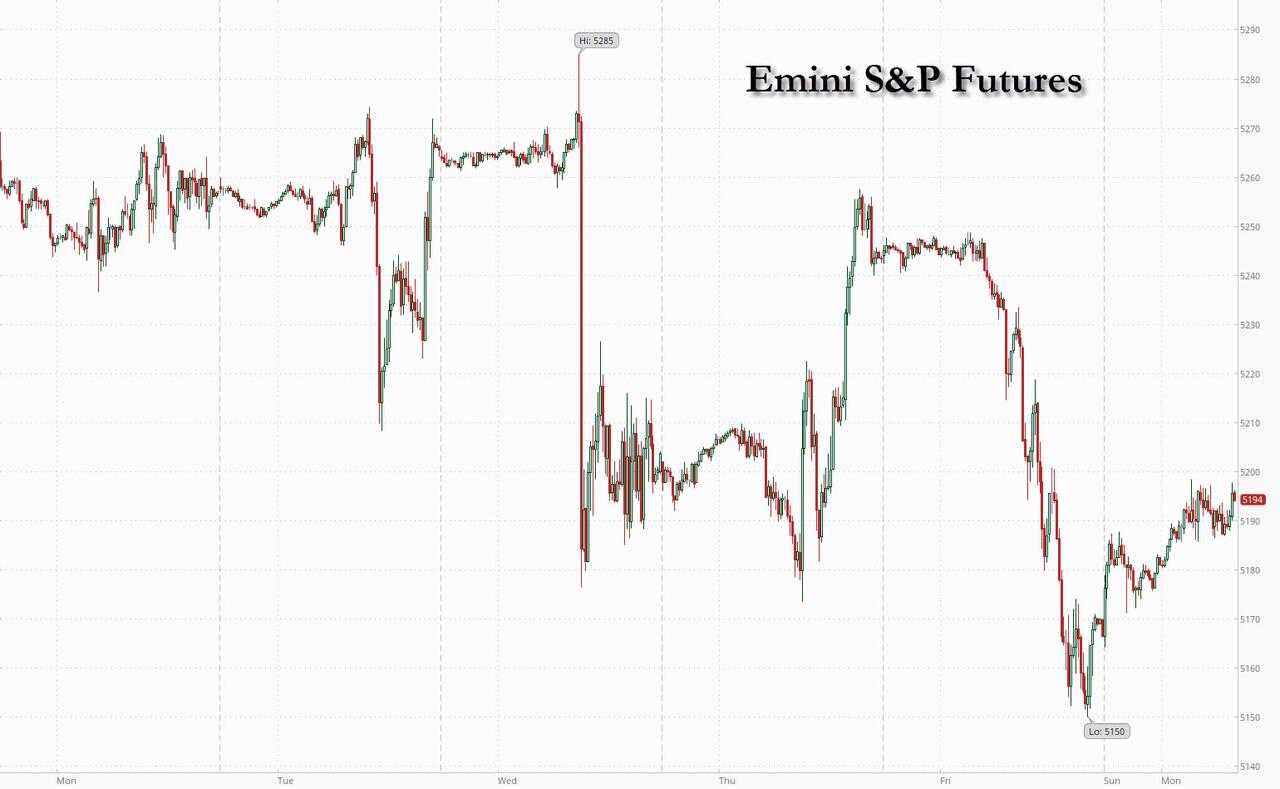

8:40 am

Good Morning!

SPX futures have risen to 5158.90 thus far this morning. The likely target may be Intermediate resistance at 5165.68. The bounce is likely to be over this morning or early afternoon. Should the SPX decline back toward the 50-deay, it may be poised for a panic decline either this afternoon or tomorrow.

Today’s options chain shows Maximum Investor pain at 5150.00. Long gamma begins at 5165.00 while short gamma may start at 5140.00.

ZeroHedge reports, “Following the emotional rollercoaster of this weekend geopolitical “straight to DVD” soap opera, in which Iran pretended to retaliate to Israel’s embassy bombing with an attack that was meant to be a dud (and succeeded), which in turn was followed by an even more dramatic de-escalation by Israel in which after much saber rattling Netanyahu did…nothing, futures and yield are predictably higher, while oil is lower. That’s right: after digesting the weekend’s news and realizing that what just happened was one giant farce, global markets are broadly higher (except for Asia which is always a few steps behind), with European stocks ticking higher and US rebounding from Friday’s 1.5% selloff in the S&P 500. As of 7:30am, S&P futures were 0.5% higher with Nasdaq futs rising 0.6%; Treasuries slipped along with the dollar. West Texas Intermediate crude dropped below $85 a barrel, while base metals rallied with Aluminum at one point surging more than 9% after Russian supply was hit by US and UK sanctions. Gold reversed Friday’s losses to rise above $2,350 an ounce and bitcoin – which was the weekend’s only operating market and saw the initial risk-off reaction – reversed all losses and is back to unchanged. Today, the macro focus will be Retail Sales release. Feroli expects headline Retail Sales to print +0.3% vs. +0.4% survey vs. +0.6% prior. China will release key macro data at 10pm ET tonight.”

VIX futures declined to 16.60 this morning, near the 61.8% retracement value at 16.57. The VIX Cycle may show strength through the rest of the week. The Current Master Cycle may run into early May.

Wednesday’s monthly options chain shows Max Pain at 15.50. Short gamma resides from 13.00 to 15.00. Long gamma starts at 16.00 and may run up to 60.00. The options market is on a hair trigger.

ZeroHedge observes, “VIX & MOVE have exploded

After months of a low volatility world we finally see some action in both VIX and MOVE. It is safe to say that derivatives markets are seeing more perceived risk than how actual equity markets are trading. Some even say that there is more upside to VIX from here. Our belief is that there is “catch-down” potential for equities from here, but that especially VIX probably has gone a little too far too fast.

What goes down must come up

Bond volatility has put in the biggest up move since September last year. Just when everybody agreed bond volatility was dead…

TNX has risen above 46.00 this morning as it journey’s toward the Cycle Top at 48.30. The Cycles Model indicates that strength may persist through the week.

I have family matter to care for today. Regular reports may resume tomorrow.