8:00 am

Good Morning!

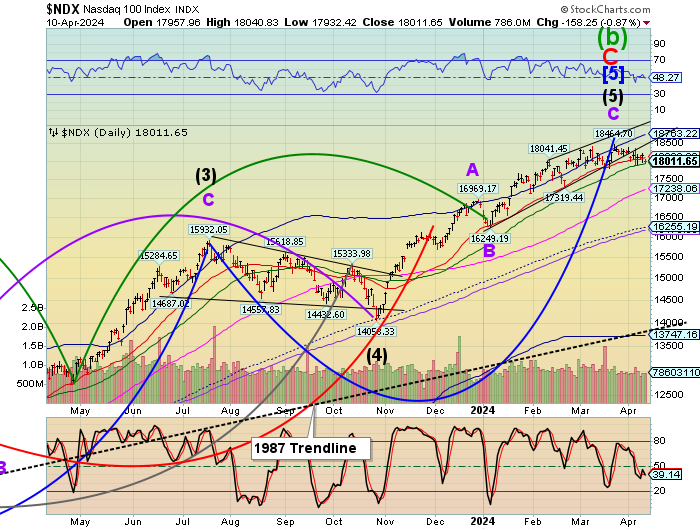

NDX futures have fallen to 17939.50 thus far this morning. It has been on a confirmed sell signal since April 5 and may be poised to decline beneath its 50-day Moving Average at 17933.15 today. Alternatively, should the 50-day Moving Average hold, NDX may bounce toward its Intermediate resistance at 18099.20, or possibly the trendline at 18500.0, since the Cycles Model pinpoints today as a day of strength.

Today’s options chain shows Maximum investor Pain at 18020.00-18125.00. Long gamma may start at 18150.00 while short gamma is massively positioned at 18100.00.

Zerohedge reminisces, “‘Sell Mortimer, Sell!’

That is the message (our translation) from Goldman Sachs Asset Management (GSAM), who told Bloomberg today that they are taking profits from high-flying technology shares and putting the money into cheaper companies.”

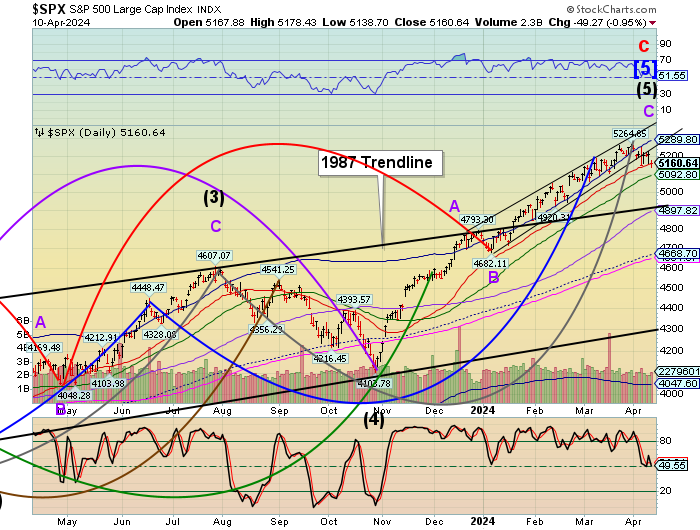

SPX futures have dipped beneath Intermediate support at 5161.37. Should they remain beneath that level, the next support is the 50-day Moving Average at 5092.80. Beyond that, the 1987 trendline may be key support. As with the NDX, today may be a day of trending strength, suggesting that, if SPX remains above Intermediate support, it may rally above 5200.00.

Today’s options chain shows Max Pain at 5175.00. Long gamma starts at 52500.00, while short gamma may begin beneath 5150.00.

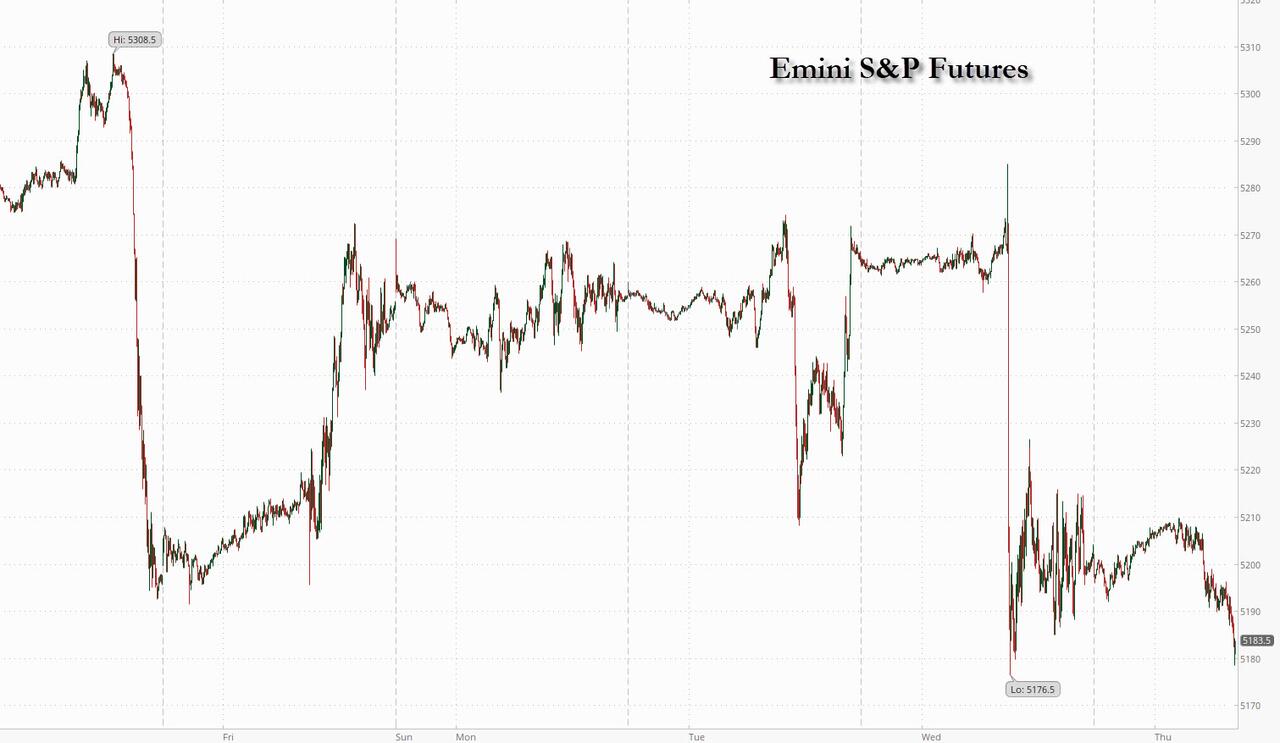

ZeroHedge reports, “Futures are weaker signaling further losses on Wall Street as stubborn inflation forces investors to reduce their expectations for Federal Reserve interest-rate cuts; tech stocks are underperforming following the significant surge in Treasuries yields which has continued today. As of 8:00am ET, S&P futures are down 0.5% and back to yesterday’s post-CPI session lows while Nasdaq futures are down 0.4%. Pre-mkt, Mag7 names are mixed, and small-caps set to underperform as yields move higher. Europe’s Stoxx 600 index also retreated, with most sectors in the red, as did Asian stocks. Treasury yields ticked higher again after the previous day’s surge, with the rate on the 10-year at 4.57%. Bonds in Europe dropped as traders trimmed their wagers on easing, with attention focused on the ECB’s policy announcement later; the USD is flat following its 1% surge yesterday, the strongest move since Mar 2023. Commodities are flattish with outperformance in base metals and crude. Today’s macro focus is on PPI and the ECB.”

VIX futures declined to 15.50 this morning, as it must complete a retracement before moving higher. As an example, s 61.8% retracement may take the VIX down to its 50-day Moving Average at 14.06

Next Wednesday’s options chain shows Max Pain at 15.50.00. Short gamma resides beneath 15.00 while long gamma starts at 16.00.

TNX futures declined from its high at 46.04 to a morning low at 45.19.The Cycles Model informs us that three of the six indicators of strength may be firing during the next week, suggesting that the Cycle Top may be within reach for the current Master Cycle.

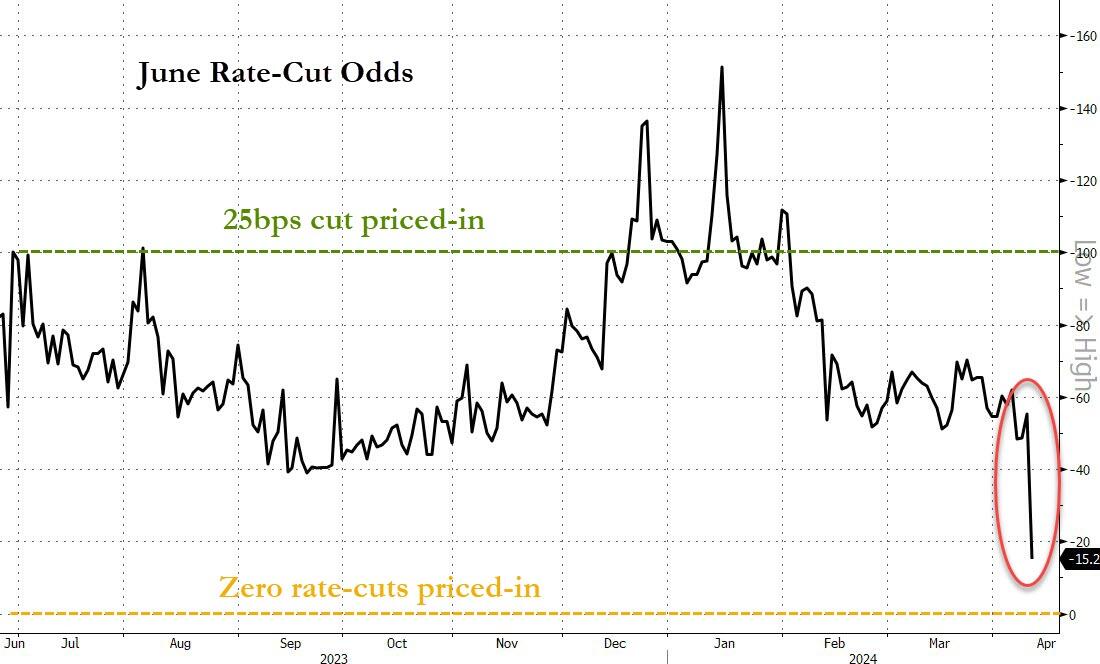

ZeroHedge remarks, “The fourth hotter-than-expected core inflation report in a row got investors reevaluating expectations around the Fed’s first rate cut…

Source: Bloomberg

Goldman’s Diana Asatryan noted that their Research group pushed its first rate cut forecast to July from June, expecting two cuts this year.

The market is now pricing in just 38bps (1.5 rate-cuts) in 2024…”