1052 am

BKX is making new retracement highs beyond the 61.8% level. The Cycles Model suggests we may see BKX going sideways or higher for another 2 weeks, while the Wave pattern appears complete.

ZeroHedge observes, ” At the start of the week, a lawyer specializing in advisory services for lenders and servicers of commercial mortgage-backed securities (CMBS) in the United States told us that the office segment of the commercial real estate market has been surprisingly quiet in the first quarter, despite the countless news headlines about towers being dumped on the market for hefty discounts.

The reason for this recent calm in the CRE space might be explained in a note by Vinay Viswanathan of Goldman Sachs on Tuesday.

Viswanathan explained that the total amount of outstanding commercial mortgages set to mature by year-end has exploded from $658 billion at the start of last year to $929 billion in mid-March. ”

9:20 AM

Good Morning!

SPX opened mildly positive, then gave up its gains. The Cycles Model suggests another two weeks of possible gains in the SPX. However, the Wave pattern suggests the end may be sooner.

Today’s options chain shows Maximum investor pain at 5230.00. Long gamma may start at 5340.00, intensifying at 5250.00. Short gamma may begin beneath 5200.00.

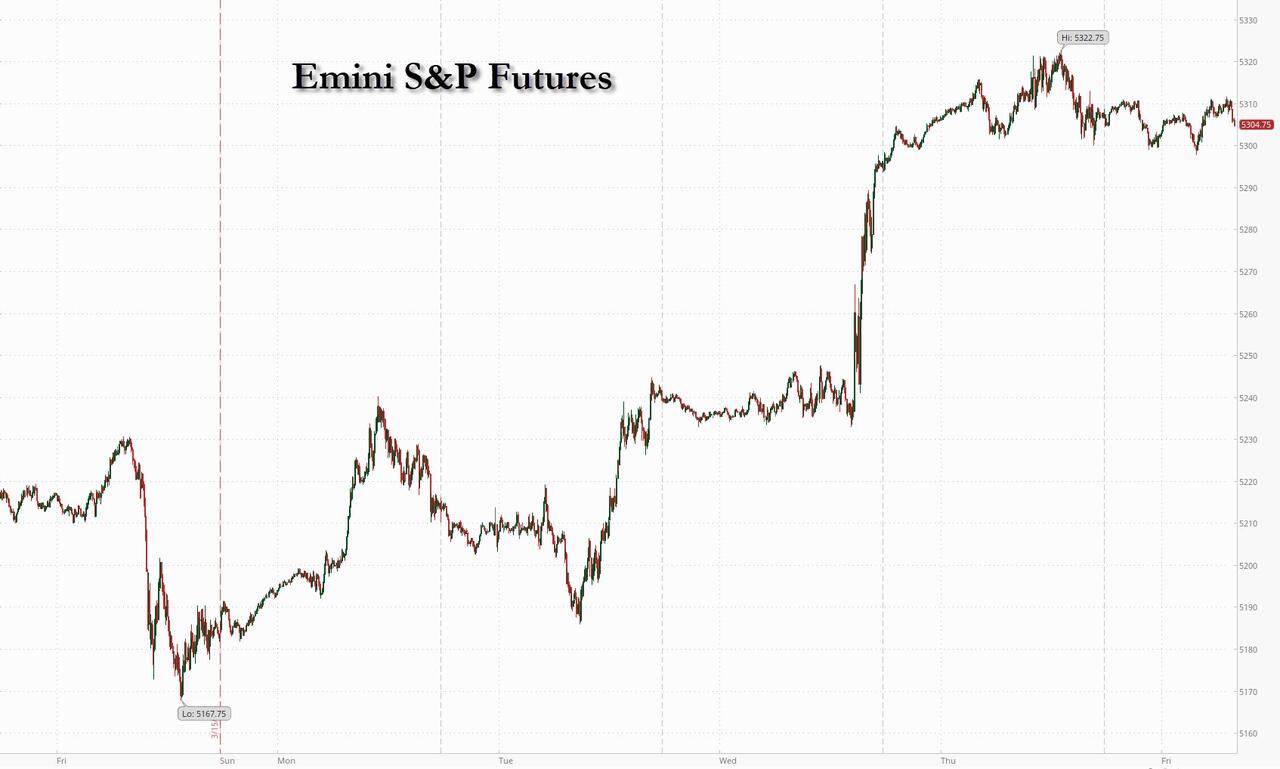

ZeroHedge reports, “Futures dropped modestly but were still on pace for their best week of the year after a raft of central bank meetings indicated that a pivot toward looser policy has been agreed upon at one of the recent central bank conclaves at the BIS tower in Basel, inflation – and 2% inflation target – be damned. As of 7:50am, S&P futures were down 0.2% and poised for a 2.2% weekly advance, the most since mid December; Nasdaq futures were also in the red as they looked to cap another blockbuster week. Friday’s selling came after the latest EPFR data revealed US stocks saw significant outflows in the runup to the Fed’s policy meeting that took the S&P 500 Index to fresh all-time highs. Market euphoria also pushed the MSCI index of global shares more than 2% higher this week so far. Europe’s stock benchmark headed for its longest weekly run of gains in more than a decade. Treasuries rose for a fourth day, taking the 10-year yield almost 10 basis points lower since Monday even as the dollar rose to the highest level in over a month. Gold dipped again after hitting a record high above $2,200 after Powell’s dovish FOMC. There are no scheduled events on the econ calendar; the US session highlight is Powell’s opening remarks at a Fed Listens event in Washington. ”

VIX appears to have made its Master Cycle low at 12.40 yesterday. It is hovering in the 12.80’s today and may make one more attempt at a lower low. One potential warning of a trend reversal is when the VIX begins rising while the SPX ventures higher. It may be wise to add protection to one’s portfolio while prices are low.

Wednesday’s op-ex shows Max Pain at 14.00. There is a single block of puts at 13.50. Otherwise the options chain is positive with calls dominating the 16.00 – 20.00 range.

TNX dropped to 42.00 this morning thus far. It may test the 50-day Moving Average at 41.69 before resuming its run to higher highs. The Cycles Model suggests that yields may rise with more strength by the end of March.

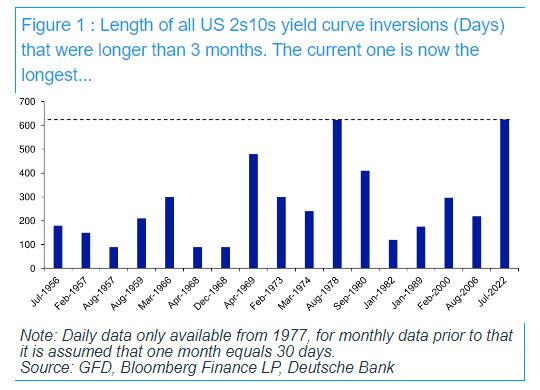

ZeroHedge remarks, “Today is a historic day, as last night – DB’s Jim Reid reminds us – we quietly passed the longest continuous US 2s10s inversion in history. After the 2s10s first inverted at the end of March 2022, it has now been continuously inverted for 625 days since July 5th 2022. That exceeds the 624 day inversion from August 1978, which previously held the record.

As regular readers are aware, an inverted yield curve has been the best predictor of a US downturn of any variable through history: the yield curve has always inverted before all of the last 10 US recessions, with a lag that is usually 12-18 months, but some cycles – certainly this one – take longer…. much longer.”