10:26 am

The Ag Index is at a critical juncture. It has declined beneath the neckline of a Head & Shoulders formation, leaving it susceptible to a further sell-off. There may be two weeks left in the current Master Cycle. However, if it cannot lift above the neckline at 385.00 or the mid-Cycle resistance at 3393.47, it may result in a panic decline in the second half of April. China has curtailed the purchase of agricultural goods from the US in 2023 and may purchase even less in 2024.

Reuters reports, ” U.S. exports of agricultural and related products reached a value of $191 billion in 2023, down 10% from 2022’s record as both commodity prices and shipment volumes declined.

10:14 am

BKX has pulled back from its Cycle Top at 102.31. It may show a weakening of its trend beneath the Cycle Top, but May not offer a sell signal until it declines beneath its trendline at 100.00. The Cycles Model allows two more weeks of rally, but the Wave structure indicates possible completion, or nearly so. There is a potential for a panic decline in the second half of April.

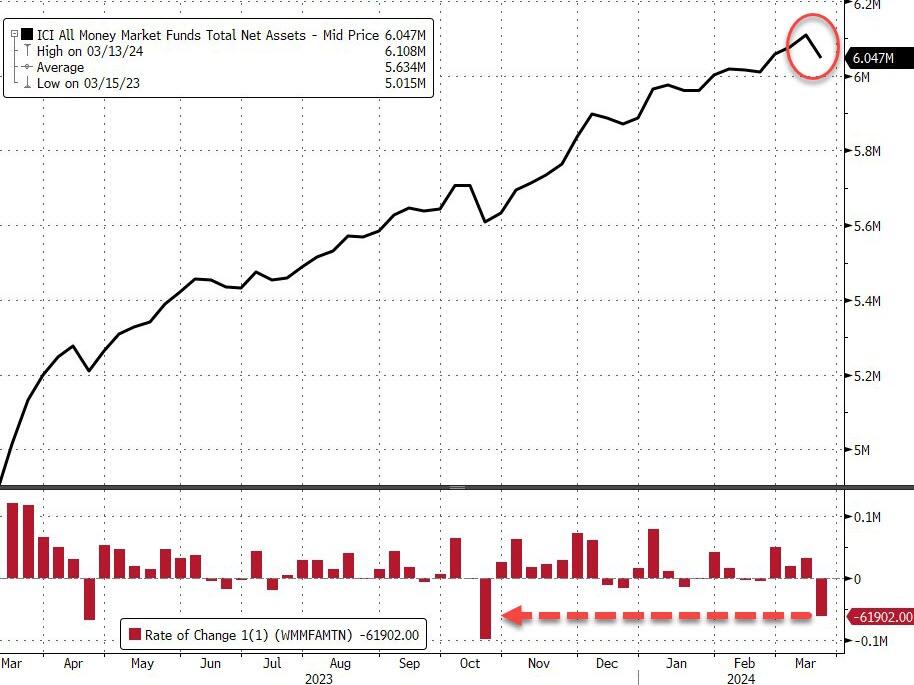

ZeroHedge remarks, “With The Fed’s bank bailout facility now expired, the 12-month term loans are starting to mature and the fund dropped over $17.2BN last week…

Source: Bloomberg

Money-market funds saw a big outflows of almost $62BN, which we wonder if related to tax-year liquidity issues, but it is a little early in the year…”

8:15 am

Good Morning!

SPX futures have declines to 5213.80, remaining above the Cycle Top support at 5178.81. It is on a buy signal until further notice. We may see a rise in volatility in the meantime. An aggressive sell signal may occur beneath the Ending Diagonal trendline near 5150.00. The Cycles Model gives this uptick another two weeks, coinciding with the solar eclipse due on April 8. That may not be a coincidence, as Cycles govern everything, including the planets.

Today’s options chain shows Maximum investor pain at 5235.00-5240.00. Long gamma may begin at 5250.00. Short gamma begins at 5200.00.

ZeroHedge reports, “Futs are lower following the S&P’s best weekly performance of the year (sparked by dovish comments by Fed chair Powell during the last FOMC) which sent the market up +2.3%. At 7:50am, S&P futures were 0.4% lower and Nasdaq futures dropped 0.6%, dragged by MegaCap tech names which were mostly lower with AMD and Intel down more than 2% after the FT reported they are being banned from Chinese government computers; NVDA swung from gains to losses after a report that Google, Intel and QCOM execs plan on battling NVDA on AI dominance (well what else can they do?). Meanwhile, JPM says to keep an eye on NFLX on bullish headlines; stock is +29% YTD which would be third among Mag7 names. Europe’s Stoxx Europe 600 dipped following nine straight weeks of gains, the longest run in 12 years. Elsewhere, treasury yields ticked higher and the Bloomberg dollar spot index was slightly lower with the yen a tad stronger after some aggressive jawboning by cartoonish Japanese officials. Oil gained on escalating geopolitical unrest following the Moscow concert hall attack on Friday that killed at least 137 people. The next 2 weeks have a lighter macro data calendar so keep an eye on Fedspeak (3x this week) and bond auctions for bond yield catalysts which could Equity sector performance. Month-end/Quarter-end rebalancing could also pressure stocks.”

VIX futures have climbed to 13.67 this morning, shy of the 50-day Moving Average at 13.81. Last Thursday may have seen the end of the Master Cycle at 12.40. A buy signal may be given as VIX rises above 13.81 with additional confirmation above the mid-Cycle support/resistance at 14.73. There is a slight chance of a probe beneath 12.40 in the next couple of days. Otherwise, we may see VIX rising even as SPX puts in its final high over hte next two weeks.

Wednesday’s op-ex shows Max Pain at 14.00 with a small contingent of shorts at 13.50. Long gamma starts at 14.50 and may extend to 30.00.

ZeroHedge exclaims, “Who’s dead?

Intra day volatility is dead, baby.”

Source: GS

TNX is rising from a low on Friday at 42.20 and has surpassed the Intermediate resistance at 42.26. It is on a buy signal which may have added confirmation above the mid-Cycle resistance at 42.52. The Cycles Model calls for rising rates to continue to mid-April. Trending strength may have begun and further boosts in strength may appear in early April. The Cycle Top at 48.28 may be a likely target.

USD futures declined to test Intermediate support at 103.76 this morning. A Master Cycle low may be expected next week near 102.00. The USD is in a secular bull market that may extend through the summer of 2024.