10:27 am

BKX is slowly losing its grip on the retracement rally. It made an early Master Cycle high March 28, on day 248 and may need another week to prove the high. In the meantime, critical support lies at the trendline at 101.00-101.50. Beneath that level is a sell signal with confirmation at Intermediate support at 98.83. A breakdown may lead to a broader sell-off in nearly all assets, as investors flee to cash.

ZeroHedge remarks, “There are more dormant office towers in the United States than at any point since 1979, according to a new report from Moody’s Analytics, which began tracking office leasing vacancies that year.

The rising supply of office space is due to a combination of surging remote and hybrid work that forces companies to reduce corporate footprints. Also, companies are exiting imploding progressive cities and high-taxed blue states for red ones while downsizing space.

In the report, office tower vacancies rose to a record 19.8%, up from 19.6% in the fourth quarter of 2023.”

8:25 am

Good Morning!

NDX futures retraced to 18132.30 before slipping back toward the trendline and Intermediate support at 18027.00. It is on an aggressive sell signal which may be confirmed beneath the abovementioned trendline. NDX marked its high on March 21. SPX made its high on March 28. Should those highs remain intact, the trend may be down until mid-May.

Today’s options chain shows Maximum Investor Pain at 18150.00. Long gamma may begin at 18200.00, while short gamma may start at 18100.00.

ZeroHedge reports, “Taiwan Semiconductor Manufacturing Co., the leading contract chipmaker for Apple Inc. and Nvidia Corp., shuttered some of its chipmaking capacity and evacuated plants after the biggest earthquake in 25 years rocked the island nation, just east of mainland China.

Taiwan plays a significant role in manufacturing advanced chips for artificial intelligence, smartphones, computers, and electric vehicles. The country is estimated to produce 80% to 90% of the highest-end chips.”

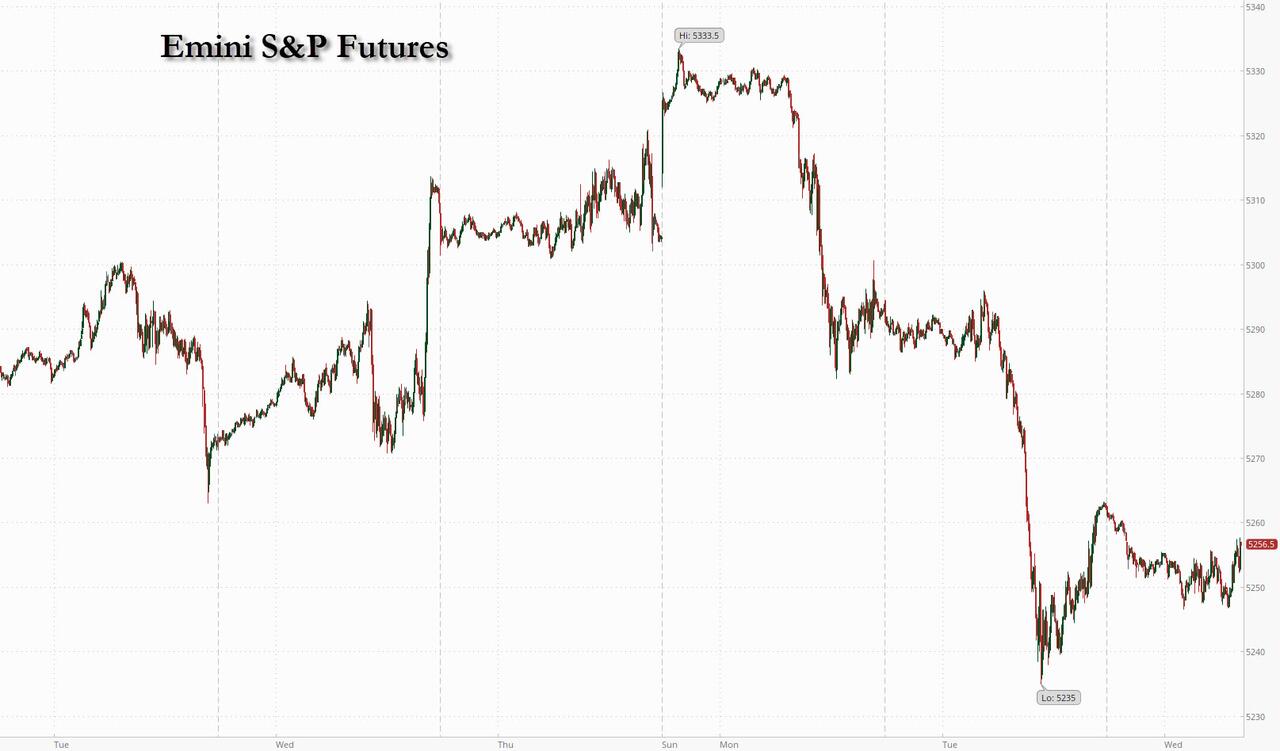

SPX futures back-tested the trading channel trendline at 5220.00, but failed to overcome it. Futures are lower but have not declined beneath short-term support at 5189.00. SPX made its all-time high on March 28 (day 245) and has not challenged that level since then. Intermediate support lies at 5126.28 and may provide support for a bounce.

Today’s op-ex shows Max Pain at 5210.00. Long gamma starts at 5225.00 while short gamma emerges beneath 5200.00.

ZeroHedge reports, “US futures are down small with Tech underperforming and small-caps flat, as rates held at 4 month highs, and Brent is about to rise above $90. As of 8:00am, both S&P and Nasdaq futures are down -0.2%, with yields higher pre-market ahead of Powell’s 12.10pm ET speech; despite his dovish rhetoric at the Mar 20 Fed Meeting press conference investors are nervous of a hawkish pivot according to JPM. This comes amid a surge a commodity prices and a spike in geopolitical tensions; pre-market all 3 commodity complexes are higher with gold the notable laggard despite USD being flat (although gold lagging these days means it hasn’t hit a new all time high in the past 15 minutes). Today’s macro focus is on ADP (has not been predictive of the brutally manipulated NFP print), ISM Services and 2x Fedspeakers, including Powell.”

VIX futures appear to be consolidating above the mid-Cycle support at 14.70. Trending strength is growing with a possible peak over the weekend and each successive weekend through the month of April. This may not be a coincidence, as the Fed has been attempting to downplay and delay the reports of bank problems until the close on Friday.

Today’s op-ex shows Max Pain at 14.50-15.00. Short gamma appears at 14.00, but long gamma begins at 16.00 shows strength at 23.00.

ZeroHedge notes, “5200 matters

This is where the lower part of the perfect Madoff channel comes in, as well as the 21 day moving average. 5200 is the make or break level.”

Source: Refinitiv

TNX continues to show strength as it advance above this year’s previous highs. The rally may last another 2-3 weeks, according to the Cycles Model.

ZeroHedge remarks, “Positioning in US Treasuries is becoming less long as the risk of persistently higher yields increases from a cyclically strong US and global economy.

Leading data have been vindicated in projecting a US and global cyclical upturn that coincident data are now unequivocally confirming. Monday’s release of the March ISM showed the index is back into expansion territory, matching the message from the manufacturing PMI.

The US manufacturing ISM is not only the best cyclical barometer of US growth, it is also the best single gauge of global growth given the sector’s outsized importance to the world economy.”

USD futures appear to be consolidating after yesterday’s potential Master cycle high on day 259. Should it take hold, the reversal may test the mid-Cycle support at 103.76. Should support hold, USD may be considerably higher by the end of May.

Gold futures have risen to a new all-time high at 2308.85 on day 247 of its master Cycle. Vigilance should be the by word as gold may reverse at any time in the next week. The decline may be greater than most would imagine.

ZeroHedge comments, “The rally in the gold price has left me non-plussed … who is behind it and why ? Rather like an Agatha Christie murder-mystery novel, with evidence thin, the culprit or cause may be deduced by excluding what it is not … and what remains, is.

Spoiler alert … I am really not sure of the answer, but follow me … it’s fun anyway. ”

Crude oil futures have advanced to a morning high at 86.08 as it continues its rally to the Cycle Top resistance at 90.44. There may be approximately 3 weeks left in this rally, so it may be doable. However, there may be a structural resistance near 86.60 that may impact the rally. Given that information, it is likely that a pullback toward mid-Cycle support at 79.75 may be in order before pressing higher.

ZeroHedge remarks, “US crude futures pierced $85 for the first time since October, the latest milestone in a rally driven by OPEC+ production cuts, strong demand and heightened geopolitical risks.

As Bloomberg reports, oil has jumped this week as tensions rise in the Middle East, with Iran vowing revenge on Israel for an airstrike on its embassy in Syria that killed a top military commander.

After last week’s surprise crude build and big jump in stocks at the Cushing hub, traders were looking for a slowing build…”